Financial markets feel increasingly fraught to me, with the elements for a meaningful selloff coming into place. This threat is highest for stocks and corporate bonds, but even crypto, gold, and silver remain at risk despite recent pullbacks. Valuations are high. There are good fundamental reasons for this, but markets appear increasingly tainted by speculation. That is, investors are simply investing on the faith that prices will rise quickly in the future because they have in the recent past.

On the fundamentals, the economy’s performance is mixed. Real GDP is the strongest indicator, and it is growing just over 2%, below the economy’s potential, estimated to be near 2.5%. Employment has flat-lined, and unemployment continues to creep higher. Inflation, as measured by the Fed’s preferred consumer expenditure deflator, remains stubbornly and uncomfortably high at 3%. And there is no economic upside to the renewed chaos over tariffs and a looming military conflict with Iran.

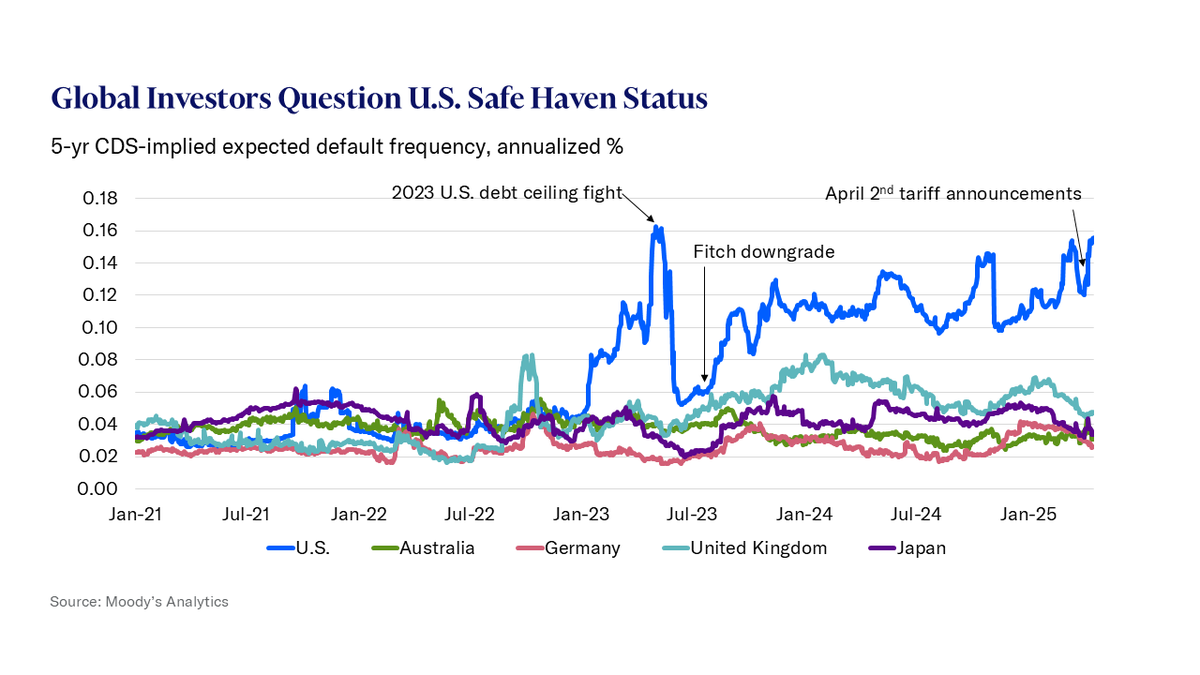

Then there is the fragile Treasury market. As the price-insensitive Federal Reserve and global investors have stepped away from the market, uber price-sensitive hedge funds playing a leveraged basis trade have stepped in. It’s not hard to imagine them running for the proverbial door all at once, and interest rates spike. The catalyst could be the nation’s massive budget deficits and funding needs, and global investors’ legitimate concerns about the safe-haven status of Treasuries in a fast de-globalizing economy.

I rarely weigh in on financial markets, as they generally reflect and are broadly consistent with economic conditions. But there are times when I feel markets are overdone and increasingly disconnected from the economy. Markets risk moving in a big way, causality is reversed, and falling asset prices threaten an already vulnerable economy. This is one of those times.

• • •

Missing some Tweet in this thread? You can try to

force a refresh