REITs are often bought for ‘passive income from real estate’ without actually owning the property. We looked at payout data since 2022 to ask: did the income match the yield you’d expect, and did payouts keep rising every year?

Here’s a Varsity explainer, plus the biggest REIT myth.

Here’s a Varsity explainer, plus the biggest REIT myth.

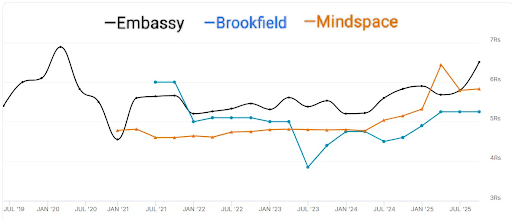

India currently has five publicly listed REITs: Embassy, Brookfield, Mindspace, Nexus Select Trust, and Knowledge Realty Trust. The REIT story in India is still fairly recent; the first public REIT, Embassy Office Parks REIT, was listed only in 2019.

Most Indian REITs are predominantly focused on office spaces. Nexus Select Trust, on the other hand, is primarily retail-focused (shopping malls).

Most Indian REITs are predominantly focused on office spaces. Nexus Select Trust, on the other hand, is primarily retail-focused (shopping malls).

If you’re buying REITs mainly for passive income, here’s what the data from above table suggests:

- Has the income been consistent? Broadly, yes. REITs typically pay distributions quarterly.

- Has the amount you receive grown every year? Not necessarily. You can’t expect it with certainty because vacancies, tenant movement, and costs affect what gets paid out.

- Have distributions kept pace with inflation every year? Maybe over the long run, they could, but not necessarily in every single year. India’s inflation over the last few years has roughly been in the 4% to 6.5% range, and distributions haven’t outpaced inflation year after year consistently. Also, the market is still young, so we need more years of data to conclude this strongly.

- Has the income been consistent? Broadly, yes. REITs typically pay distributions quarterly.

- Has the amount you receive grown every year? Not necessarily. You can’t expect it with certainty because vacancies, tenant movement, and costs affect what gets paid out.

- Have distributions kept pace with inflation every year? Maybe over the long run, they could, but not necessarily in every single year. India’s inflation over the last few years has roughly been in the 4% to 6.5% range, and distributions haven’t outpaced inflation year after year consistently. Also, the market is still young, so we need more years of data to conclude this strongly.

Do these observations change dramatically in the future? Mostly, no. The exact rupee amount you receive will vary with your entry price (since that decides how many units you own). But the broader trends observed above will mostly remain the same.

Now, the biggest REIT myth: “Distributions rise every year because commercial rents have escalation clauses."

Sounds logical. But payout data since 2022 doesn’t support it. Some REITs had flat or even lower payouts in certain years.

Sounds logical. But payout data since 2022 doesn’t support it. Some REITs had flat or even lower payouts in certain years.

Why so?

- Escalations may kick in only once every 3–5 years

- Tenants leave → vacancies hit cash flows

- Borrowing gets expensive when rates rise

- Maintenance/capex reduces what’s available to distribute

And a couple of other factors.

So expect a regular income stream, but not a guaranteed yearly increase.

- Escalations may kick in only once every 3–5 years

- Tenants leave → vacancies hit cash flows

- Borrowing gets expensive when rates rise

- Maintenance/capex reduces what’s available to distribute

And a couple of other factors.

So expect a regular income stream, but not a guaranteed yearly increase.

And finally, as you know that distributions are only one part of REIT returns. The second part is capital appreciation. Over time, if the underlying buildings become more valuable, the REIT’s portfolio value can rise too. But your realised return also depends on the price you pay in the market.

Our recent Second Order newsletter covered how to assess a REIT and the current state of REITs in India.

zerodhavarsity.substack.com/p/indian-reits…

Our recent Second Order newsletter covered how to assess a REIT and the current state of REITs in India.

zerodhavarsity.substack.com/p/indian-reits…

• • •

Missing some Tweet in this thread? You can try to

force a refresh