The State of Fintech 2026:

Nubank: 127m customers

Klarna: 114m

Revolut: 65m

A handful of companies now have more users than most countries have people.

We've entered the Age of the Fintech Hyperscaler.

🧵 What I learned writing the annual report with @jevgenijs

Nubank: 127m customers

Klarna: 114m

Revolut: 65m

A handful of companies now have more users than most countries have people.

We've entered the Age of the Fintech Hyperscaler.

🧵 What I learned writing the annual report with @jevgenijs

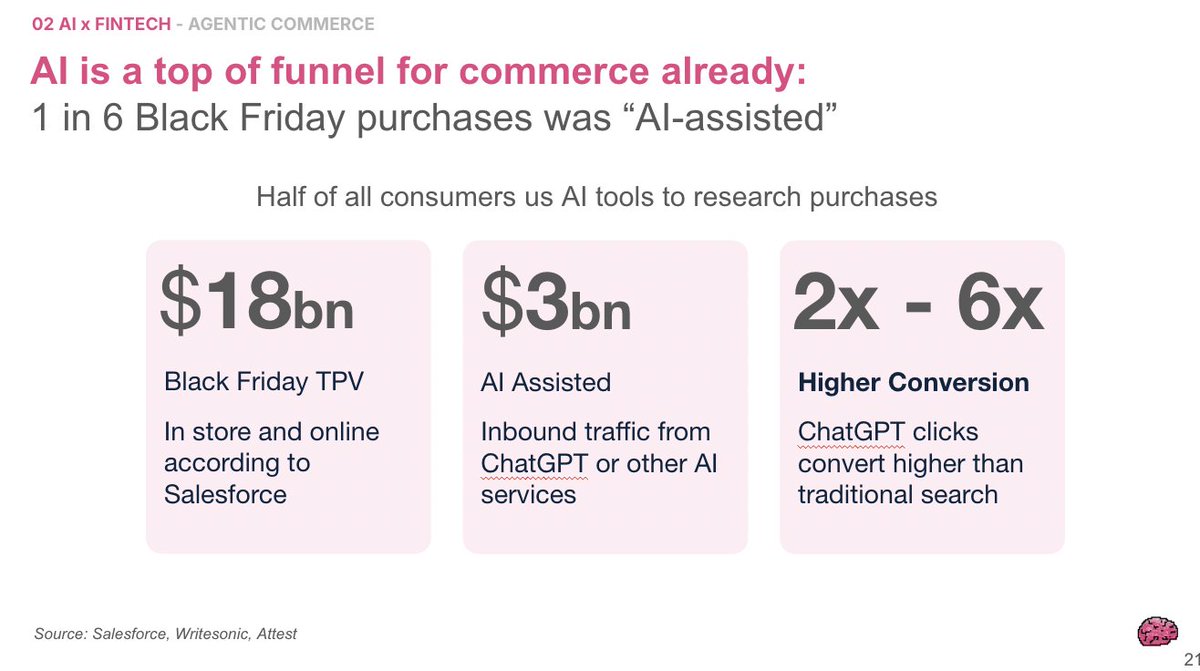

AI assisted 1 in 6 purchases this Black Friday.

It showed in the data for the first time.

But here's the uncomfortable truth:

Almost no fintech has an industry-specific foundation model driving earnings.

Stripe is the only example I found.

The rest is still vibes.

It showed in the data for the first time.

But here's the uncomfortable truth:

Almost no fintech has an industry-specific foundation model driving earnings.

Stripe is the only example I found.

The rest is still vibes.

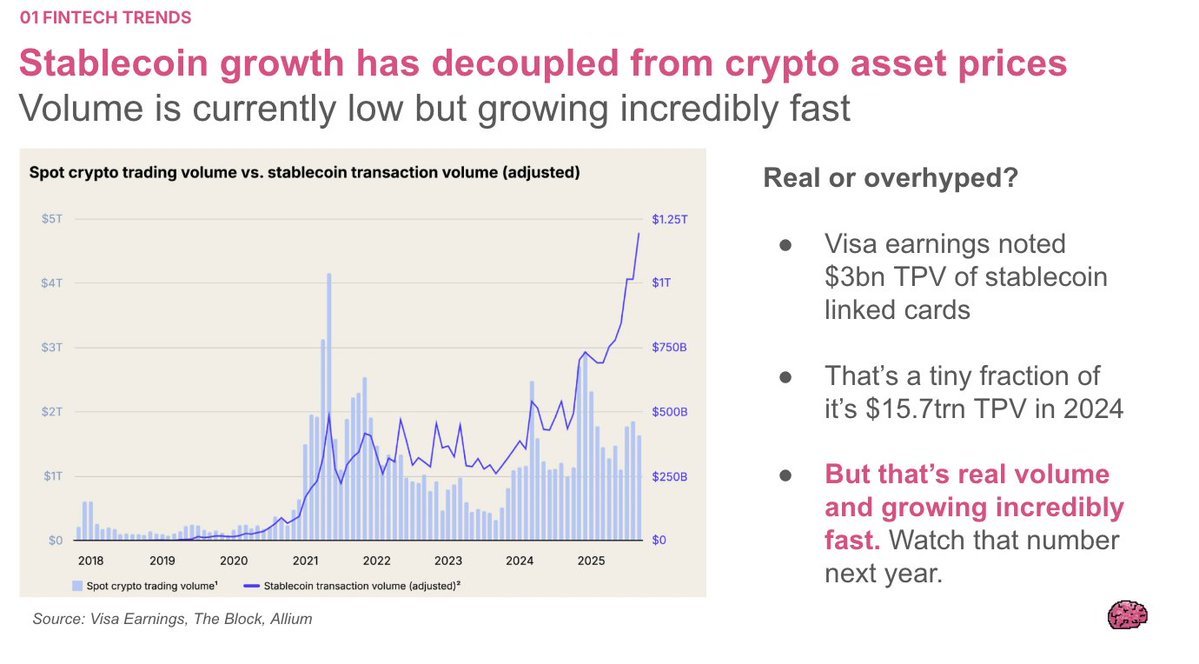

Stablecoins found product-market fit.

Not as "bank killers."

As cross-border rails and corporate treasury tools.

The use case that won: payouts and pay-ins for businesses tired of correspondent banking.

Boring? Yes. Working? Also yes.

Not as "bank killers."

As cross-border rails and corporate treasury tools.

The use case that won: payouts and pay-ins for businesses tired of correspondent banking.

Boring? Yes. Working? Also yes.

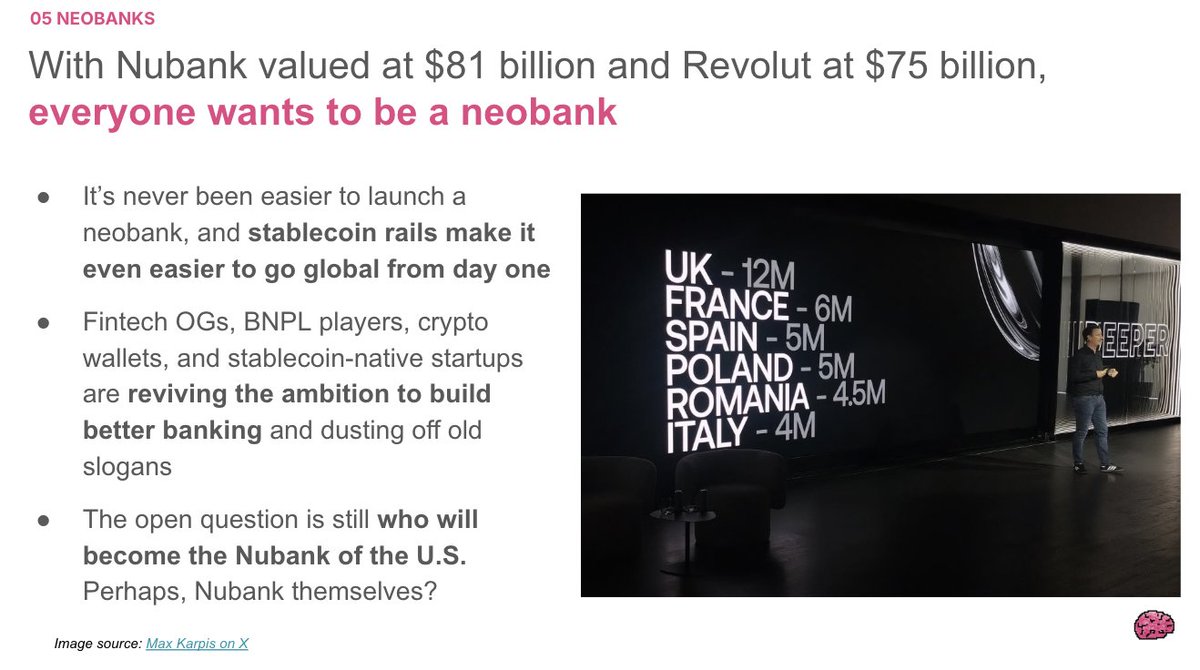

The plot twist of 2025?

Everyone wants to be a neobank now.

- Robinhood → launching cards

- Klarna → launching cards

- Affirm → launching cards

Cards became the universal growth lever.

The BNPL wars evolved into the neobank wars.

Everyone wants to be a neobank now.

- Robinhood → launching cards

- Klarna → launching cards

- Affirm → launching cards

Cards became the universal growth lever.

The BNPL wars evolved into the neobank wars.

But here's what everyone's missing:

Banks had a RECORD year.

Far from being disrupted, M&A tailwinds and macro helped them grow.

Citi and Wells are back in position to compete.

The "banks are dead" narrative needs to die.

Banks had a RECORD year.

Far from being disrupted, M&A tailwinds and macro helped them grow.

Citi and Wells are back in position to compete.

The "banks are dead" narrative needs to die.

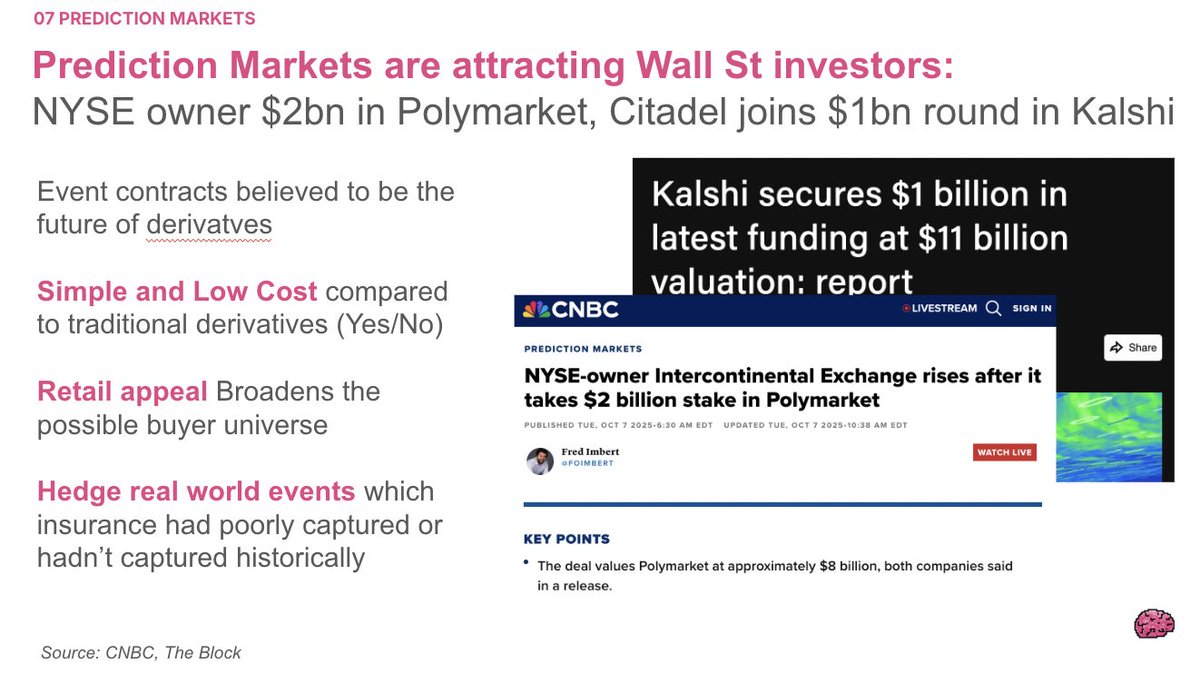

Prediction markets had their breakout year.

Wall Street firms started making strategic bets.

Polymarket became a news source.

The debate now is between "is this gambling?" and "is this price discovery?"

Wall St has made its choice.

Wall Street firms started making strategic bets.

Polymarket became a news source.

The debate now is between "is this gambling?" and "is this price discovery?"

Wall St has made its choice.

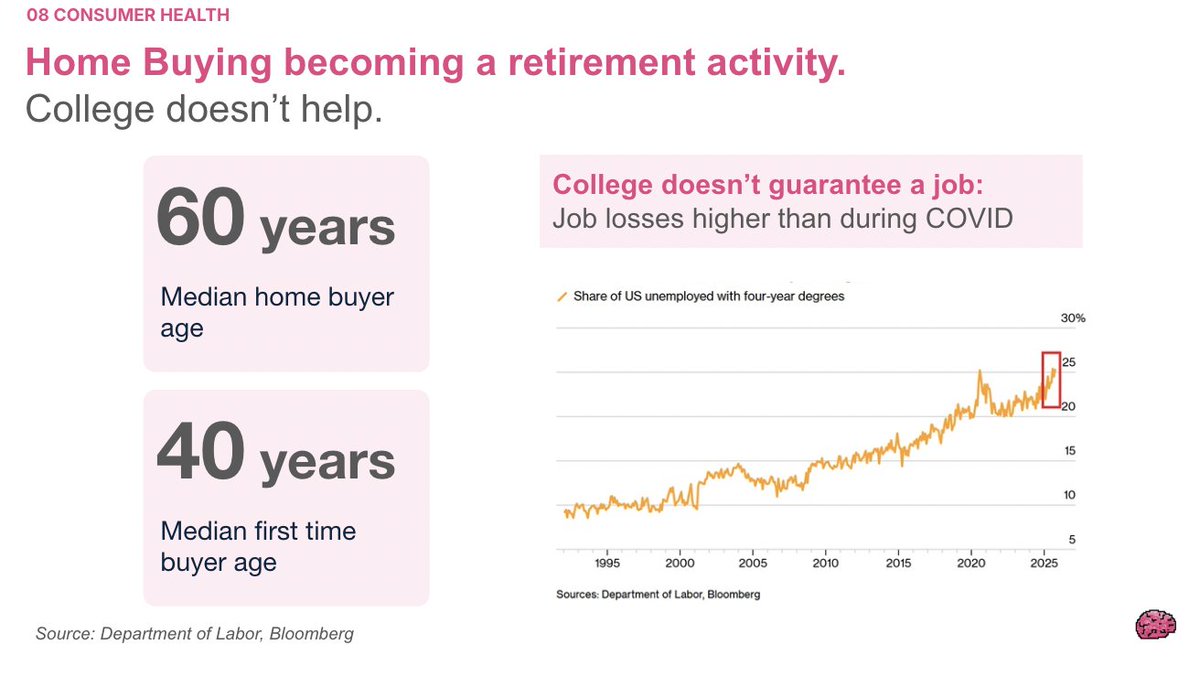

Now for the uncomfortable part.

Consumers no longer believe the 60/40 portfolio leads to retirement.

Housing costs broke the social contract.

This is why every Western incumbent gets voted out.

Financial nihilism isn't a meme. It's a political force.

Consumers no longer believe the 60/40 portfolio leads to retirement.

Housing costs broke the social contract.

This is why every Western incumbent gets voted out.

Financial nihilism isn't a meme. It's a political force.

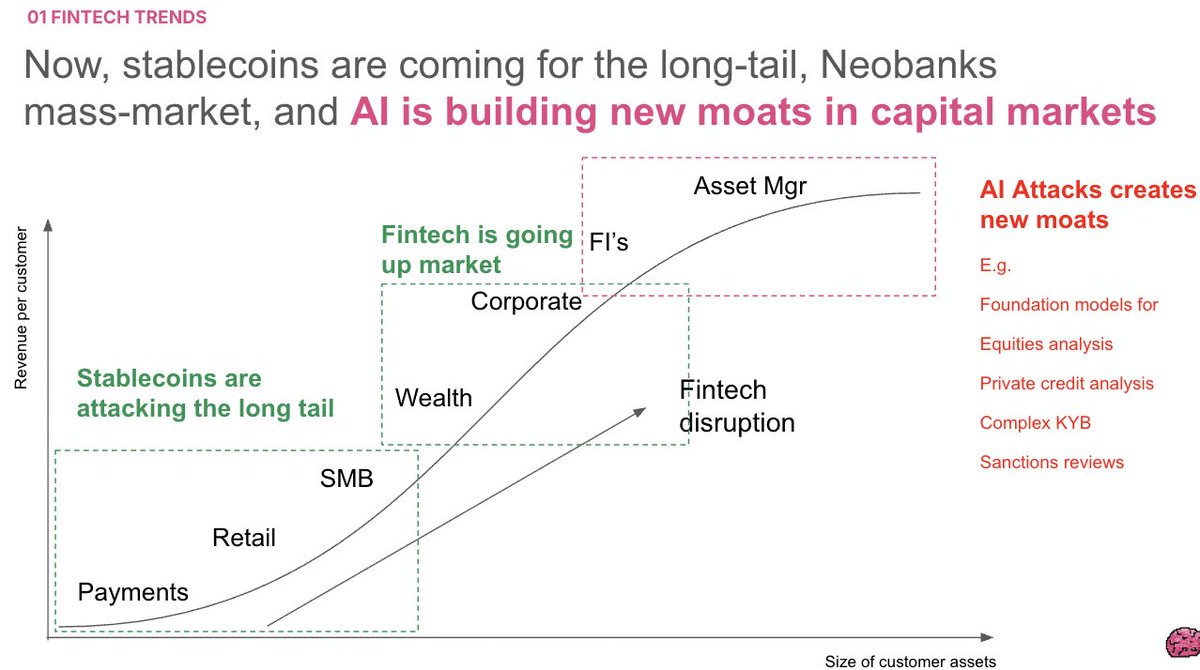

What's actually happening:

- Neobanks → coming for mass affluent

- Stablecoins → attacking the long tail

- AI → unbundling asset manager workflows

Three different attacks on the same system.

The wedges are in place. 2026 is execution.

- Neobanks → coming for mass affluent

- Stablecoins → attacking the long tail

- AI → unbundling asset manager workflows

Three different attacks on the same system.

The wedges are in place. 2026 is execution.

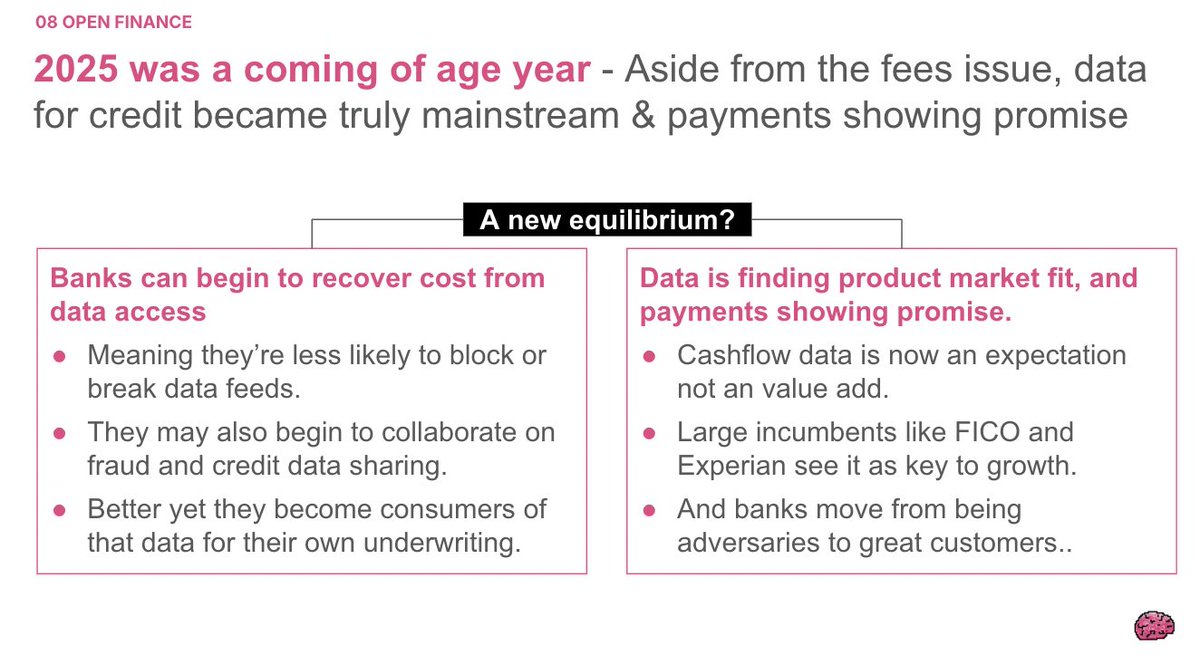

One thing that worked quietly in 2025:

Open finance.

Cash flow data is now used by Experian and FICO.

The ugly data-sharing deal with banks? It let business resume.

Sometimes the boring compromise wins.

Open finance.

Cash flow data is now used by Experian and FICO.

The ugly data-sharing deal with banks? It let business resume.

Sometimes the boring compromise wins.

Full 110 slide report with:

- Every hyperscaler breakdown

- 2026 predictions

- The data behind each trend

Find it at the link in the bio.

What surprised YOU most about fintech in 2025?

- Every hyperscaler breakdown

- 2026 predictions

- The data behind each trend

Find it at the link in the bio.

What surprised YOU most about fintech in 2025?

• • •

Missing some Tweet in this thread? You can try to

force a refresh