Las Vegas apartment vacancies are spiking.

And landlords are not happy.

7.6% of Vegas apartments are now sitting vacant, the highest level in nearly 10 years.

(Triple the pandemic low of 2.4%).

4 years ago, rents were soaring, and there was no availability.

Now they're cutting rents aggressively and giving concessions just to get tenants through the door.

A potentially ominous sign for Vegas' overall housing market in 2026.

And landlords are not happy.

7.6% of Vegas apartments are now sitting vacant, the highest level in nearly 10 years.

(Triple the pandemic low of 2.4%).

4 years ago, rents were soaring, and there was no availability.

Now they're cutting rents aggressively and giving concessions just to get tenants through the door.

A potentially ominous sign for Vegas' overall housing market in 2026.

1) I like looking at a local area's rental market as an additional bellwether of where things are heading.

If vacancies are rising, and rents are getting cut, it's a suggestion that the broader housing market is oversupplied.

And that general housing deflation could be on the way (as if the case in Las Vegas).

If vacancies are rising, and rents are getting cut, it's a suggestion that the broader housing market is oversupplied.

And that general housing deflation could be on the way (as if the case in Las Vegas).

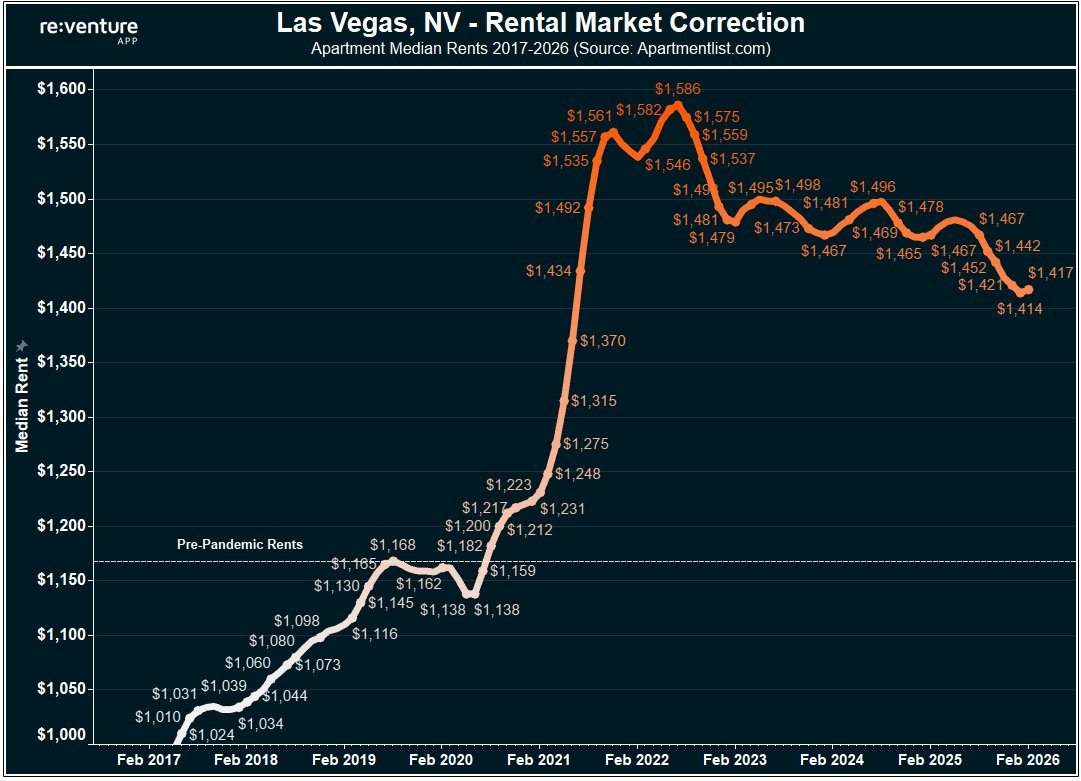

2) Data from Apartment List shows that apartment rents in Vegas are down about 10% from their post-pandemic peak in 2022.

Back then, they were at $1,586 per apartment.

Now they're at $1,417.

(note that this is still 21% above pre-pandemic rents)

Back then, they were at $1,586 per apartment.

Now they're at $1,417.

(note that this is still 21% above pre-pandemic rents)

3) In some communities, the cuts could be even steeper.

Here is an apartment community that has 1-month free.

On 600 SF studios at $725/month base rent.

($664 net of concession)

Here is an apartment community that has 1-month free.

On 600 SF studios at $725/month base rent.

($664 net of concession)

4) The reason why this is happening is multi-fold.

First, Las Vegas is experiencing a slowdown in net migration after the pandemic, both from domestic and international sources. This is crimping housing demand.

Second, the affordability metrics in Vegas became skewed after the pandemic, and many local renters, especially those on the lower end of the income spectrum, became priced out.

Third, the local economy in Las Vegas is starting to struggle. Job growth in the metro just went into negative YoY territory for only the 4th time in the last 35 years.

First, Las Vegas is experiencing a slowdown in net migration after the pandemic, both from domestic and international sources. This is crimping housing demand.

Second, the affordability metrics in Vegas became skewed after the pandemic, and many local renters, especially those on the lower end of the income spectrum, became priced out.

Third, the local economy in Las Vegas is starting to struggle. Job growth in the metro just went into negative YoY territory for only the 4th time in the last 35 years.

5) Nevada non-farm payrolls hit -0.6% YoY in December 2025, which is the first negative reading since the pandemic.

And only the 4th since 1992.

Indicating how robust Vegas' job growth usually is.

And only the 4th since 1992.

Indicating how robust Vegas' job growth usually is.

6) But no longer. Slower job growth, due to reduced tourist demand and potentially lower immigration, is weighing the rental market.

At the same time, there's been a marked slowdown in migration from other U.S. states, which is causing a reduction in home sales and buyer demand.

In fact - demand to buy houses in Vegas in Jan 2026 was 43% below the pandemic peak.

At the same time, there's been a marked slowdown in migration from other U.S. states, which is causing a reduction in home sales and buyer demand.

In fact - demand to buy houses in Vegas in Jan 2026 was 43% below the pandemic peak.

7) Home values are now also officially dropping in Vegas' housing market. They're down -2.2% YoY.

But still up 35.8% over the last five years.

But still up 35.8% over the last five years.

8) The value drops are getting especially intense in certain ZIP codes.

Some areas are down over 6% in the last year, according to Zillow's value index, which is a big drop for just one year.

Some areas are down over 6% in the last year, according to Zillow's value index, which is a big drop for just one year.

9) To see our forecasts on the Vegas housing market, and to arm yourself with the right data before making a big purchase in 2026, head to and upgrade to a premium plan.

Forecasts are available for nearly every ZIP code in the U.S., and are updated monthly based on the underlying data in each market.reventure.app/mobile

Forecasts are available for nearly every ZIP code in the U.S., and are updated monthly based on the underlying data in each market.reventure.app/mobile

• • •

Missing some Tweet in this thread? You can try to

force a refresh