As mentioned now that mkts are open again I will do a no of deep dive 🧵 on Humm Group $HUM.AX.

As you prob know, I own ~29mm shs here (~$20mm AUD); and have (along w/ CSAM) called an EGM to effect Board Renewal, that will be held on Feb 19, 2025. All details here:

hummboardcleanout.com

These threads will be organized as follows:

1) What are we playing for? (valuation, etc - 50+% upside imo if we win)

2) The status quo (incumbent Board) and what it offers

3) What I/new Board offers + event/arbitrage set-up

NB you should only look at this if you intend to vote in the EGM. It is not hard to vote - full instructions will be forthcoming - takes 5min online for most Aussie shareholders. If you hold through IBKR/overseas brokers it is a bit more involved but still, not exactly difficult.

Also - given the high reflexivity of this idea - that is, the more who believe in it and vote, the more likely it is to work - if you agree w/ the thesis/goal, I would appreciate all sharing on this one. 🙏🙏

OK, on to the 🧵, what are we playing for?

As you prob know, I own ~29mm shs here (~$20mm AUD); and have (along w/ CSAM) called an EGM to effect Board Renewal, that will be held on Feb 19, 2025. All details here:

hummboardcleanout.com

These threads will be organized as follows:

1) What are we playing for? (valuation, etc - 50+% upside imo if we win)

2) The status quo (incumbent Board) and what it offers

3) What I/new Board offers + event/arbitrage set-up

NB you should only look at this if you intend to vote in the EGM. It is not hard to vote - full instructions will be forthcoming - takes 5min online for most Aussie shareholders. If you hold through IBKR/overseas brokers it is a bit more involved but still, not exactly difficult.

Also - given the high reflexivity of this idea - that is, the more who believe in it and vote, the more likely it is to work - if you agree w/ the thesis/goal, I would appreciate all sharing on this one. 🙏🙏

OK, on to the 🧵, what are we playing for?

$HUM.AX is a non-bank lender (non-bank financial services), w/ two main businesses: Commercial and Consumer. This is a quintessential 'good business, bad Board' set-up. Fundamentally there isn't much wrong w/ the business, I am not trying on some massive operational turnaround, this is all about simple blocking and tackling on capital allocation and proper, fit for purpose governance norms.

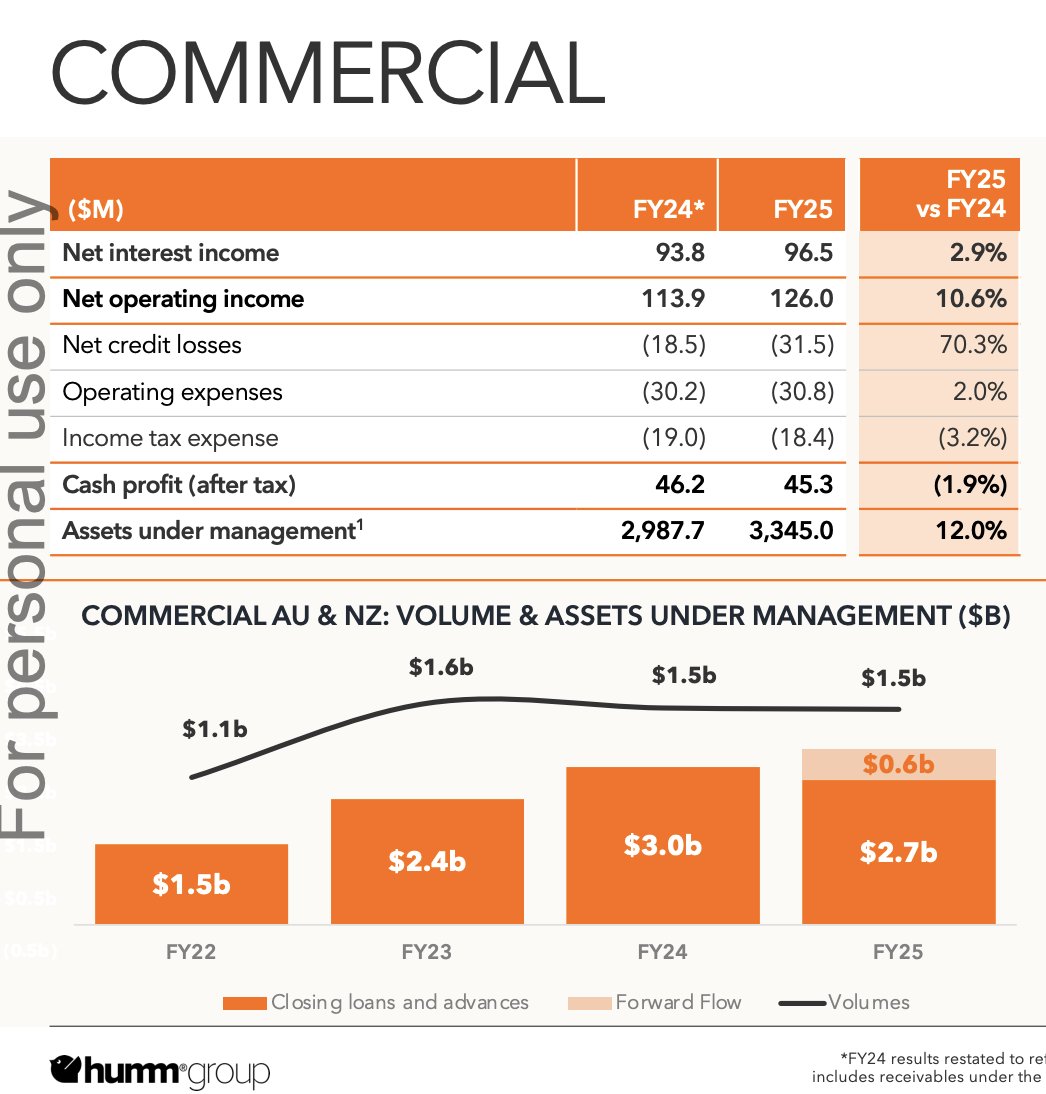

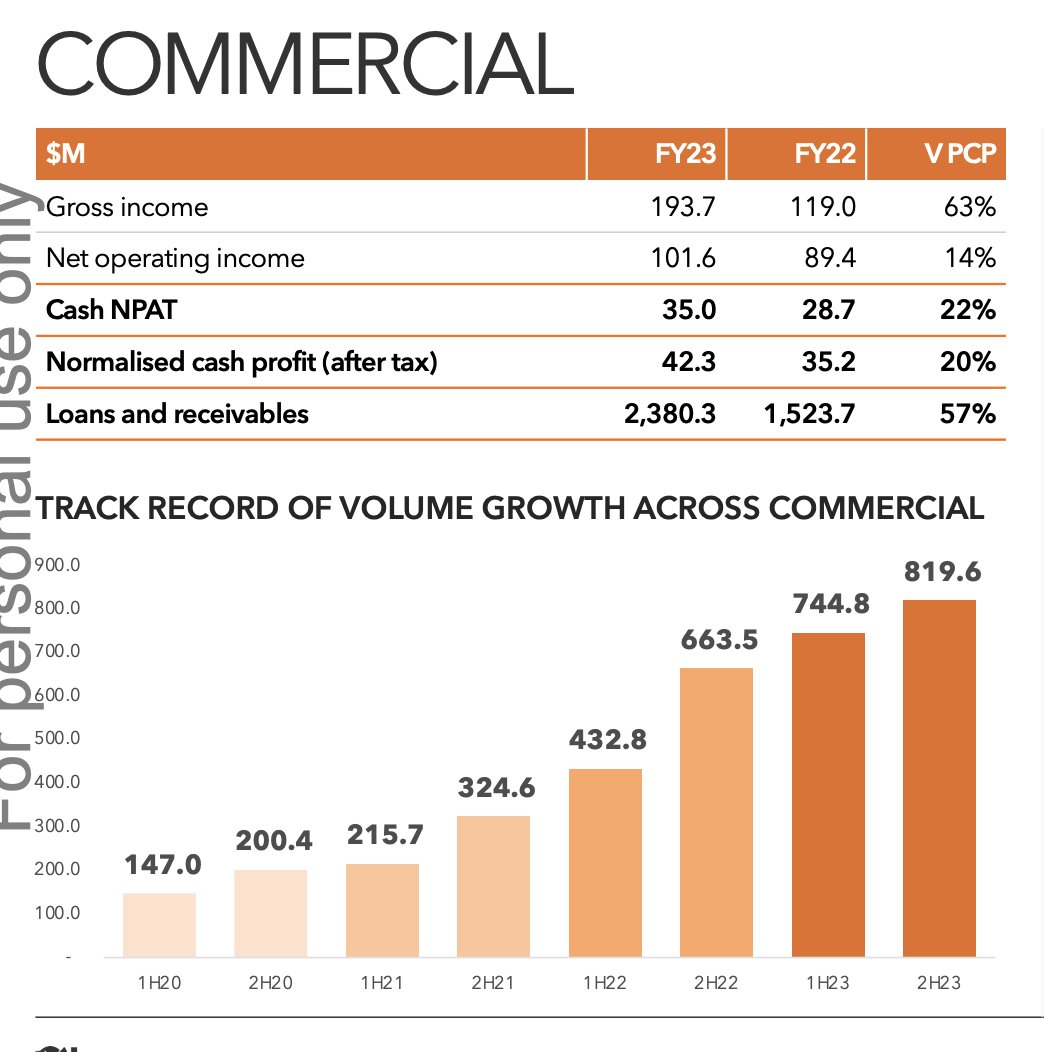

Commercial is a jewel, they provide asset-backed financing to SMEs, for things like equipment, vehicles, inventory. Per below, this segment alone is doing $45-46mm NPAT:

Commercial is a jewel, they provide asset-backed financing to SMEs, for things like equipment, vehicles, inventory. Per below, this segment alone is doing $45-46mm NPAT:

Commercial has a long track record of structural growth (see below). AUM is growing, avg losses have been stable (and low) at ~1%; and CTI has improved sequentially over last 4yrs (currently <25% ie v competitive for this type of biz).

The opportunity remains large as banks continue to cede share to non-bank lenders (like $HUM.AX) better able to quickly offer and disburse credit to SMEs.

The opportunity remains large as banks continue to cede share to non-bank lenders (like $HUM.AX) better able to quickly offer and disburse credit to SMEs.

What is Commercial worth, free and clear?

There is nothing exactly like it listed in Aus - no pure comps - but an analogous biz is perhaps Scottish Pacific. PE owned, mostly inventory financing (ie riskier), more levered, and private.

scotpac.com.au

There is nothing exactly like it listed in Aus - no pure comps - but an analogous biz is perhaps Scottish Pacific. PE owned, mostly inventory financing (ie riskier), more levered, and private.

scotpac.com.au

ScotPac was acquired by Affinity in 2018 for 17-18x P/E, and well over 2x P/NTA...

It currently has a $2.1bn loan book - that is, maybe a third smaller than $HUM.AX Commercial - and is being marketed currently for $650mm USD...or over 10x EBIT...theaustralian.com.au/business/datar…

It currently has a $2.1bn loan book - that is, maybe a third smaller than $HUM.AX Commercial - and is being marketed currently for $650mm USD...or over 10x EBIT...theaustralian.com.au/business/datar…

Implying perhaps 13-14x NPAT.

We can debate specifics and cap structure but at a minimum this suggests Commercial, unencumbered, is worth a dd multiple of NPAT, call it $500mm minimum (ie no synergies).

Thats $1/share just for Commercial (since FDSO is 500mm)...

We can debate specifics and cap structure but at a minimum this suggests Commercial, unencumbered, is worth a dd multiple of NPAT, call it $500mm minimum (ie no synergies).

Thats $1/share just for Commercial (since FDSO is 500mm)...

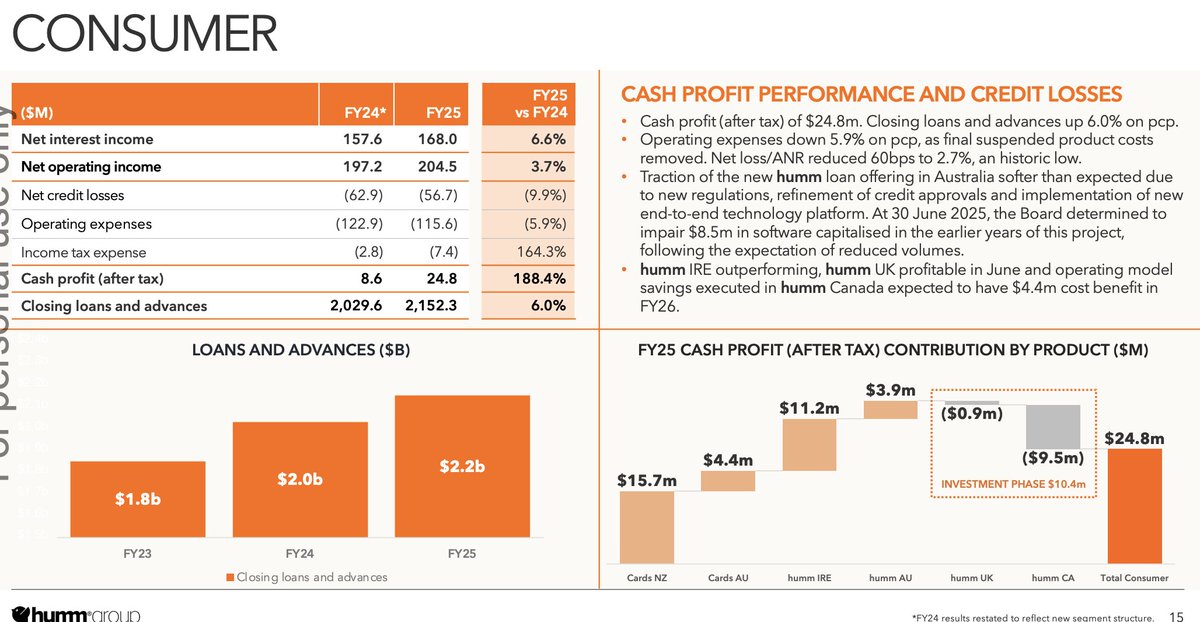

Then there is Consumer - a bit more of a hodge podge, and admittedly much lower quality. Consumer has been built by acquistion, it includes some quite good businesses - NZ Cards, AU Cards, Ireland - and some more marginalized segments (BNPL in Aus, Canada, etc).

Still the biz has continued to grow, with scale benefits and cost cutting outweighing share loss and more competition in some of the more commoditized segments. Today it remains highly profitable w/ KPIs generally improving:

Given the mixed models tho the most intellectually consistent way to value the co is consolidated (incl corp costs which run $15-20mm pa and look v high to me) and comp vs other Aussie listed non-bank financials.

This is the core of the argument, doing this $HUM.AX looks v cheap.

This is the core of the argument, doing this $HUM.AX looks v cheap.

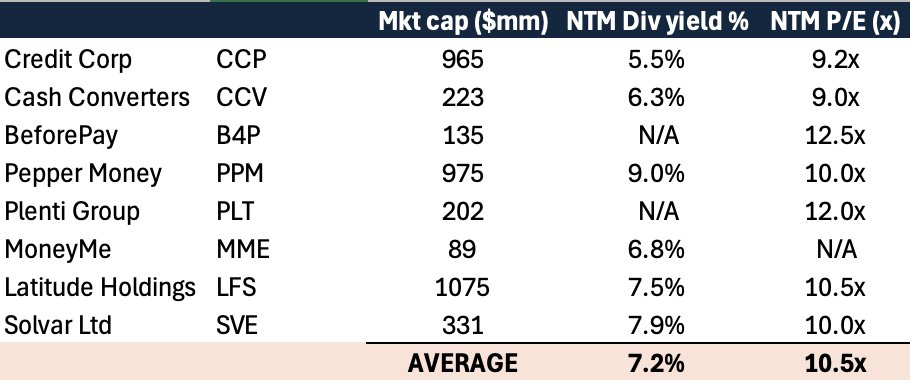

Most all non-bank lenders in Aus trade at a multiple of NTA; ~10x net income; and with a single digit dividend yield % - but most all of them not in hypergrowth mode pay out the majority of net income as divs. This is the range no matter the subsegment; biz model; growth rate; or capital structure:

Ref 70c, $HUM.AX is 6.5x P/E, but only 2.8% div yield...because they pay out <25% of their earnings as divs. Keep in mind they also have 20% of the mkt cap in NET cash, vs many others in the above carrying leverage at the corporate level...

It should be obvious what we are playing for here. If $HUM.AX traded at 10.5x P/E - the avg - it would trade at $1-1.10 per share (earnings volatility aside). If they paid out 75% of net earnings and traded at a 7.5% yield it would trade above $1 per share.

You see where I am going with this. Keep in mind $HUM.AX also has >$65mm of net cash - 13c a share - and over 3.5c per share of franking credits as well.

That is, paying out excess capital, through divs and a prompt buyback, would return most all o this 13-16c per share...

That is, paying out excess capital, through divs and a prompt buyback, would return most all o this 13-16c per share...

...to the shareholders, and would engender a rerating to (in my view) at a minimum a peer multiple.

Hence TSR in the near-term - should this capital allocation policy be followed - be something like 13-16c of capital return + $1-1.1/share ongoing = $1.1-1.3/share...

Hence TSR in the near-term - should this capital allocation policy be followed - be something like 13-16c of capital return + $1-1.1/share ongoing = $1.1-1.3/share...

Note that this itself is static and (imo) too low, bec $HUM.AX is now 'in play' (third party bidder) and there are large synergies when you combine loan books in this space (opex and revenue lines). Moreover I think a lot of these Aussie small-cap non-bank lenders look decent value in any case.

I will address the eventy angle in a subsequent 🧵. For now I will leave it here, we are pursuing Board renewal to achieve a proper capital allocation policy that not only returns a ton of excess capital in the near-term but also allows the equity to rerate simply inline w the sector (55-70% upside).

Please help me achieve this laudable goal/ GLTA. DYODD.

$HUM.AX

$HUM.AX

@threadreaderapp unroll

• • •

Missing some Tweet in this thread? You can try to

force a refresh