Japan is an interesting case in a lot of ways. It has a ton of domestic debt (and significant domestic financial assets) which generates heated concerns about its solvency/ ability to manage higher rates. But it is also a massive global creditor --

1/

1/

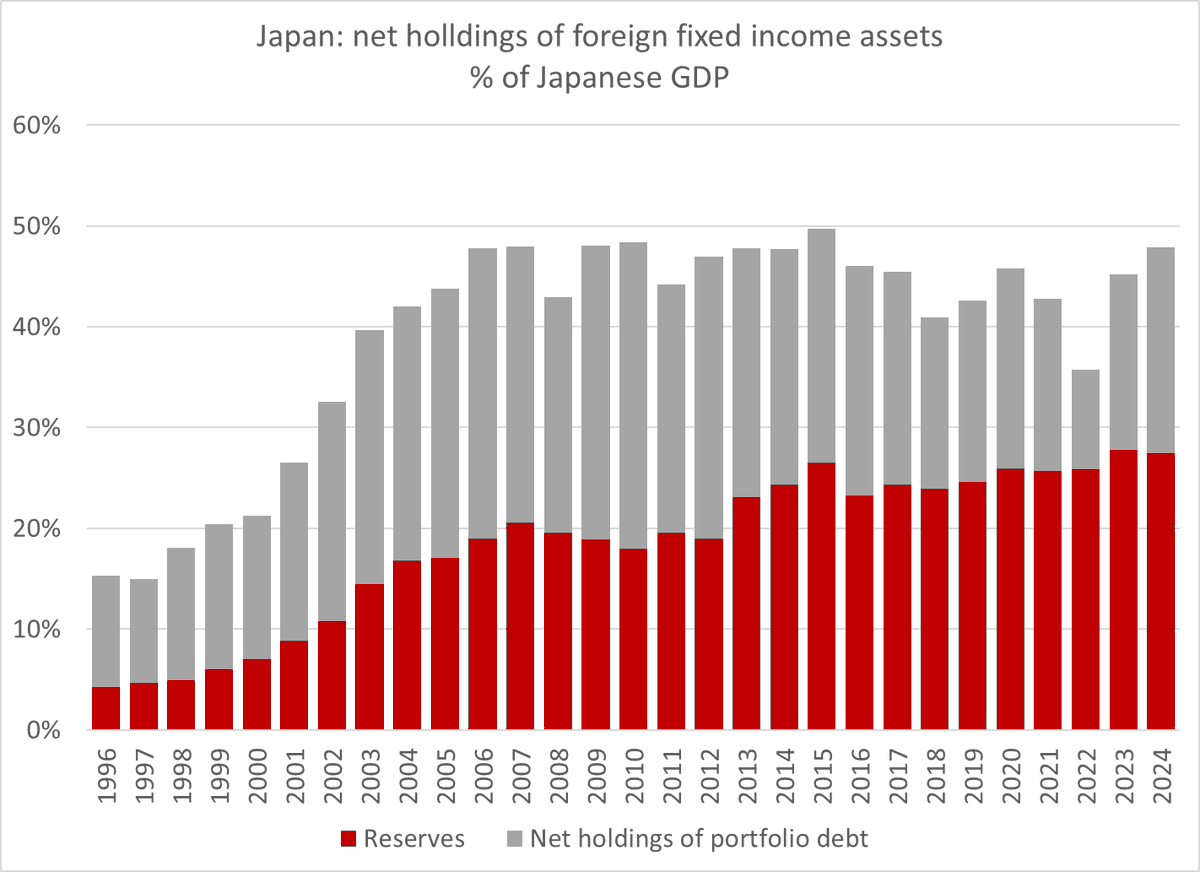

Japan's net holdings of bonds (net of foreign holdings of JGBs) is close to 50% of its GDP (a creditor position as big v GDP as the US net det position). That includes $1 trillion in bonds held in Japan's $1.175 trillion in reserves, + over $2 trillion in other holdings

2/

2/

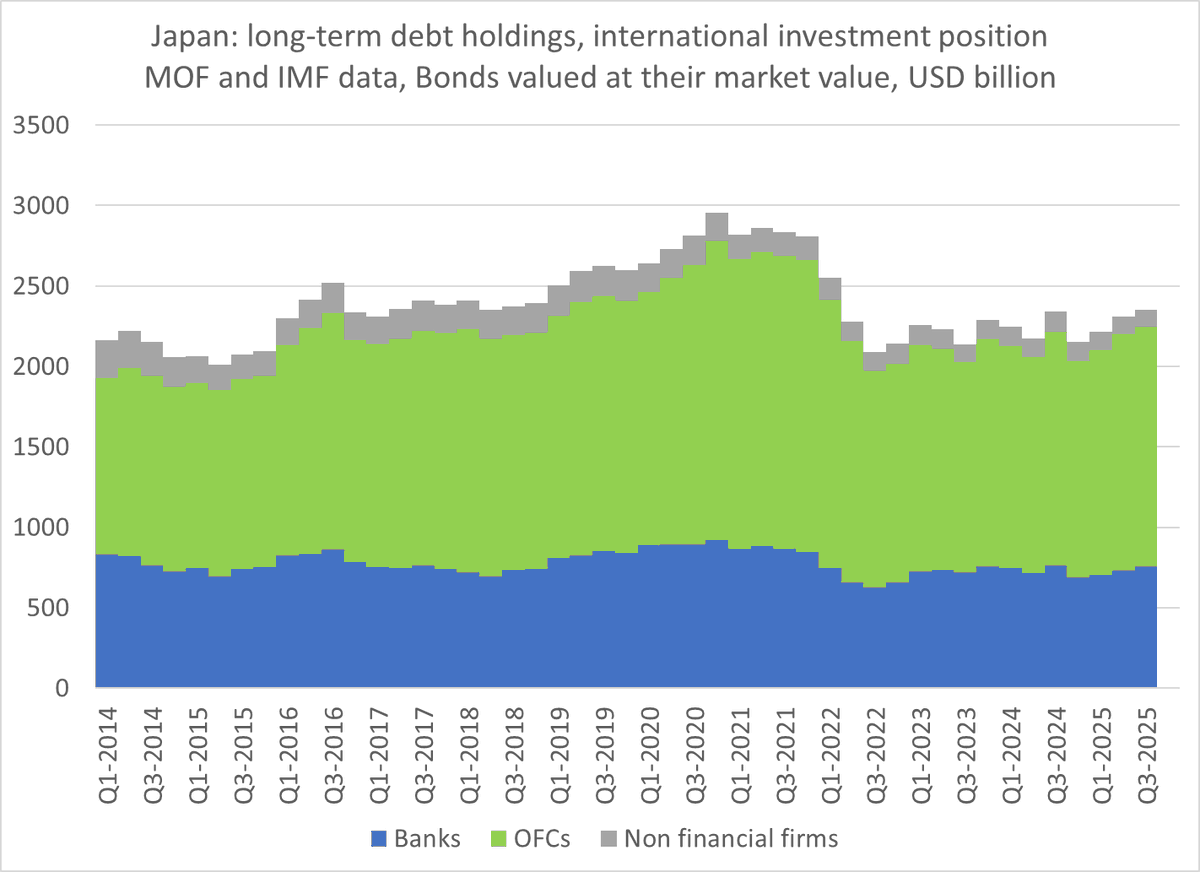

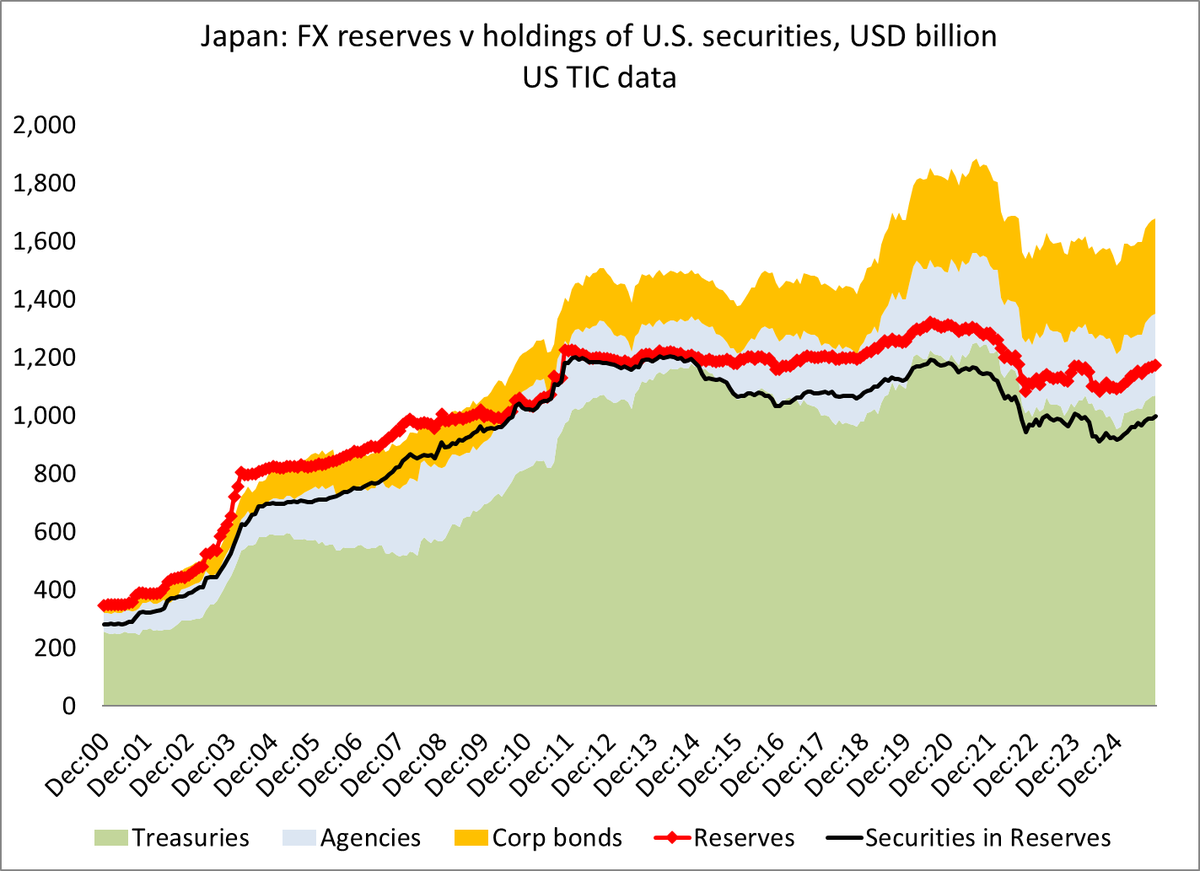

That translates into big holdings of US debt -- the MoF's Treasuries all show up in the US TIC data, but the corporate bonds held by the lifers, postbank and the GPIF are only partially captured in the US data b/c of third party management/ the use of EU custodians

3/

3/

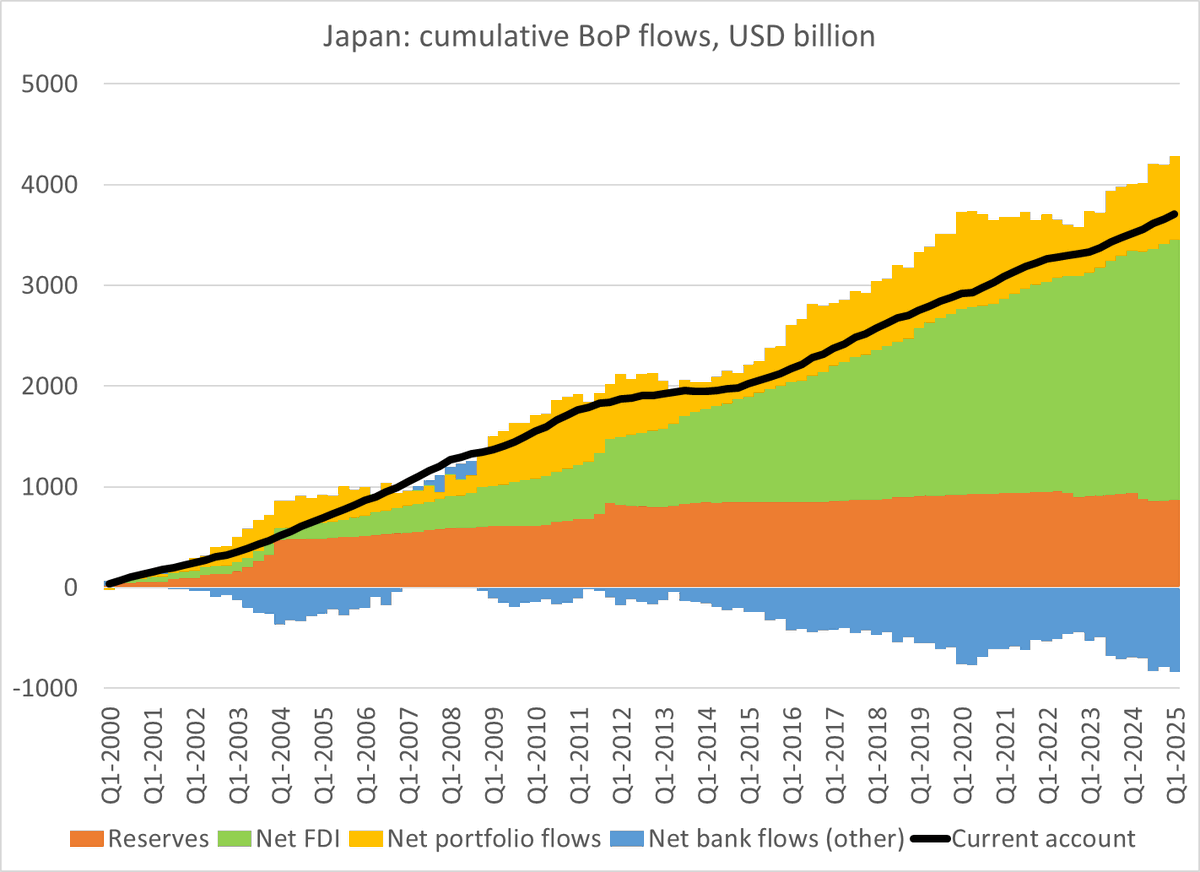

Japan has a big net FDI position as well -- so the net international investment position is much bigger than just the net position in bonds

4/

4/

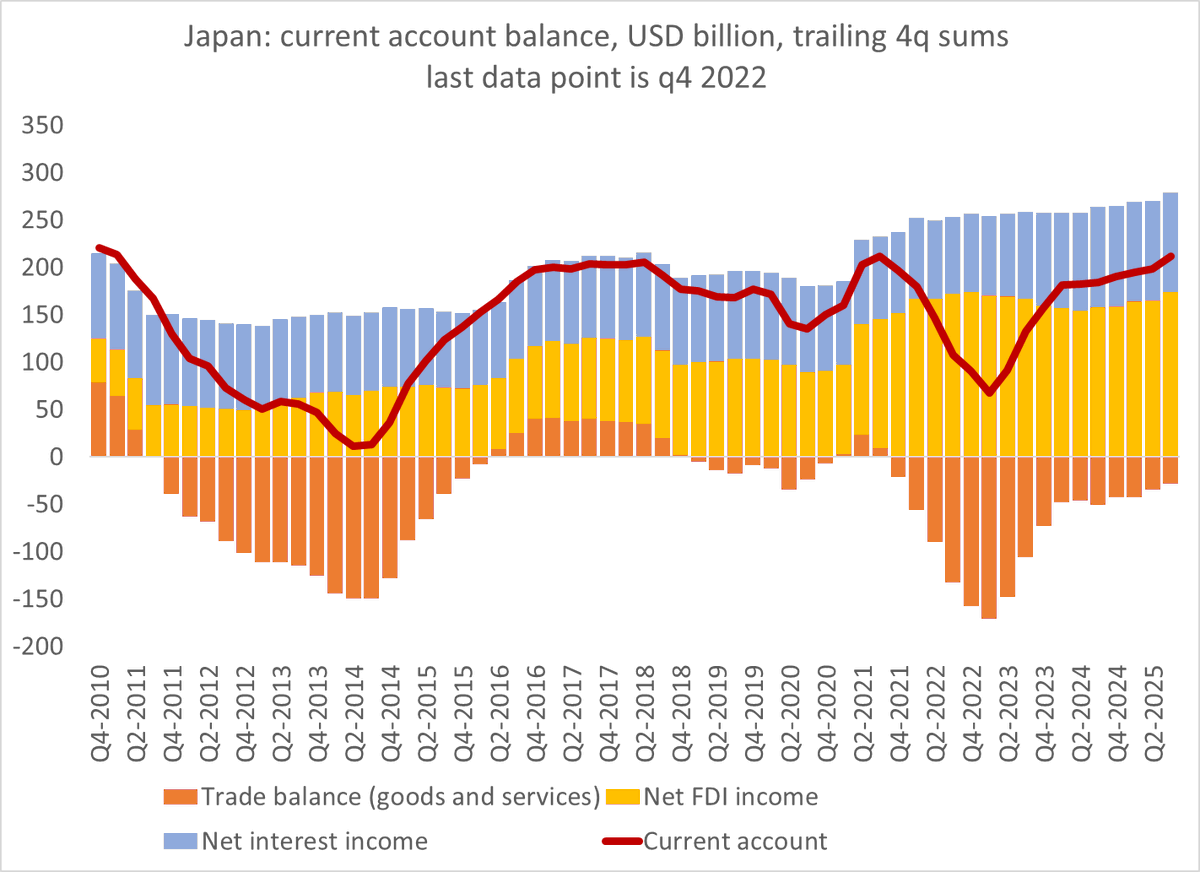

This translates into a 4.8 pp of GDP current account surplus even with the trade deficit -- all from investment income

5/

5/

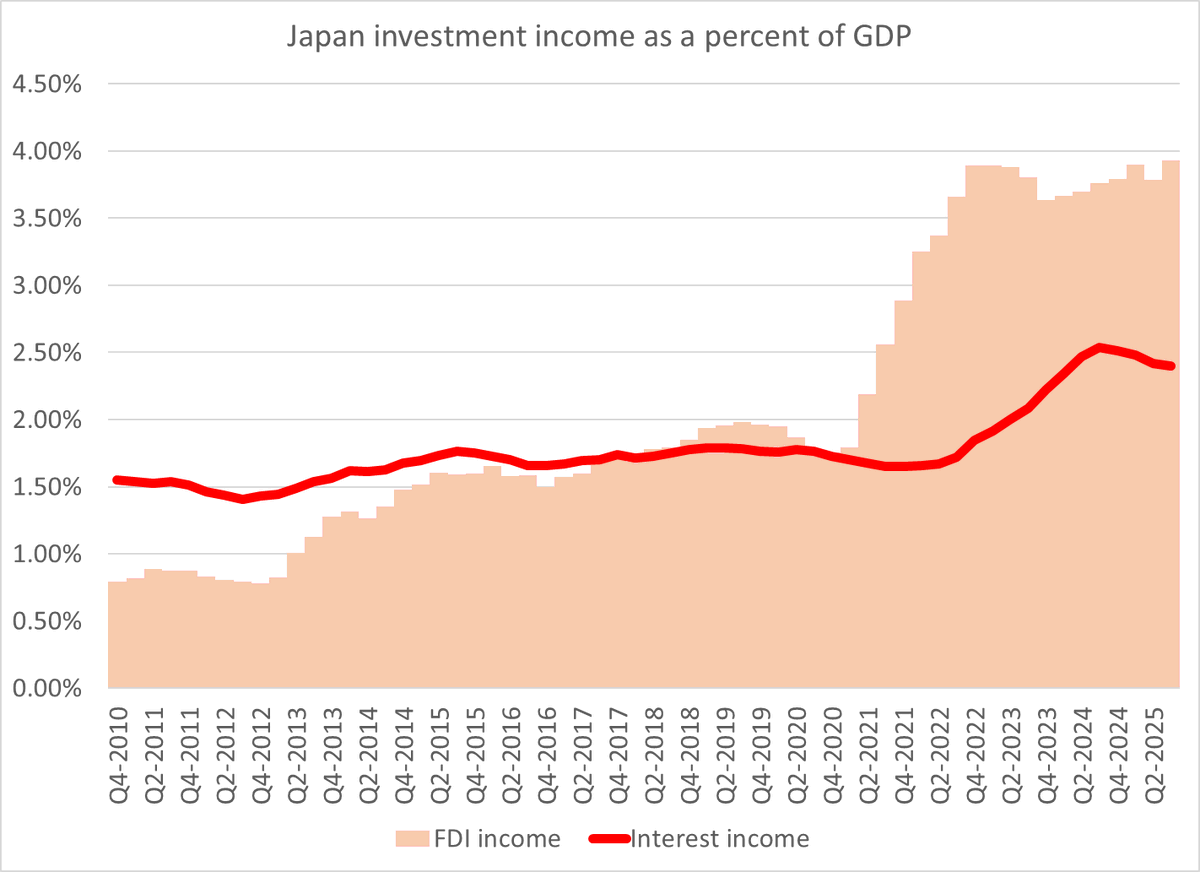

Coupon income from the bonds is now close to 2.5% of GDP - a real sum, even if it is smaller that the global profit of Japanese firms (Toyota etc)

6/

6/

The other key thing about Japan is that a large share of the country's foreign assets are held by the public sector:

MoF has $1.175 trillion in reserves

GPIF has over $900b in foreign assets, including over $450b in bonds

7/

gpif.go.jp/en/

MoF has $1.175 trillion in reserves

GPIF has over $900b in foreign assets, including over $450b in bonds

7/

gpif.go.jp/en/

Post bank has another $600b in foreign bonds (mostly corporate bonds, and mostly hedged) -- tho is it finally starting to raise its holdings of JGBS (its financial statement also shows how it became overweight in long-dated JGBs)

8/

jp-bank.japanpost.jp/en/ir/financia…

8/

jp-bank.japanpost.jp/en/ir/financia…

Sum that all up and it is a huge amount of foreign assets -- over $2.5 trillion, mostly unhedged ... and with massive mark to market gains that the public sector could realize to reduce its gross debt at any point in time!

9/

9/

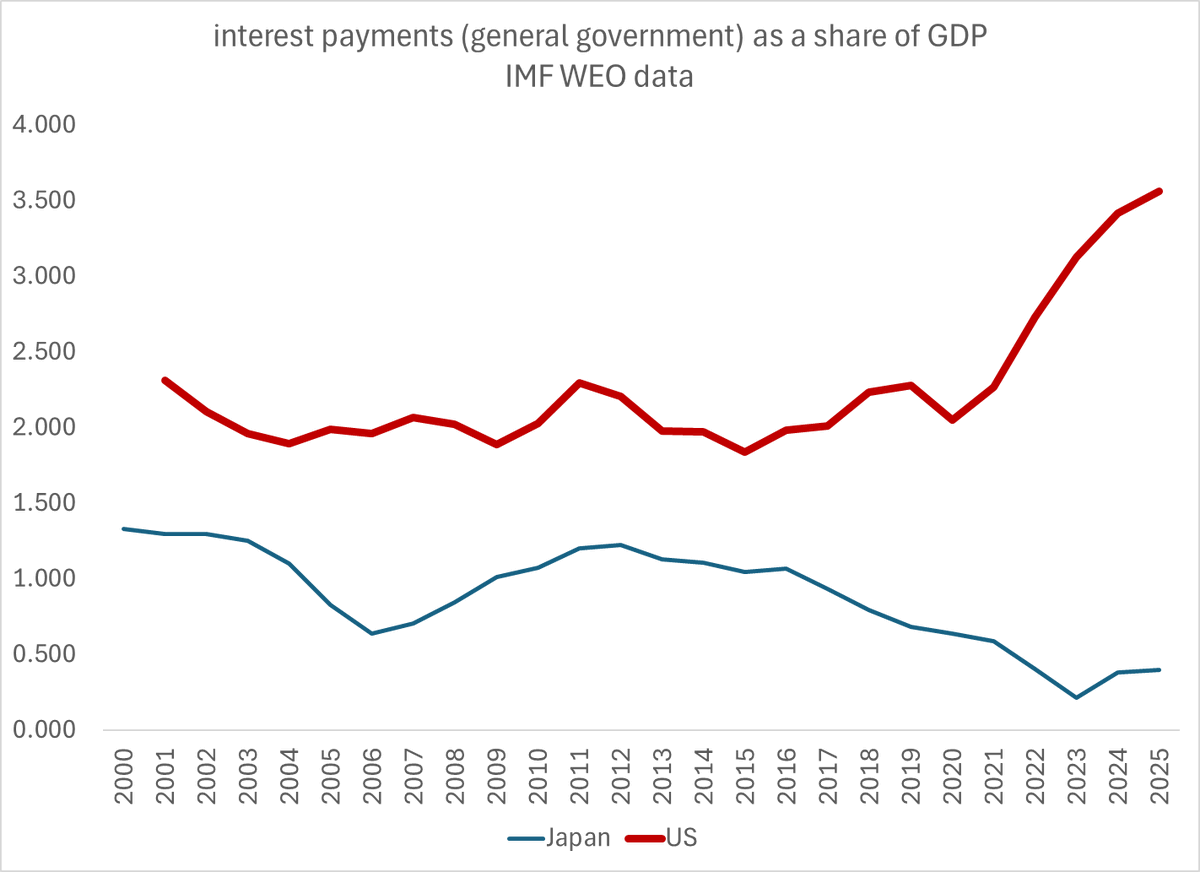

right now the interest income on Japan's foreign assets is more or less offsetting domestic interest payments, so net interest is tiny -- despite massive debts (the rate on yen liabilities tho is poised to rise a bit)

10/

10/

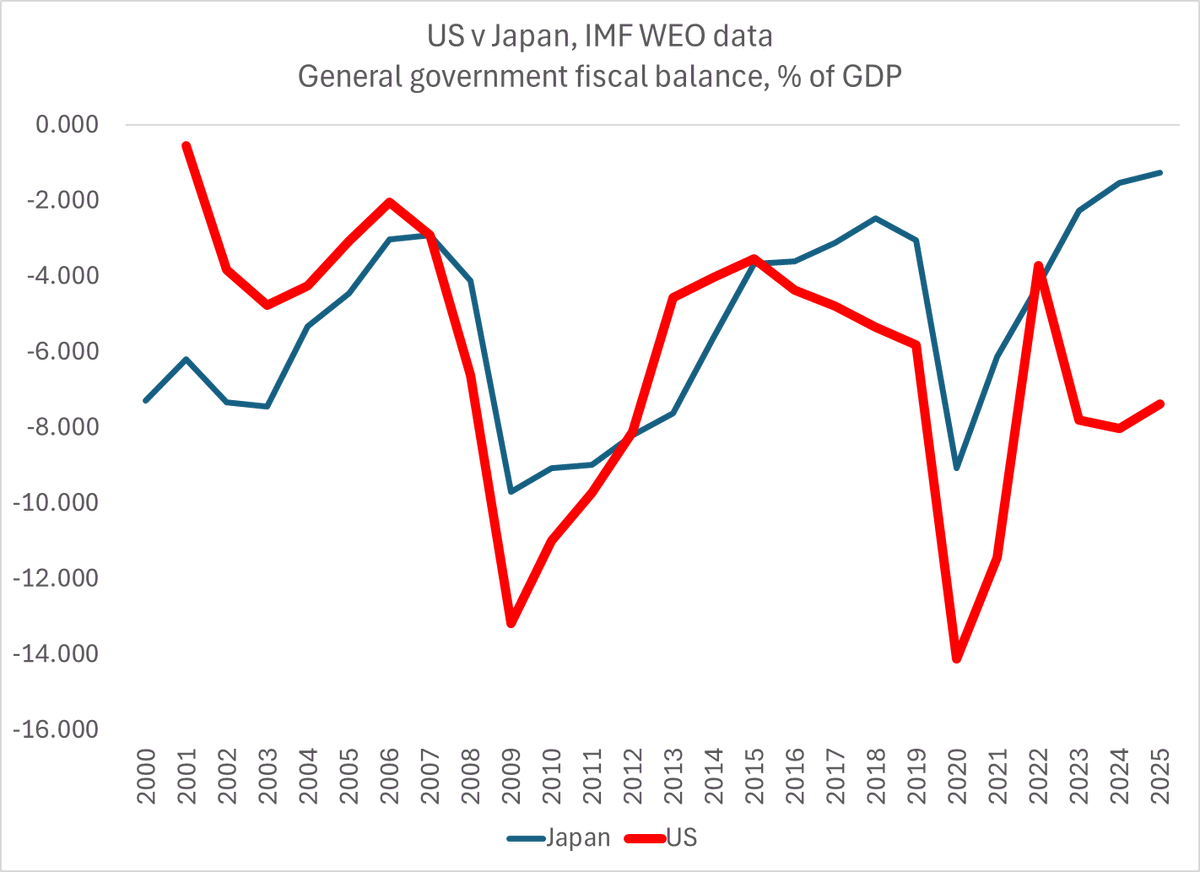

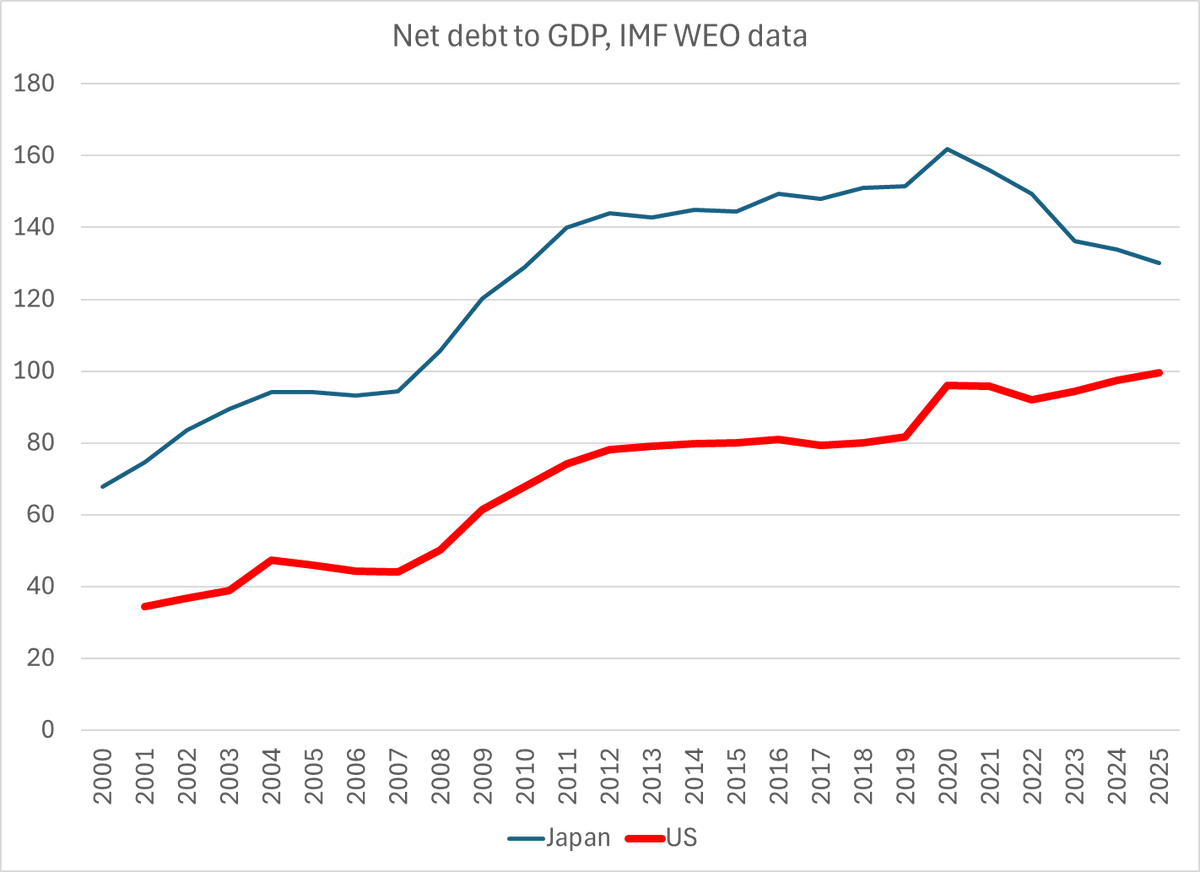

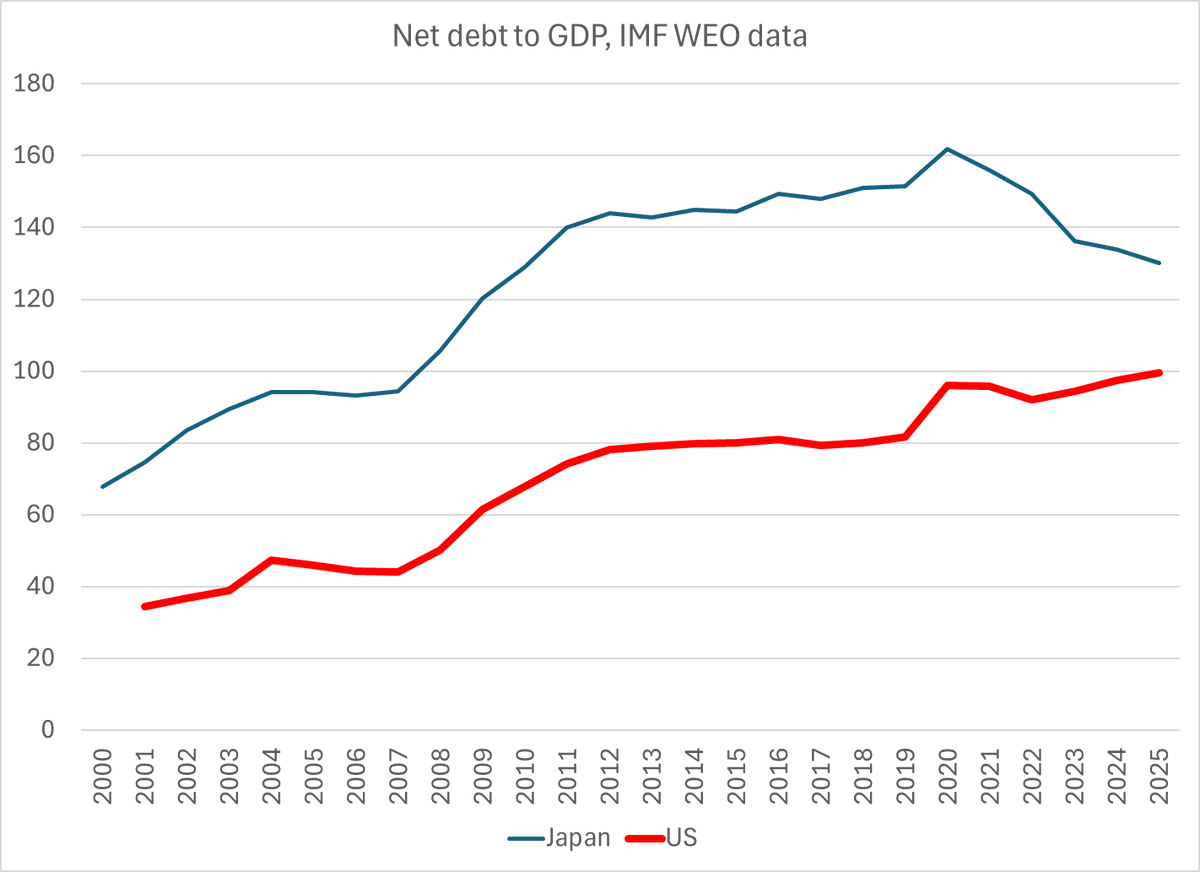

And capital gains on all of the foreign assets at MoF and the GPIF + smaller far fiscal deficits than in the US have brought net debt down to be within shooting distance of much of the rest of the G-7

11/

11/

So to my way of thinking, heavily influenced by the strength of Japan's external fx balance sheet, some of the concerns about Japan's proposed fiscal loosening are overdone. Takaichi isn't proposing half of what Trump has tweeted out ... and her starting point is better

12/

12/

And Japan has options that most countries with lots of fiscal debt don't have, as most countries with a large stock of domestic fiscal debt aren't also massive external creditors with big flow earnings on their offshore assets.

13/13

13/13

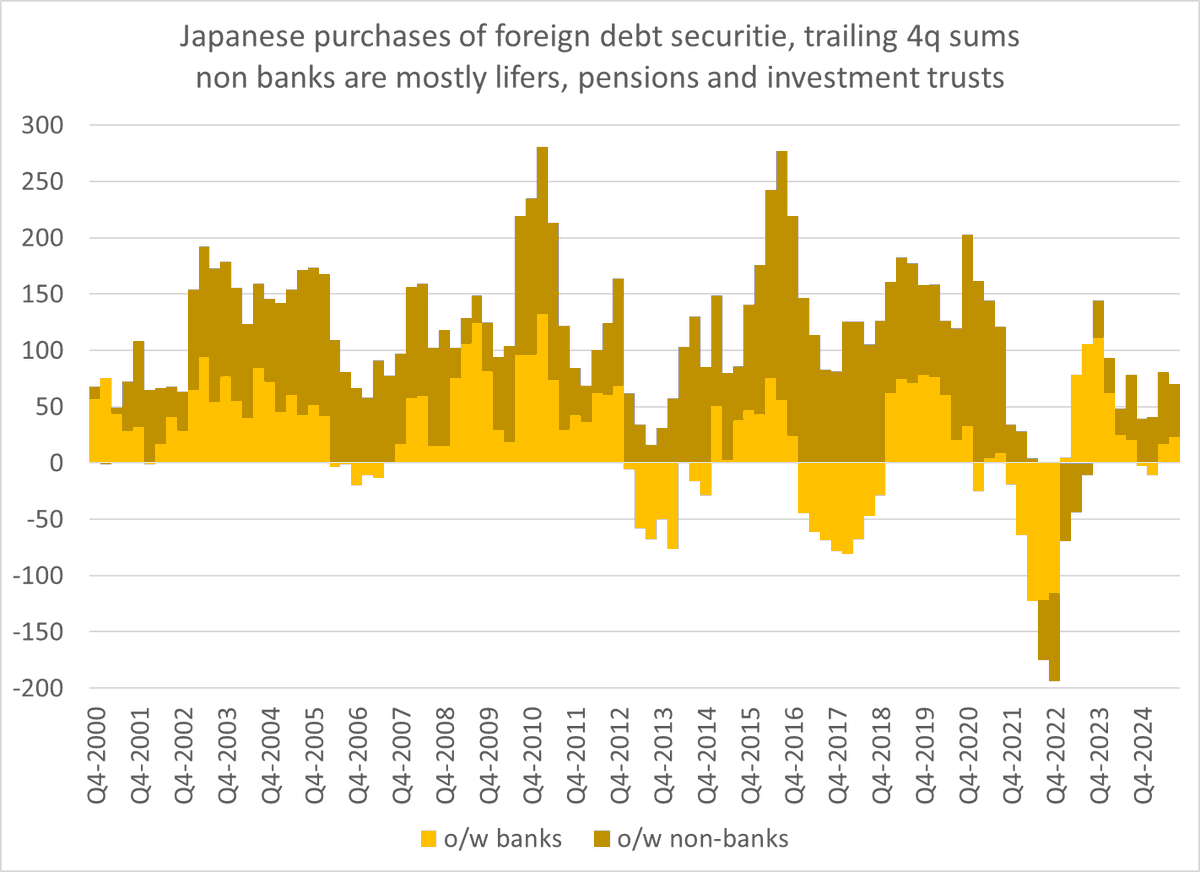

p.s. The flow out of Japan and into global bonds in recent years has been modest, a net flow of around $70 billion 0.2 pp of US GDP). That is much lower than pre-COVID.

• • •

Missing some Tweet in this thread? You can try to

force a refresh