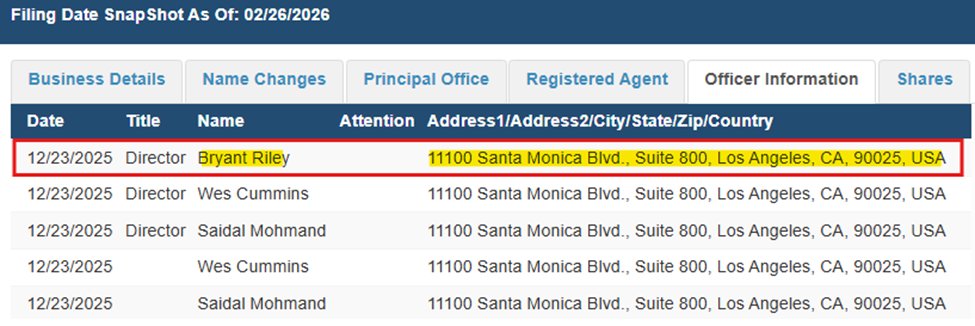

We are short $HIFS: we believe it is the $RILY of regional banks because it is over-leveraged, under-reserved, with a significant portion of its loan book underwater and/or in distress. $HIFS foreclosed two loans for $5.2m in January but did not disclose either of these loans as “non-performing” as of earnings ending 12/31/2025. We have found more than >$125m additional high risk, distressed loans in the D.C. area. We believe $HIFS lacks the liquidity, capital cushion, or earnings power to easily absorb the losses we believe are inevitable. We see potential downside of ~60% or more from capital erosion and multiple compression. Let’s take a tour.

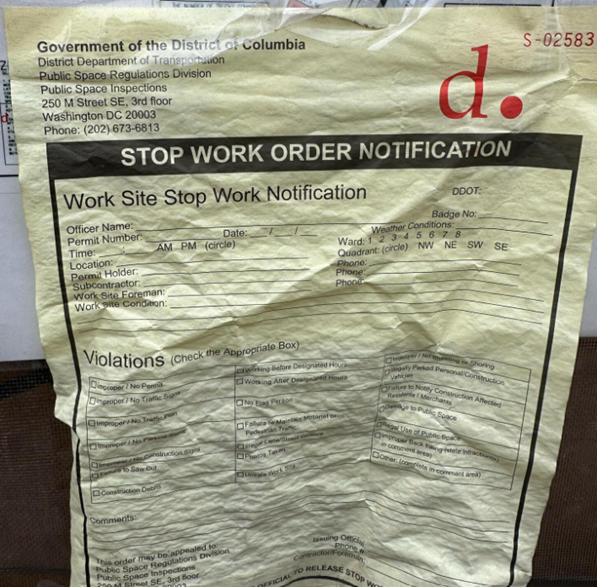

1701 Park Road NW, Washington, DC. One of the borrowers who entered foreclosure in January owns $47m worth of real estate backed by $HIFS. The largest loan is this “low-risk” $17m loan which is, in our view, a disaster. The borrower is being sued by multiple other lenders. This vacant and vandalized project has been hit with multiple stop work orders.

2637 16thSt NW, Washington, DC. This same borrower, who had one of his smaller $HIFS properties enter foreclosure in January has another “low-risk” $15m loan for a rehab project that appears completely stalled. In December, it was hit with a lien for unpaid masonry work. Our site visits, three months apart, revealed that the exact same pile of garbage has been sitting in the same spot the entire time...

50 M St NW, Washington, DC. It is 270 days delinquent and failed to sell in March 2025. $HIFS refuses to take any reserves for this $31m loan; however, the borrower has described this project as “infeasible” due to high financing and construction costs.

8008 Wisconsin Ave, Bethesda, MD. $HIFS's $15m loan was given in October 2023 but there has been no visible progress on this rehab. Other projects by this same borrower also appear to have stalled, according to our research. How is this project “low risk?”

Almost half of $HIFS earnings from 2023-2025 were mark-to-market gains on its securities portfolio. $HIFS's 13-F indicates that the primary driver of returns has been a large bet on $GOOG, which comprises ~40% of its reported 13-F portfolio. If $GOOG gets a cold, $HIFS gets pneumonia. What could go wrong?

@CitronResearch

@DonutShorts

@GuastyWinds

@blueorcainvest

@jacobadelman

@blalpert

@RealJimChanos

@FriendlyBearSA

@BreakoutPoint

@hibearnating

@ParrotCapital

@Seawolfcap

@QTRResearch

@muddywatersre

@ursustrades

@StockJabber

@kakashiii111

@wallstengine

@calvinfroedge

@tabbata

@GothamResearch

@ScorpionFund

@KerrisdaleCap

@thebankzhar

@DonutShorts

@GuastyWinds

@blueorcainvest

@jacobadelman

@blalpert

@RealJimChanos

@FriendlyBearSA

@BreakoutPoint

@hibearnating

@ParrotCapital

@Seawolfcap

@QTRResearch

@muddywatersre

@ursustrades

@StockJabber

@kakashiii111

@wallstengine

@calvinfroedge

@tabbata

@GothamResearch

@ScorpionFund

@KerrisdaleCap

@thebankzhar

• • •

Missing some Tweet in this thread? You can try to

force a refresh