Nothing I say/tweet/emoji is investment advice, and is solely for entertainment only. Always DYODD, I am not your fiduciary!

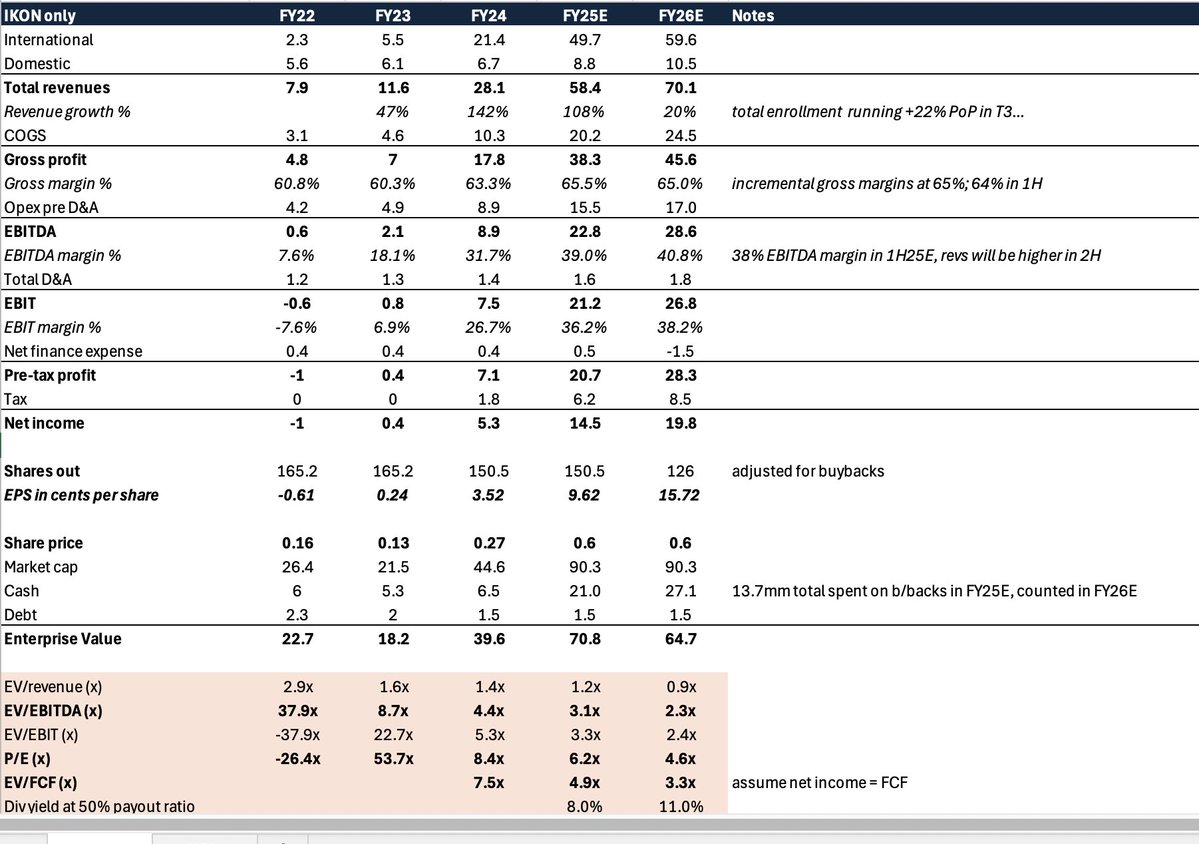

At 16.5c per share (the supposedly 'fair' buyback px) the implied mkt cap was $25mm 🤣🤣

At 16.5c per share (the supposedly 'fair' buyback px) the implied mkt cap was $25mm 🤣🤣

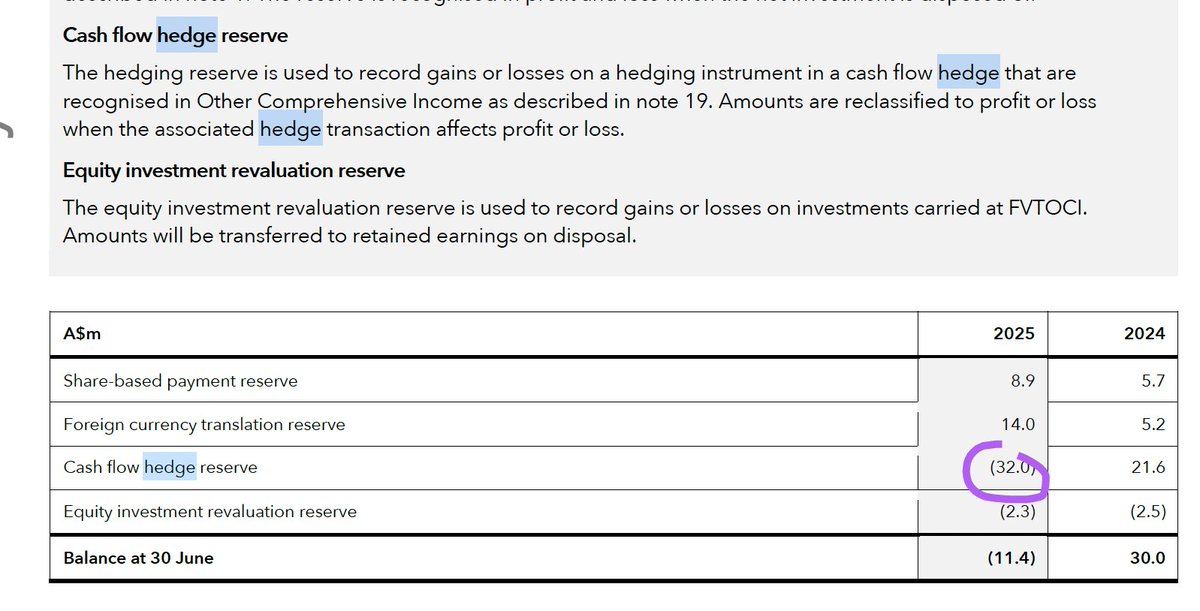

Given (I believe) TFG owns (at mids) 4.5mm shs of Ripple Labs, I think they are marking their Ripple shs at about $53/share (a big discount to private market transactions, given liquidity, etc).

Given (I believe) TFG owns (at mids) 4.5mm shs of Ripple Labs, I think they are marking their Ripple shs at about $53/share (a big discount to private market transactions, given liquidity, etc).

Still think another 10-15% upside nt in $AER but easy $$ has been made.

Still think another 10-15% upside nt in $AER but easy $$ has been made.