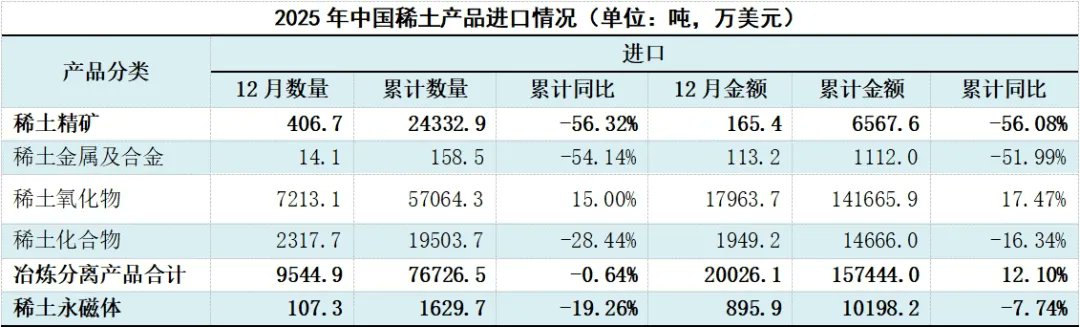

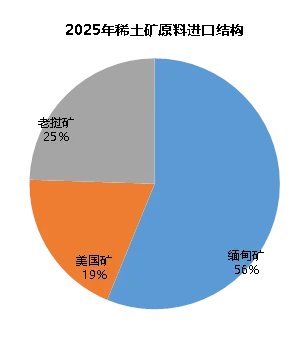

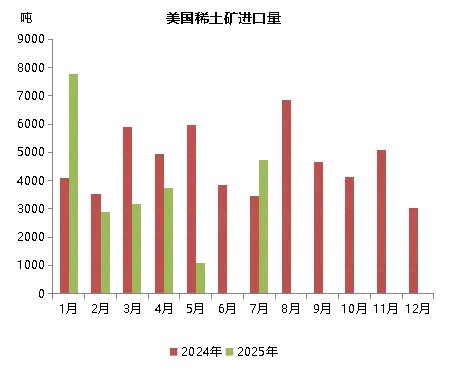

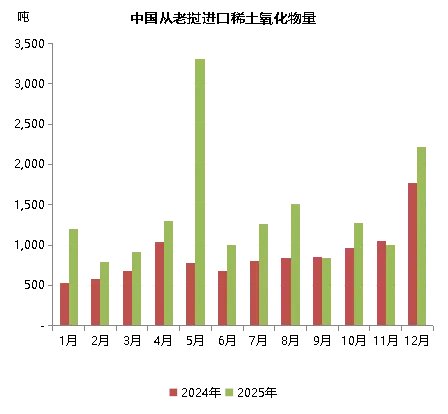

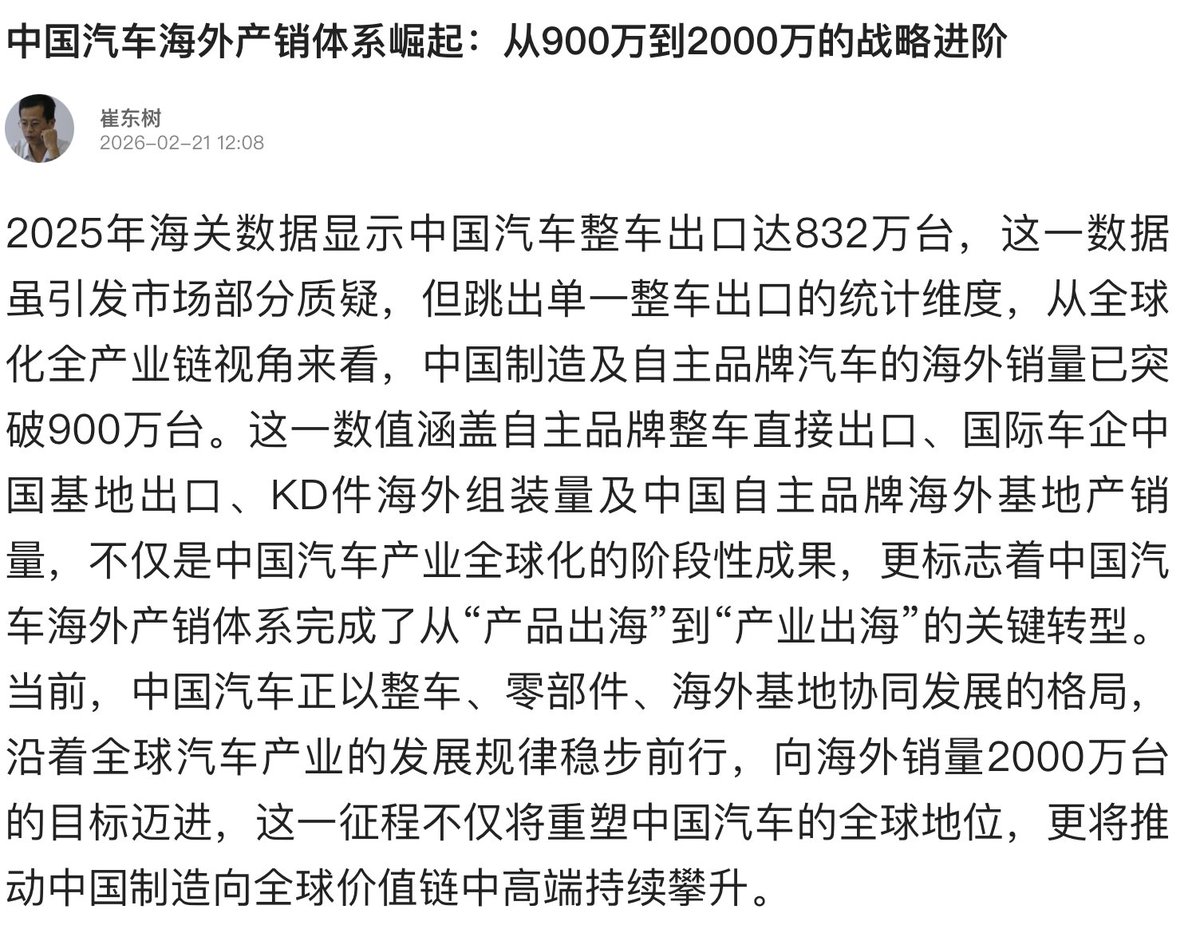

Update on Iran's attack tempo:

Its attack tempo noticeably slowed down earlier this wk as it shifted to longer range & more powerful BM while reducing attacks on GCC countries, especially UAE.

But that look to have changed last 2 days as Saudis & Jordan are getting attention

Its attack tempo noticeably slowed down earlier this wk as it shifted to longer range & more powerful BM while reducing attacks on GCC countries, especially UAE.

But that look to have changed last 2 days as Saudis & Jordan are getting attention

A simple look at the US tanker fleet action would point to the importance of Saudi Arabia, Jordan & Iraq toward continually supporting Coalition strikes on Iran.

As such, Iran has dialed up attacks on US bases & radar/command sites in this line.

As such, Iran has dialed up attacks on US bases & radar/command sites in this line.

It had some successes as 5 tankers were hit in the Prince Sultan AFB earlier while a huge contingent of USAF aircraft (including KC135 & E3).

They are defended by Saudi's immense air defense system. As such, Iran is also attacking oil facility to expend precious interceptors.

They are defended by Saudi's immense air defense system. As such, Iran is also attacking oil facility to expend precious interceptors.

At the same time, attacks on Jordan has really picked up as it gained importance in this conflict after the nearby military bases got shelled really hard.

The huge concentration of bases mean that hitting them probably gives a good missile to damage ratio for Iran.

The huge concentration of bases mean that hitting them probably gives a good missile to damage ratio for Iran.

Iran's proxy in Iraq has picked up attacks on US bases in Erbil but also Basra.

Given the huge Shiite presence in Iraq + proximity to Iran, it seems just a matter of time b4 resistance gets overcome here.

Iran conserved some fire this wk as its proxy is doing all the work here.

Given the huge Shiite presence in Iraq + proximity to Iran, it seems just a matter of time b4 resistance gets overcome here.

Iran conserved some fire this wk as its proxy is doing all the work here.

The attacks on UAE & Bahrain have slowed down but not stopped. It seems like US forces in those 2 countries have shifted out of the bases & attacking Iran w/ Himars from civilian areas.

Iran has shifted attacks to really go after those areas + infrastructure to hurt UAE/Bahrain

Iran has shifted attacks to really go after those areas + infrastructure to hurt UAE/Bahrain

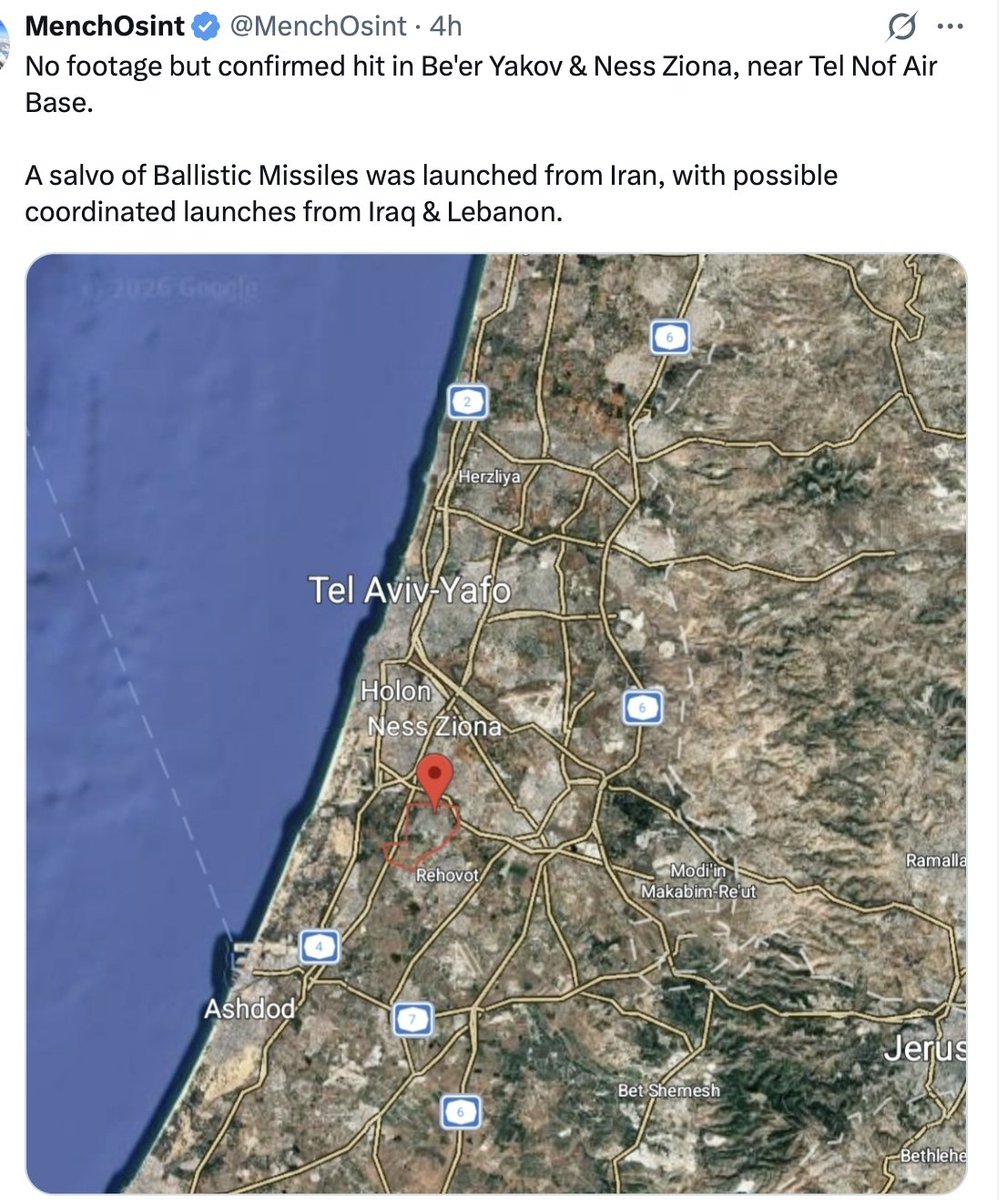

If we shift our attention back to Israel, it seems like attacks on the major military bases have picked up recently. They seemed to have concentrate on Tel Aviv & Haifa earlier, but some initial targets are likely destroyed.

So, target now is toward suppressing IAF operations.

So, target now is toward suppressing IAF operations.

It should be obvious by now that Iran is getting significant intel help from both Russia/China w/ both HUMINT & satellites.

It looks like China has a live view of the conflict & is really studying up on what's happening here.

It looks like China has a live view of the conflict & is really studying up on what's happening here.

https://x.com/BabakVahdad/status/2031815721509072990

So what do I think will happen next wk?

Well, GCC + Israel have clearly not run out of AD missiles yet. Iran's firing rate has slowed down & interceptors are still getting launched.

Until Iran can suppress IAF & push USAF out of Saudi Arabia, they will continue to get hammered.

Well, GCC + Israel have clearly not run out of AD missiles yet. Iran's firing rate has slowed down & interceptors are still getting launched.

Until Iran can suppress IAF & push USAF out of Saudi Arabia, they will continue to get hammered.

The obvious implication of USAF leaving this many military aircraft in Prince Sultan Airbase is that more of them will get damaged as Iran really shifts its focus toward Saudi Arabia & Jordan.

• • •

Missing some Tweet in this thread? You can try to

force a refresh