Wolfpack Research is a short-biased activist research and due-diligence firm founded by Dan David. For personal/political views follow @Dan_David44

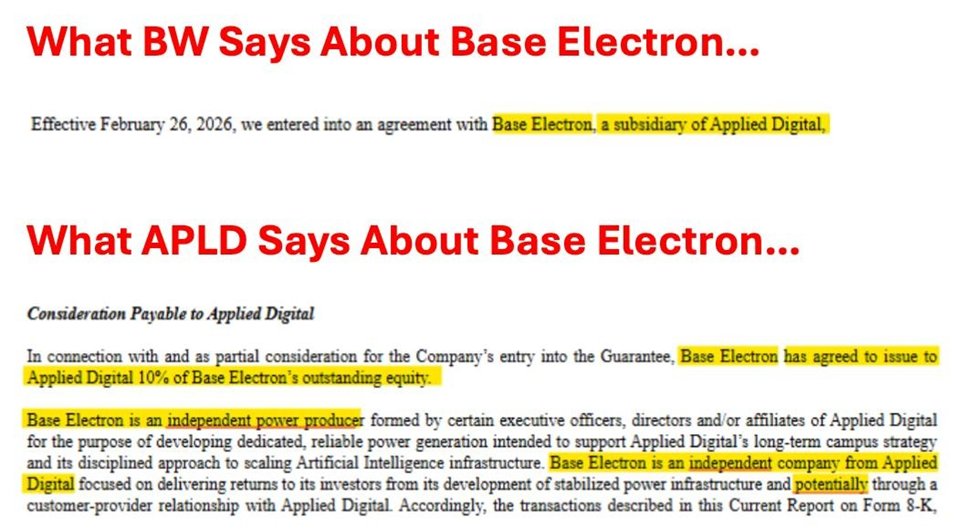

The first sign of trouble is that $BW calls Base Electron a “subsidiary” of $APLD, but this is contradicted by $APLD, who repeatedly says that it is an “independent” company and that it only owns 10% of the equity. Someone has got it wrong here, with think it’s $BW.

The first sign of trouble is that $BW calls Base Electron a “subsidiary” of $APLD, but this is contradicted by $APLD, who repeatedly says that it is an “independent” company and that it only owns 10% of the equity. Someone has got it wrong here, with think it’s $BW.

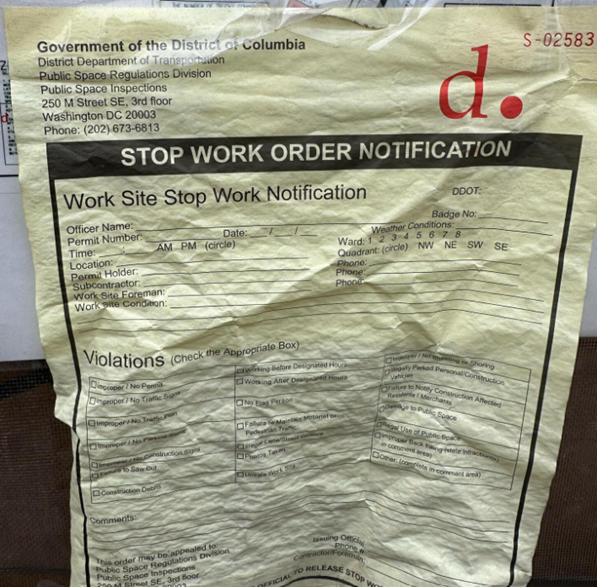

1701 Park Road NW, Washington, DC. One of the borrowers who entered foreclosure in January owns $47m worth of real estate backed by $HIFS. The largest loan is this “low-risk” $17m loan which is, in our view, a disaster. The borrower is being sued by multiple other lenders. This vacant and vandalized project has been hit with multiple stop work orders.

1701 Park Road NW, Washington, DC. One of the borrowers who entered foreclosure in January owns $47m worth of real estate backed by $HIFS. The largest loan is this “low-risk” $17m loan which is, in our view, a disaster. The borrower is being sued by multiple other lenders. This vacant and vandalized project has been hit with multiple stop work orders.

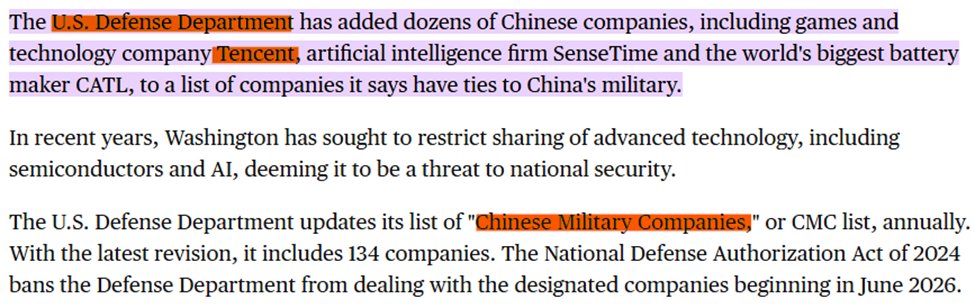

We learned from multiple sources that it is common knowledge in the industry that Datasection's mystery customer is China-based. We were told Datasection let the cat out of the bag that Tencent was its backer while it was pursuing financing from Japanese banks, and that the banks quickly shut their doors due to the horrendous reputational risk. We suspect Chinese involvement was also the reason Datasection changed auditors from PwC Japan to a small, relatively unknown auditor.

We learned from multiple sources that it is common knowledge in the industry that Datasection's mystery customer is China-based. We were told Datasection let the cat out of the bag that Tencent was its backer while it was pursuing financing from Japanese banks, and that the banks quickly shut their doors due to the horrendous reputational risk. We suspect Chinese involvement was also the reason Datasection changed auditors from PwC Japan to a small, relatively unknown auditor.

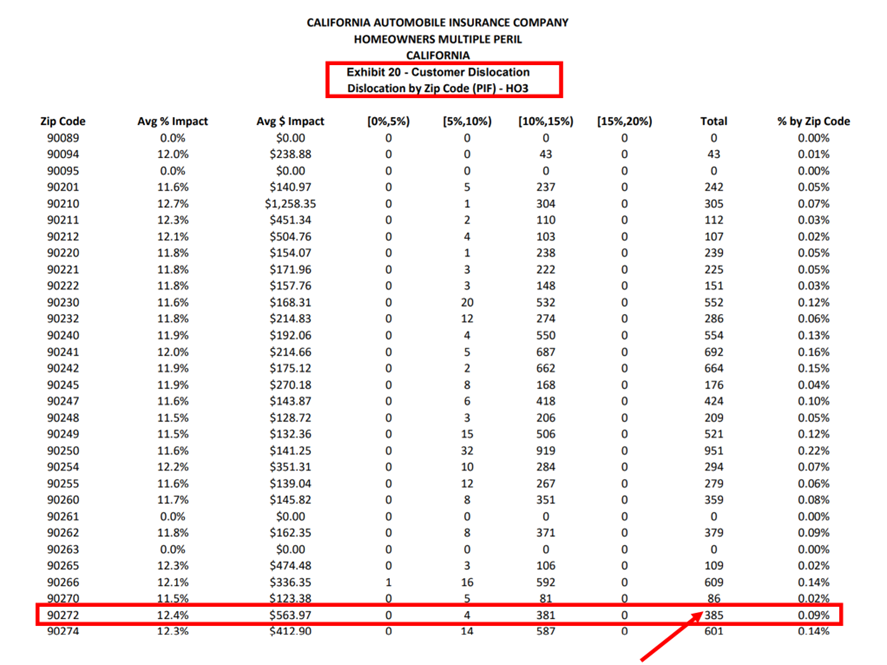

Using $MCY's rate filings, we see $MCY had ~1,300 home and landlord policies in force as of June 2024 between Altadena and the Pacific Palisades.

Using $MCY's rate filings, we see $MCY had ~1,300 home and landlord policies in force as of June 2024 between Altadena and the Pacific Palisades.

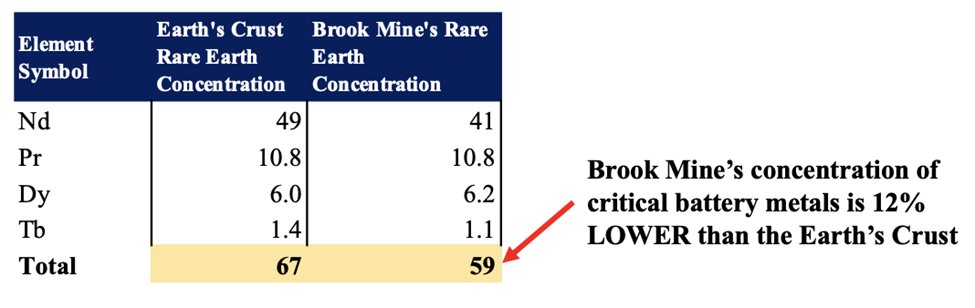

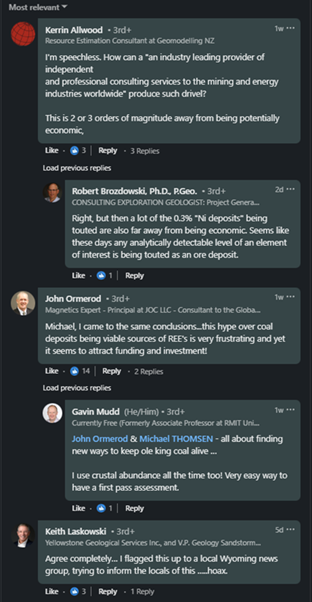

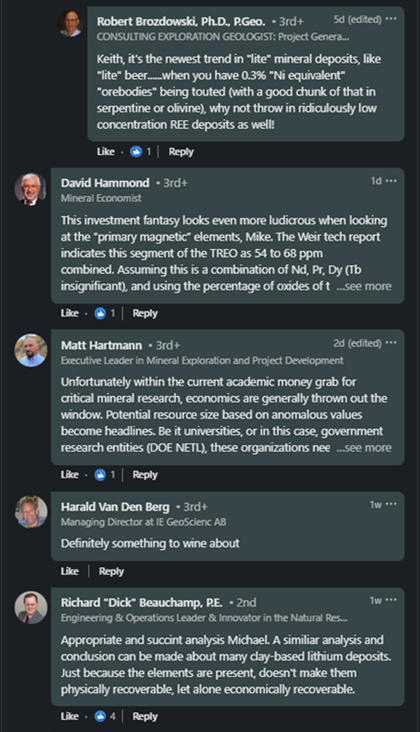

2/ A number of mining professionals appear to have identified the same problem with $METC claims:

2/ A number of mining professionals appear to have identified the same problem with $METC claims:

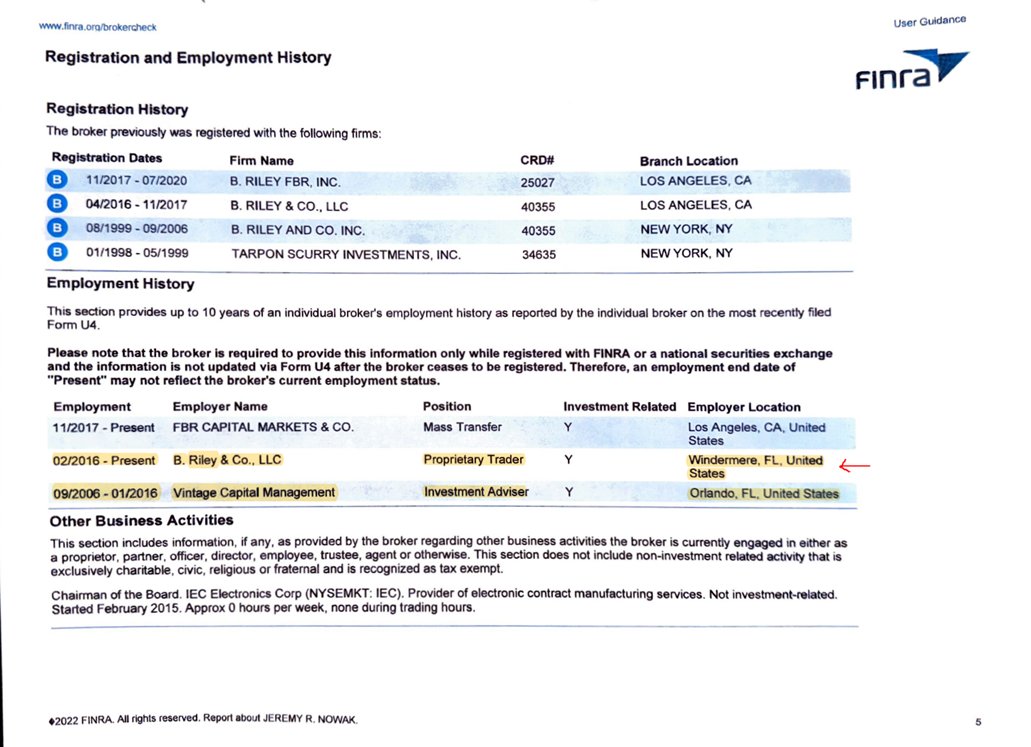

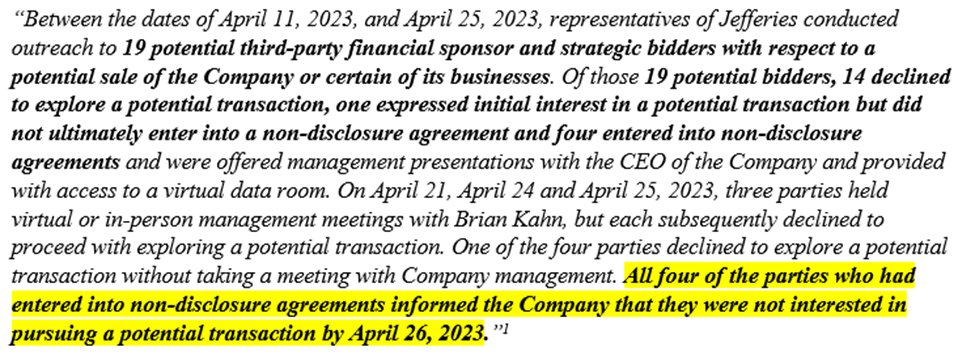

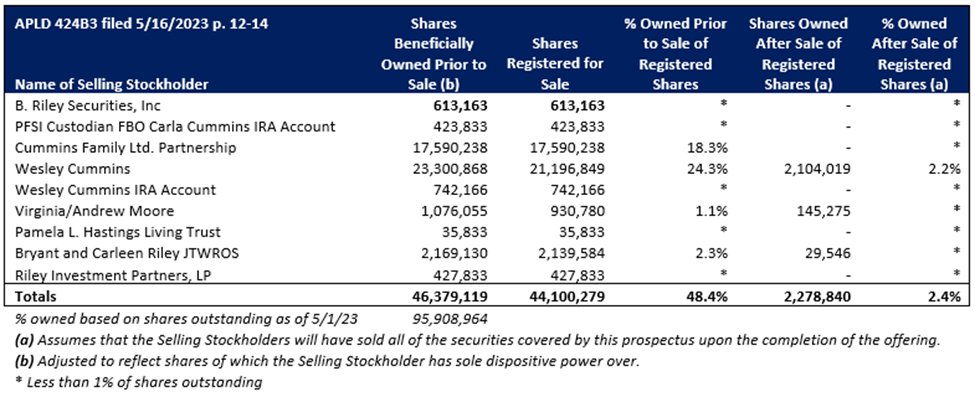

2/ $RILY should’ve known Kahn had been accused of misusing funds in a civil suit from 2022. Yet, $RILY negotiated directly with Kahn anyway in order to get a deal done to take his failing public company $FRG private at $30/share

2/ $RILY should’ve known Kahn had been accused of misusing funds in a civil suit from 2022. Yet, $RILY negotiated directly with Kahn anyway in order to get a deal done to take his failing public company $FRG private at $30/share

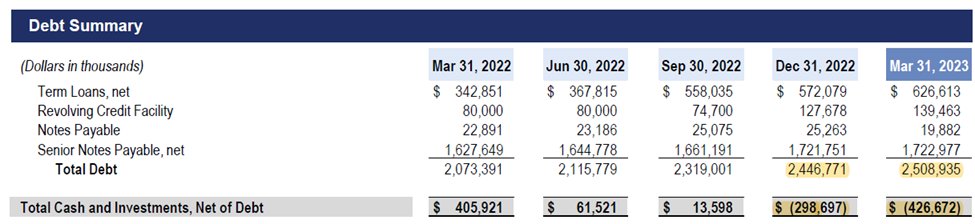

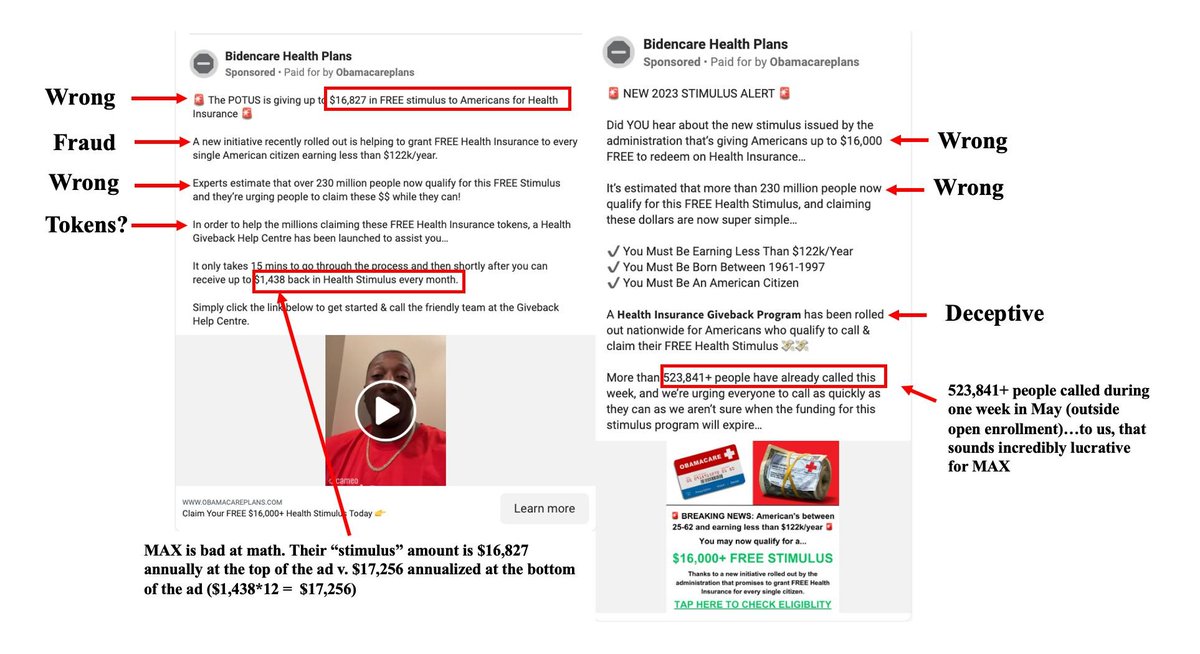

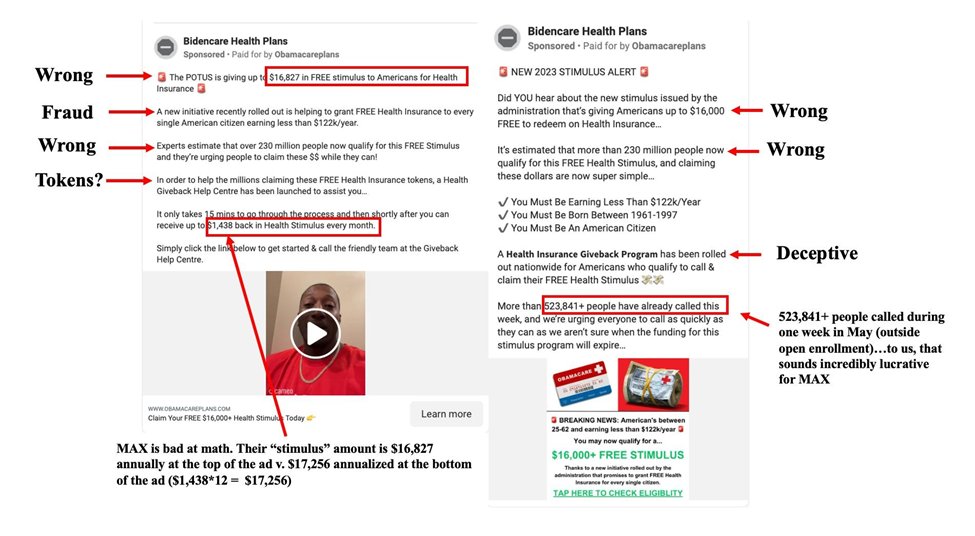

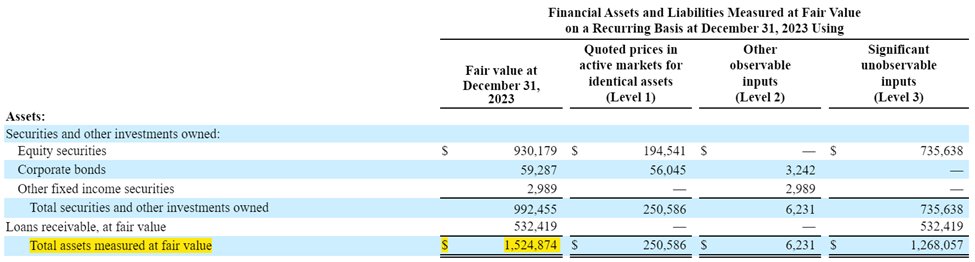

2/ Mgmt would have us believe $RILY is on the upswing, but a closer look at the numbers indicate that it is not:

2/ Mgmt would have us believe $RILY is on the upswing, but a closer look at the numbers indicate that it is not: