The affordability crisis is an inequality crisis. When prices spike in key sectors, it's not just inflation—it's a massive redistribution shock that hits poor households hardest. In our **new working paper**, we identify the sectors that matter most. A 🧵 scholarworks.umass.edu/entities/publi…

Standard inflation analysis reduces inflation to a single aggregate index. This conceals that inflation is often triggered by price shocks and that consumption baskets differ systematically across income groups, producing unequal inflation burdens. 2/16

Sectoral cost shocks are therefore non-neutral: when relative prices shift unevenly across essential goods, inflation redistributes income, increasing income inequality. 3/16

We ask: which sectors' price shocks have the largest potential to raise income inequality in the US, and how do these sectors overlap with the systemically significant sectors for inflation identified in earlier work? 4/16

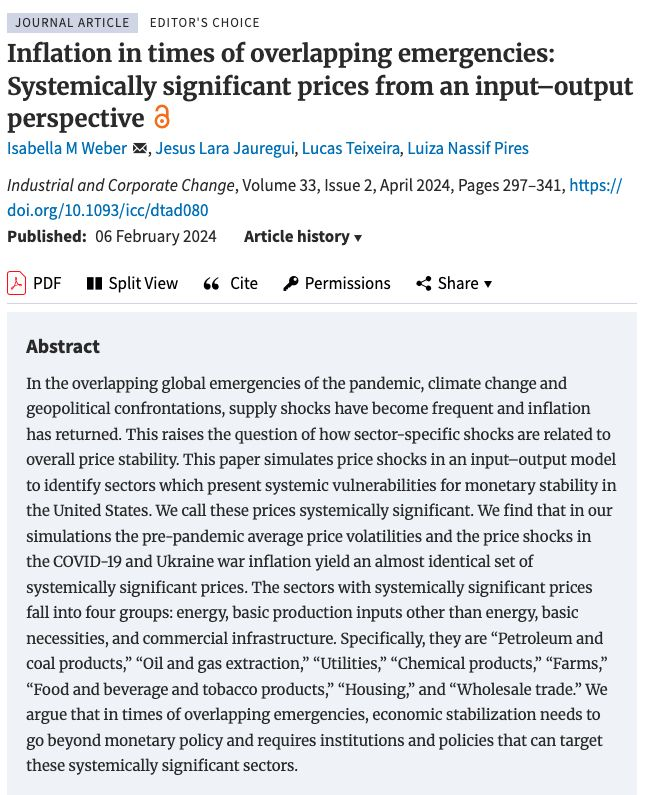

We extend the input–output price model developed by Weber et al. (2024), which traces how a price shock in one sector propagates through production linkages, increasing the overall price level. 5/16 academic.oup.com/icc/article/33…

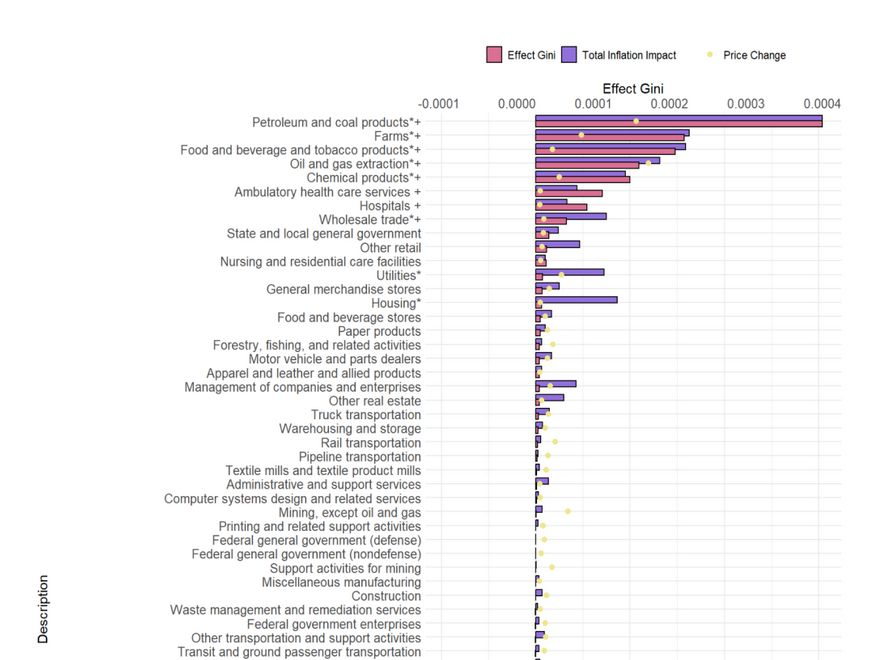

Using decile-specific consumption baskets, we simulate how each sectoral price shock affects each income group’s cost of living, mapping these heterogeneous effects into changes in the Gini coefficient, ranking sectors by inequality impact. 6/16

Consumption heterogeneity is central: even a uniform initial price increase produces sharply different inflation outcomes for poor and rich households, depending on the structure of spending across income groups. 7/16

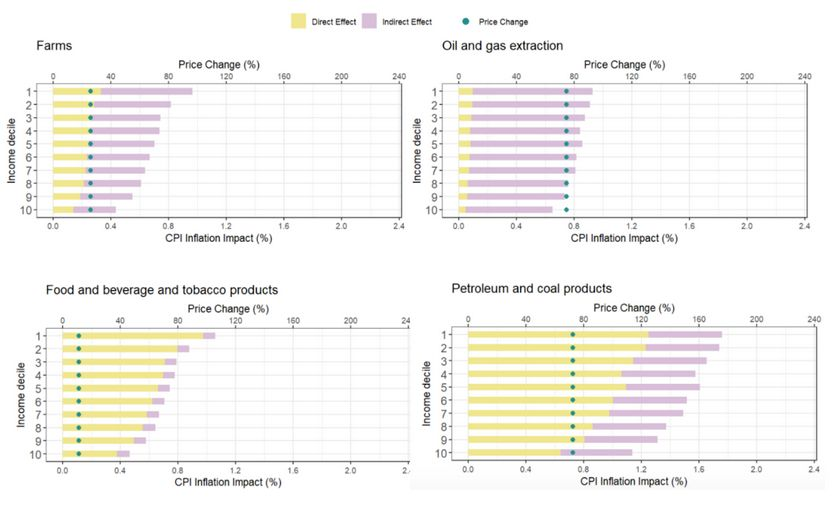

For example, a shock to food generates inflation 126% higher for the poorest than the richest decile; for petroleum and coal products, inflation is 54% higher for the poorest, revealing sectors where price increases have systemic distributional effects. 8/16

Using pre-pandemic sectoral price volatility and real 2022 Q2–2023 Q2 price changes as shocks, we find that the capacity to increase inequality is highly concentrated within a small set of systemically significant sectors for inequality (SSS-I). 9/16

These sectors span energy (oil, gas, petroleum & coal), food and agriculture, chemicals, housing, wholesale trade, and healthcare. With the important exception of healthcare, they mirror the sectors that propagate inflation systemically. 10/16

This overlap implies that targeted price stabilization must be studied jointly with inflation and inequality, because shocks to these prices simultaneously raise the price level and regressively redistribute real income. 11/16

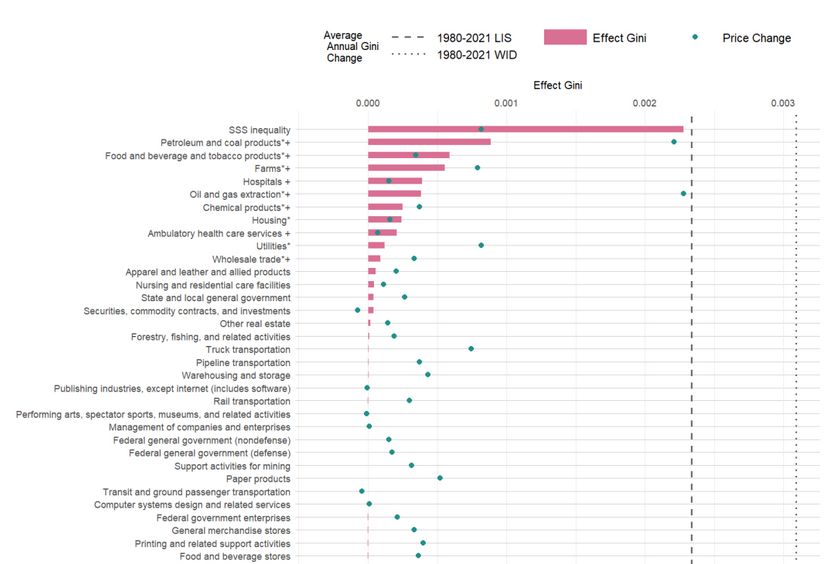

The 2021-2022 joint shock to the eight systemically significant sectors raises the Gini coefficient by 0.0023—approximately one full year of the average annual increase in inequality observed during 1980–2021. 12/16

Shocks to petroleum and coal products alone ≈ 1/3 of a yearly inequality increase, while food and agriculture shocks each ≈ 2/3 of that last magnitude, underscoring their disproportionate redistributive capacity. 13/16

These shocks do not simply move the aggregate price level—they reshape the distribution of real income, compressing structural inequality dynamics in a single inflationary episode. 14/16

Interest-rate hikes do little to lower the price of oil or food, yet they raise debt costs and weaken labor markets, amplifying inequality. Using blunt monetary tightening against supply shocks is both inefficient and regressive. 15/16

Macroeconomic stability and the stability of the real income distribution are intertwined. A toolkit based on strategic reserves, supply resilience, and sector-specific price instruments can contain inflation without worsening inequality. 16/16

• • •

Missing some Tweet in this thread? You can try to

force a refresh