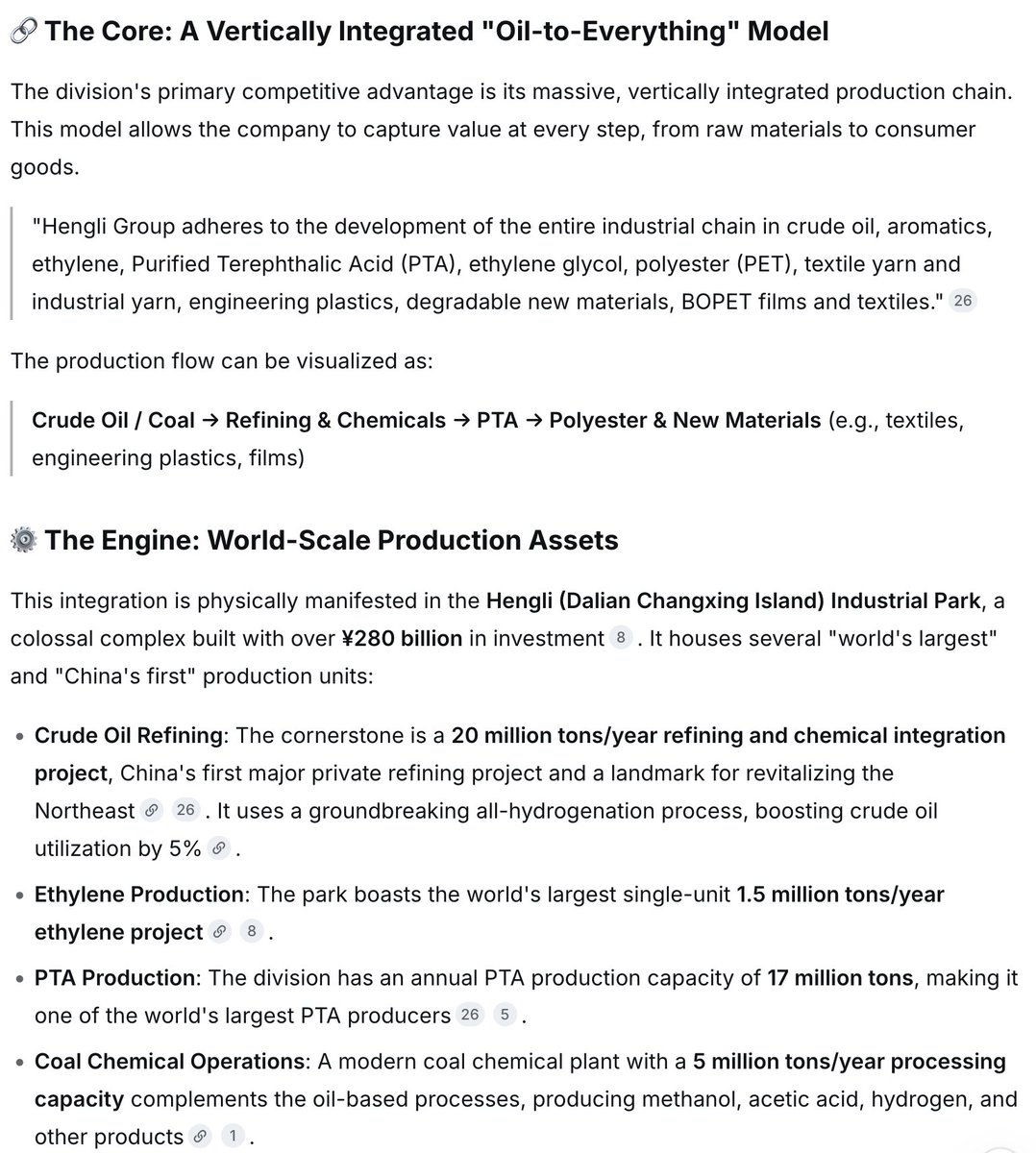

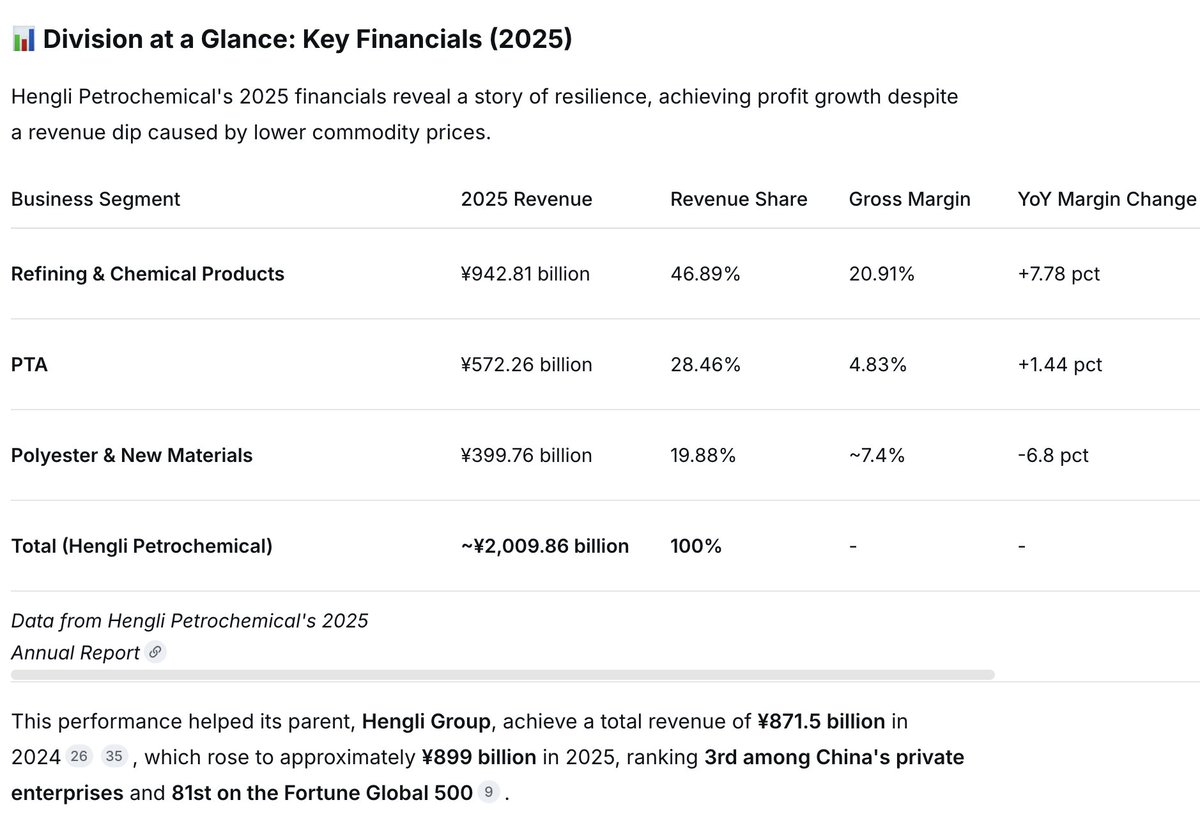

Hengli in Dalian Changxing Island was built w/ 280B RMB in total investment. Dalian is 1 of China's 7 major petrochem base. 20mt/yr of refining, 1.5mt/yr Ethylene, 17mt of PTA + 5mt/yr of coal chemical.

Hengli in Dalian Changxing Island was built w/ 280B RMB in total investment. Dalian is 1 of China's 7 major petrochem base. 20mt/yr of refining, 1.5mt/yr Ethylene, 17mt of PTA + 5mt/yr of coal chemical.

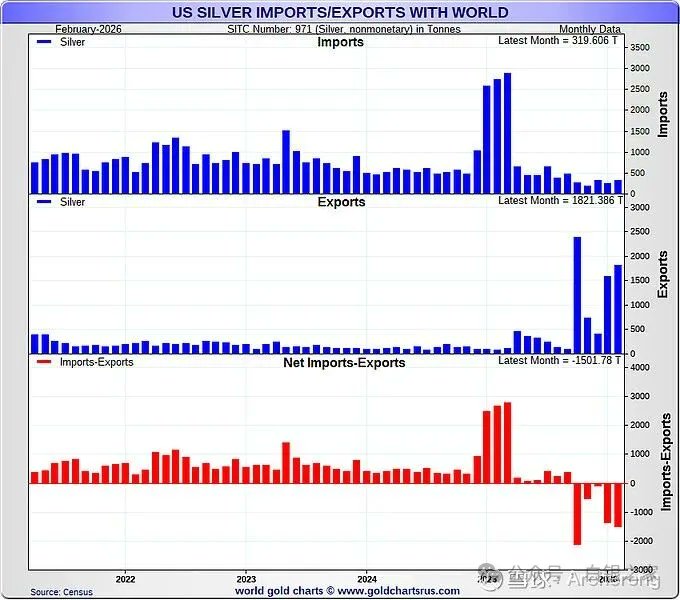

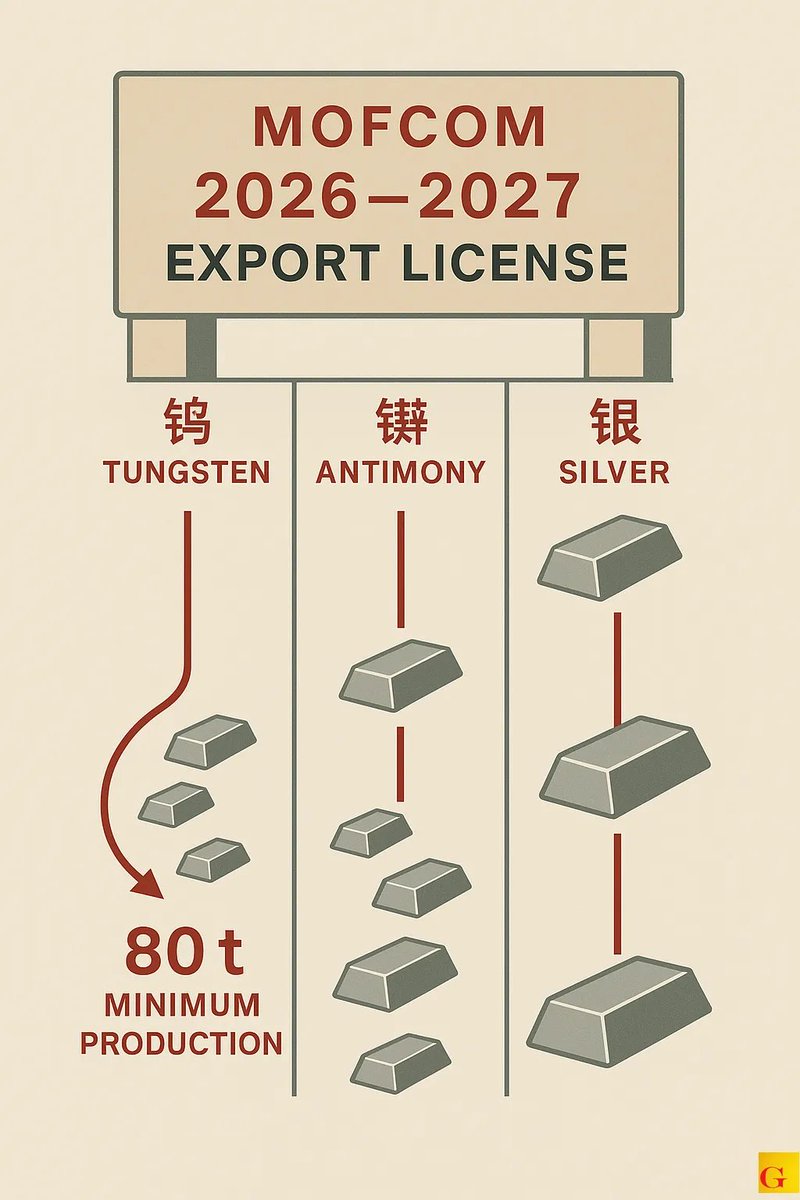

Maybe it's the export license put in at end of last yr to restrict Tungsten, Antimony & Silver.

Maybe it's the export license put in at end of last yr to restrict Tungsten, Antimony & Silver.

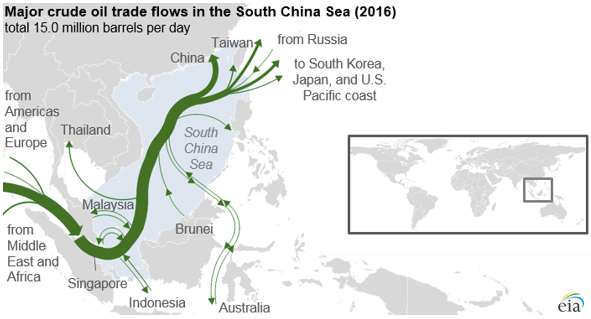

In order to control SCS, PLA had to control major area of SCS that are far from Hainan.

In order to control SCS, PLA had to control major area of SCS that are far from Hainan.

Saudis could very well be settling more in RMB due to shift from relying on Chinese weapons (directly + those operated by Pakistan) for its security vs reliant on US protection.

Saudis could very well be settling more in RMB due to shift from relying on Chinese weapons (directly + those operated by Pakistan) for its security vs reliant on US protection.

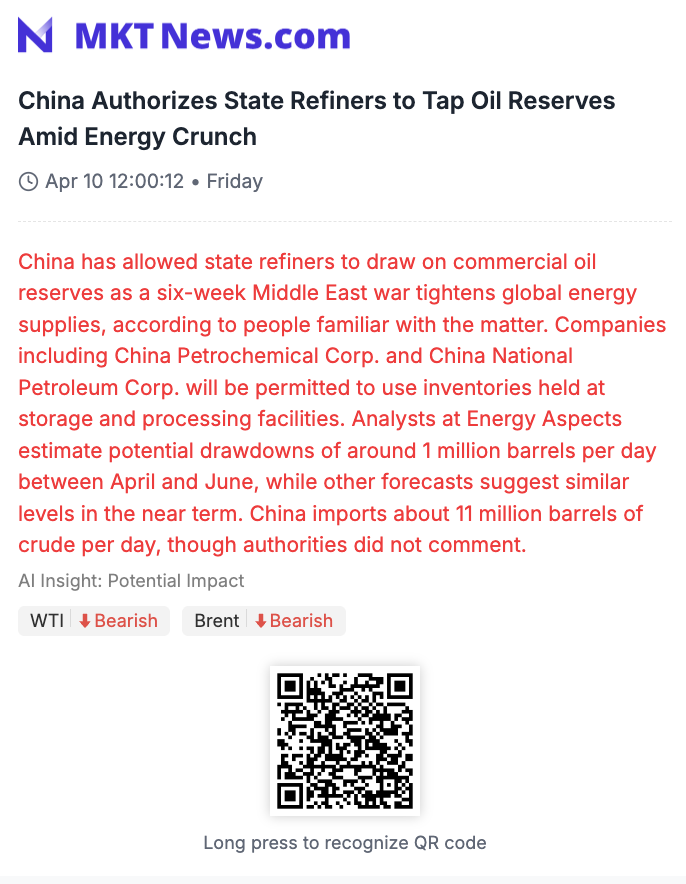

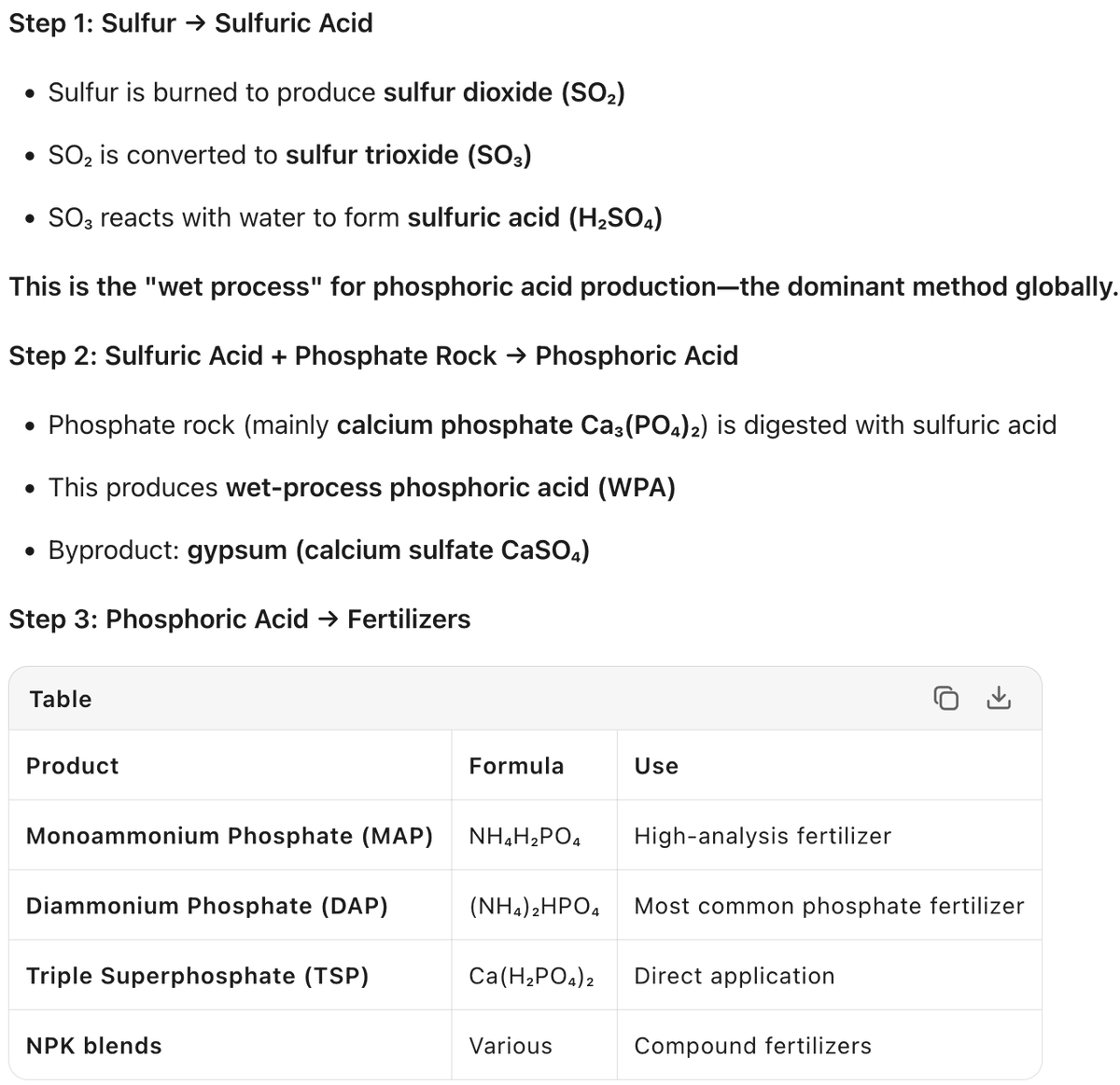

Even w/ the Iranian & Russian supply, China banned Sulfuric Acid export recently + started tapping commercial oil reserves (not SPR).

Even w/ the Iranian & Russian supply, China banned Sulfuric Acid export recently + started tapping commercial oil reserves (not SPR).

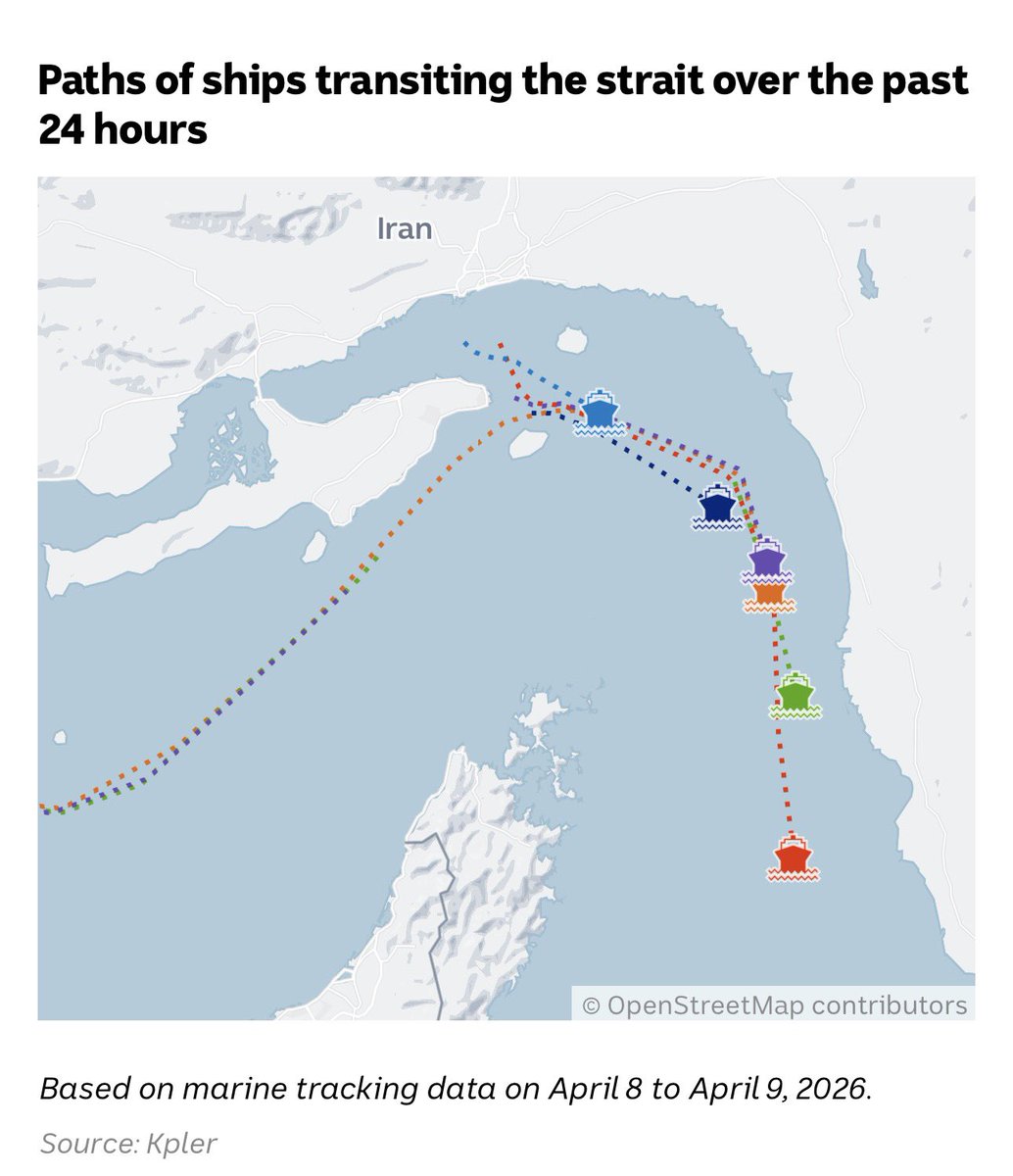

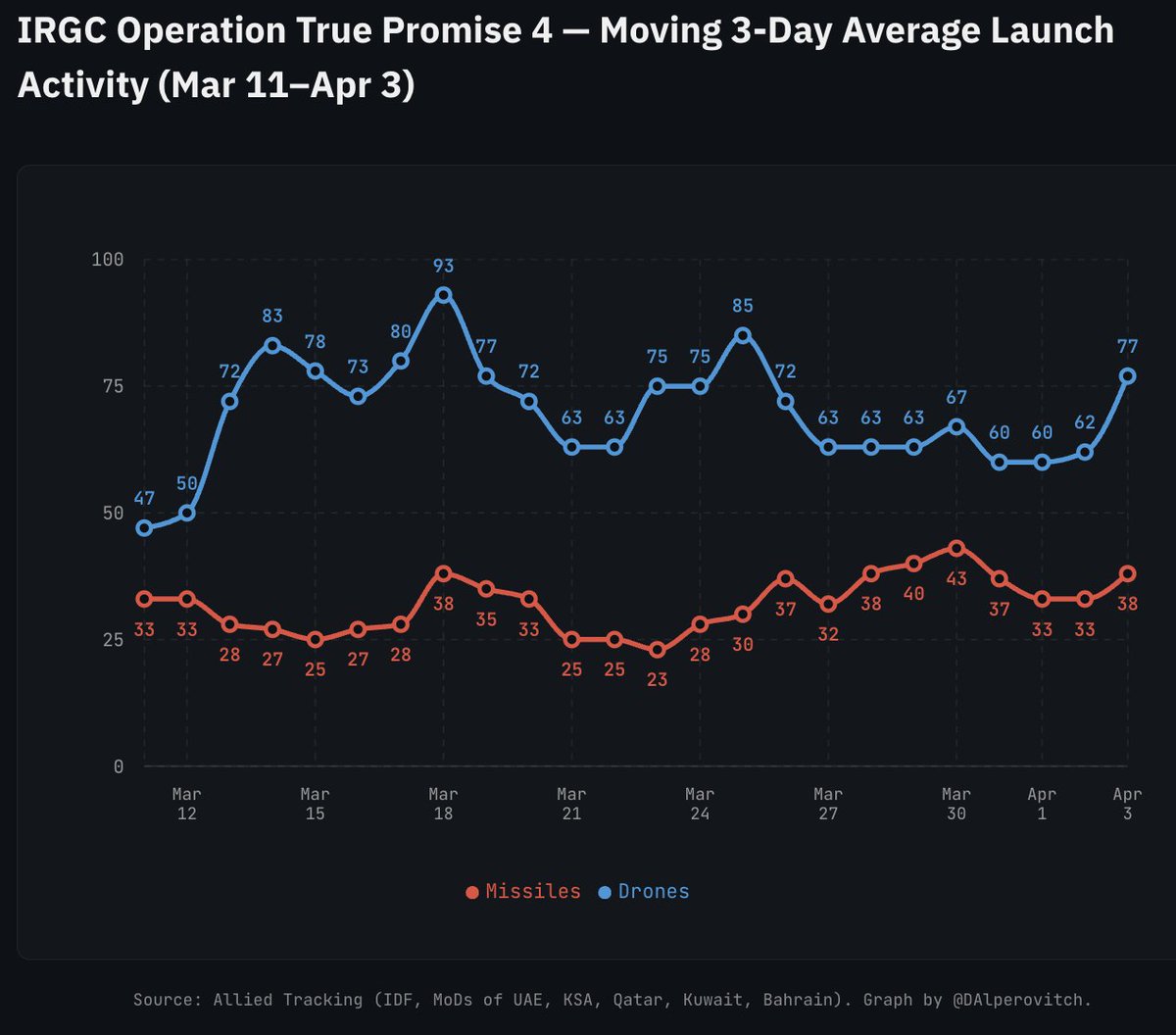

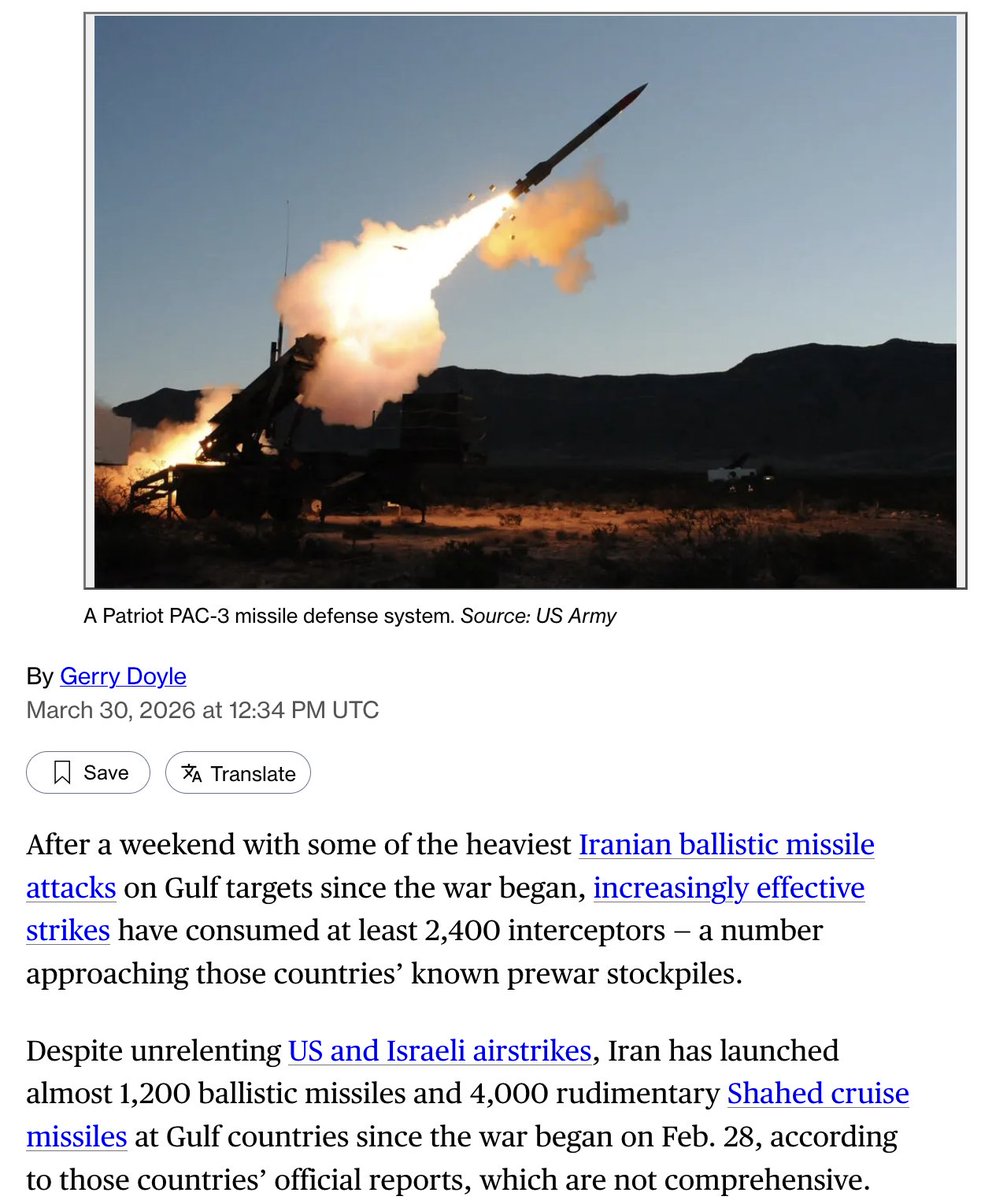

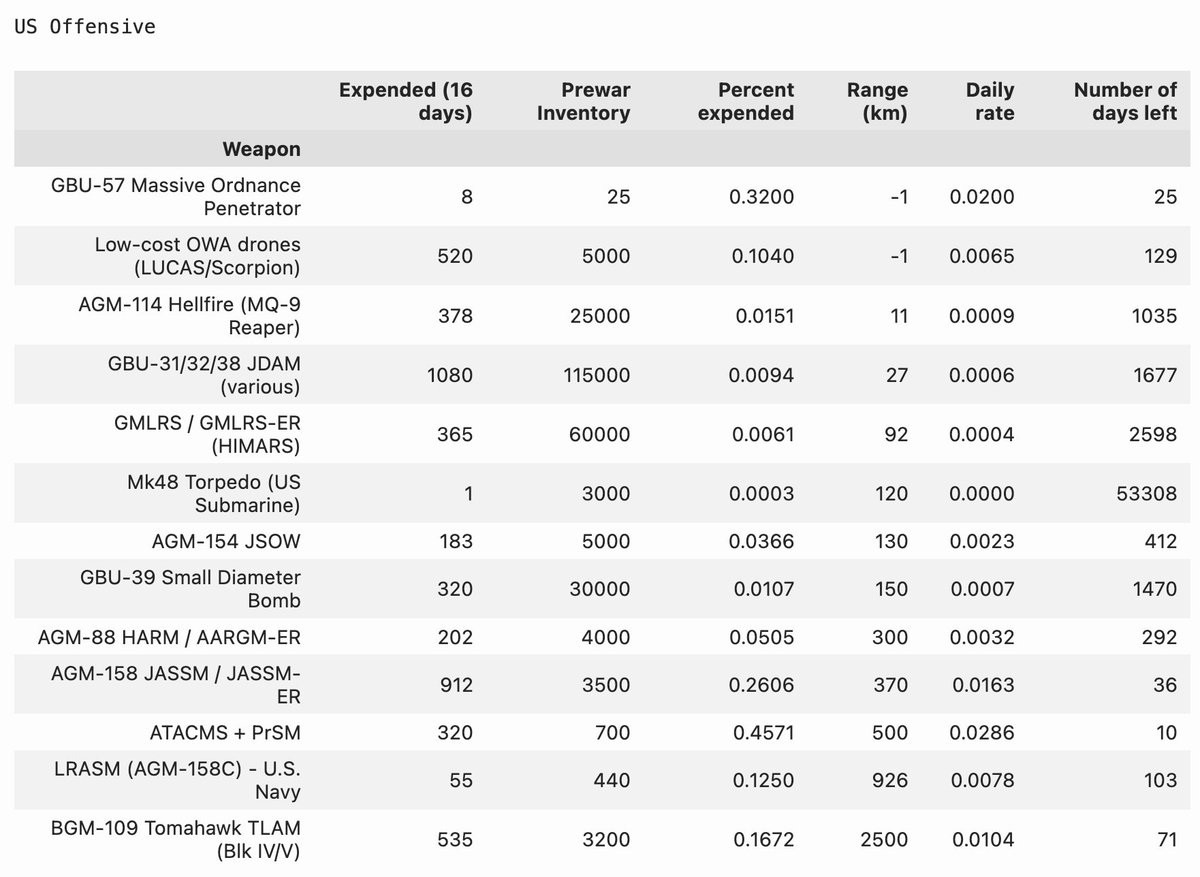

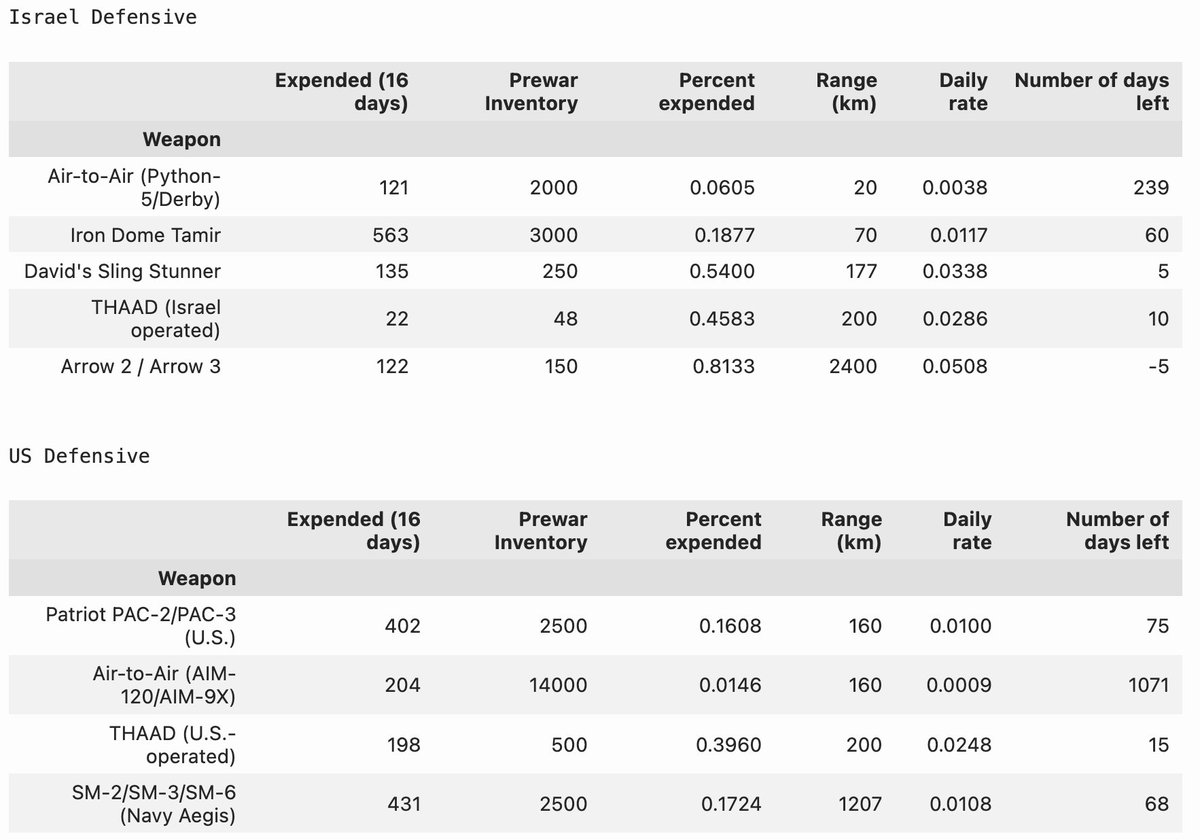

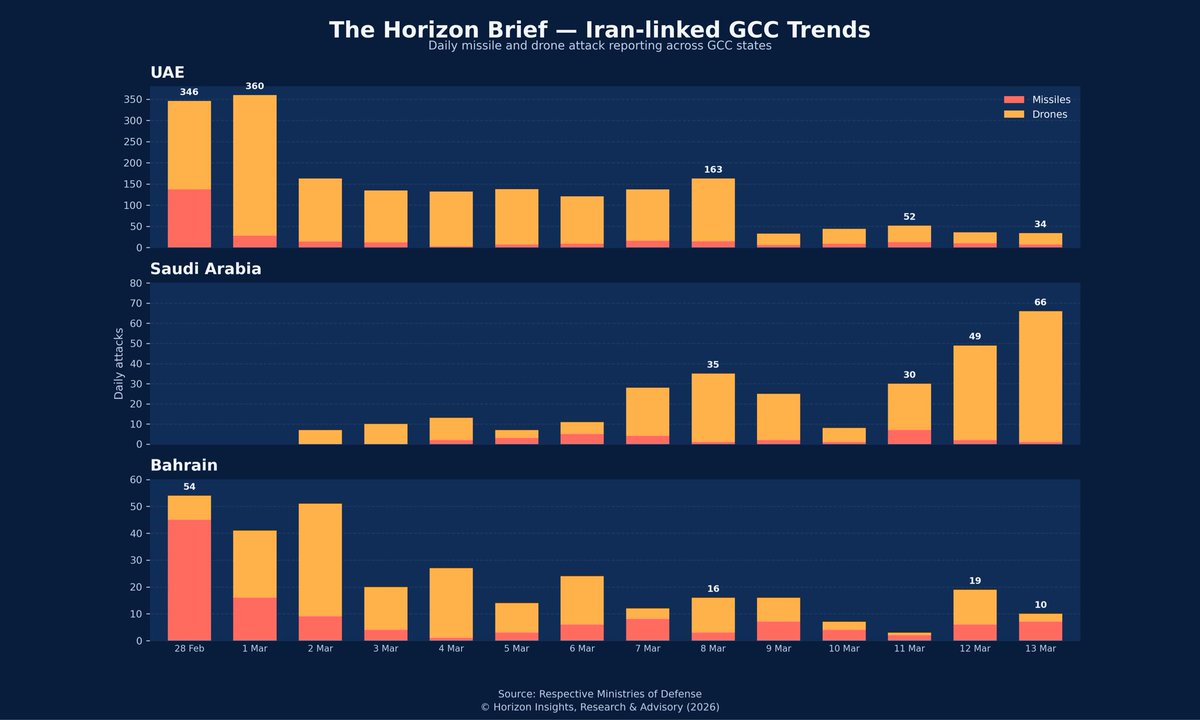

US allies in the region are running out of interceptors after a month of attack & Strait of Hormuz remains shut unless you have a deal w/ Iranian & "pay the toll".

US allies in the region are running out of interceptors after a month of attack & Strait of Hormuz remains shut unless you have a deal w/ Iranian & "pay the toll".

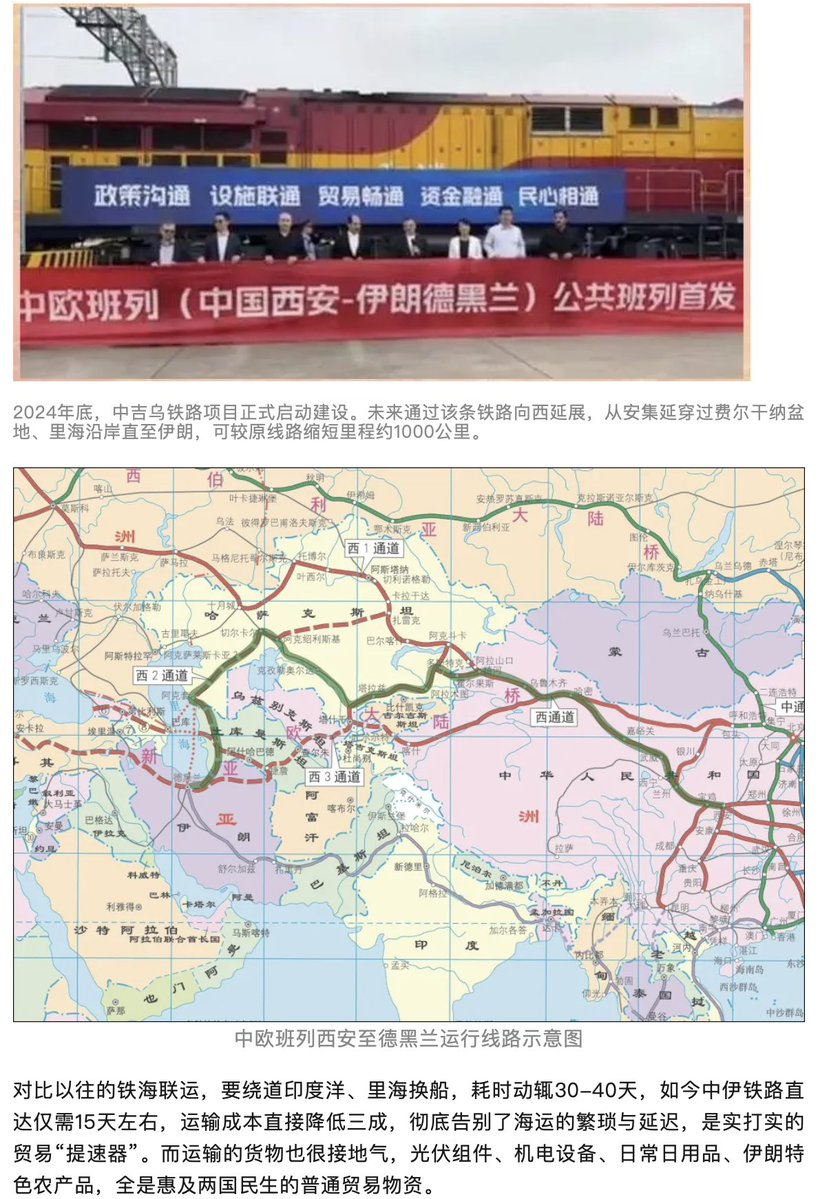

Iran would provide a Russian-free rail option to Europe that is not limited by Caspian Sea. Can go through newly constructed CKU rail & Turkmenistan or thru Afghanistan or thru Kazakhstan+Turkmenistan or thru Pakistan.

Iran would provide a Russian-free rail option to Europe that is not limited by Caspian Sea. Can go through newly constructed CKU rail & Turkmenistan or thru Afghanistan or thru Kazakhstan+Turkmenistan or thru Pakistan.

Yesterday, another few tankers + 1 or 2 E-3 got taken out (only 6 E3 in theater in total), huge loss for USAF.

Yesterday, another few tankers + 1 or 2 E-3 got taken out (only 6 E3 in theater in total), huge loss for USAF.

Lao Cai - Hai Phong project connects Northern Vietnam from border w/ China in Yunnan to the biggest city next to Halong Bay.

Lao Cai - Hai Phong project connects Northern Vietnam from border w/ China in Yunnan to the biggest city next to Halong Bay.

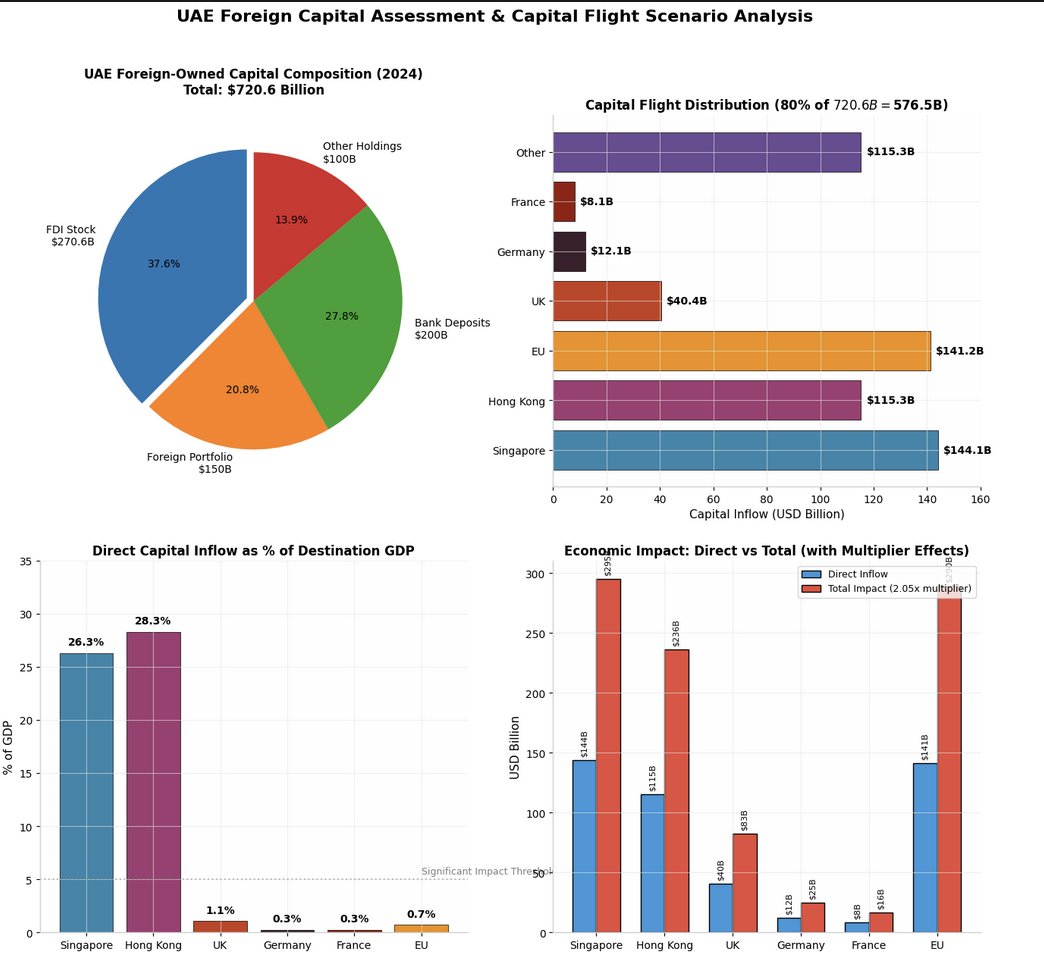

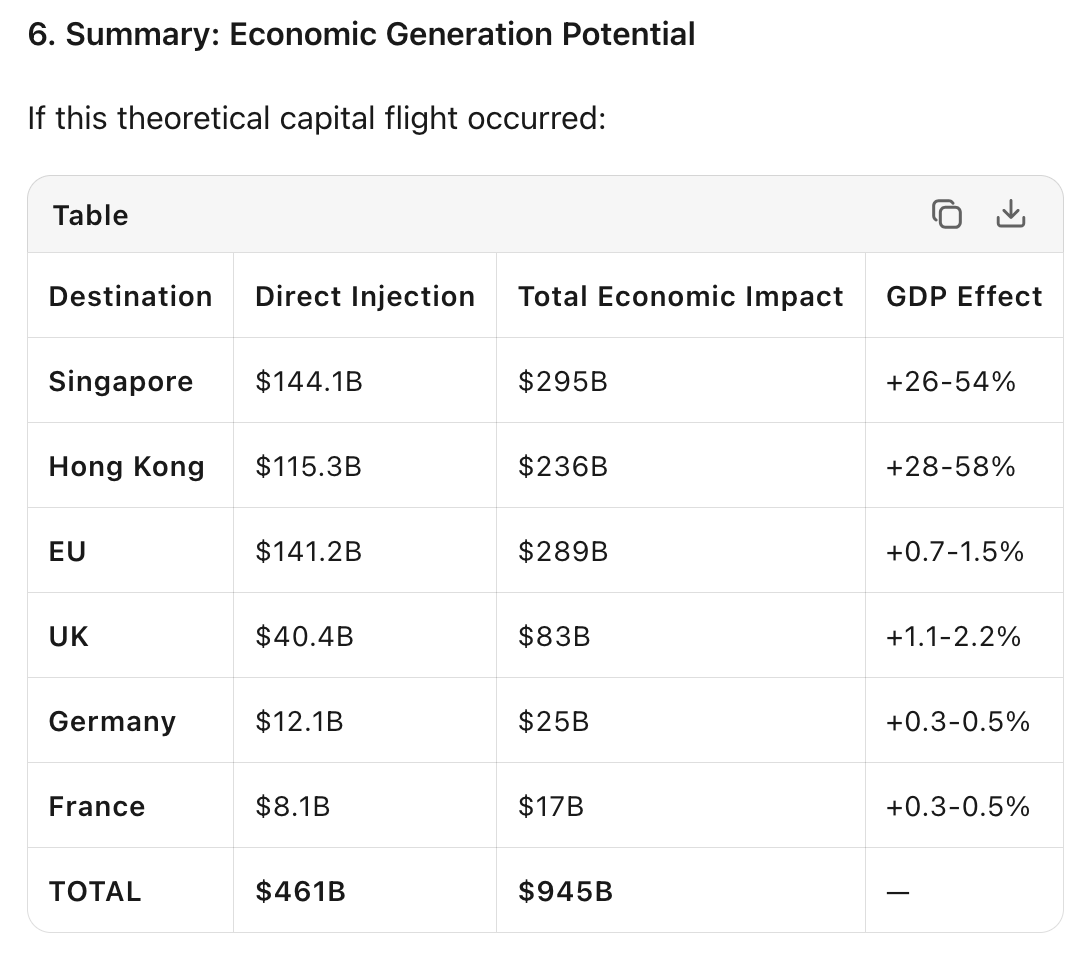

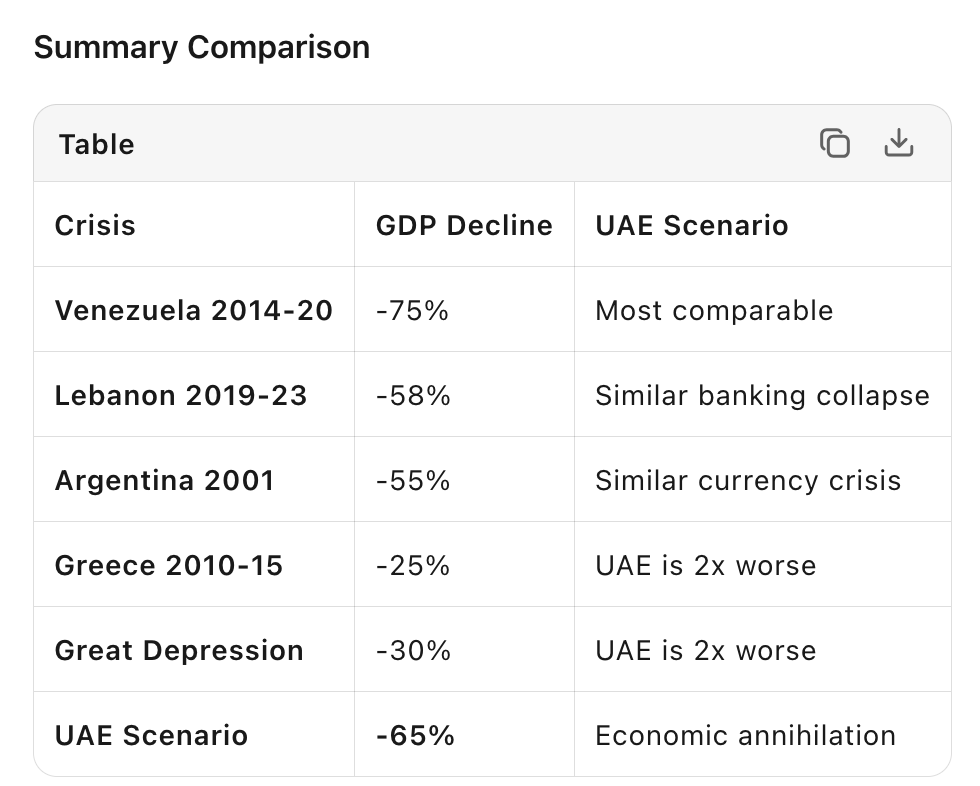

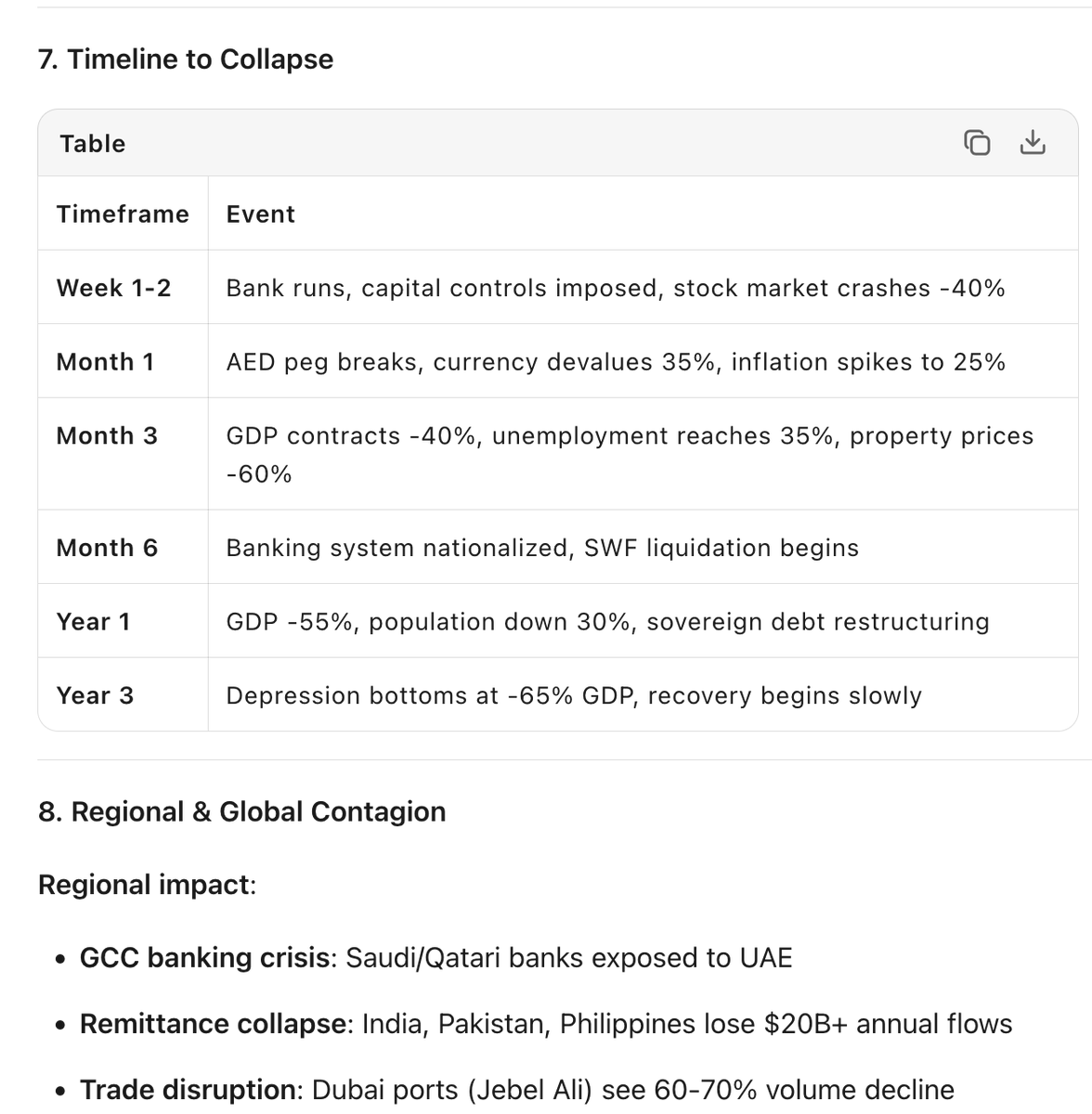

A massive outflow of foreign capital from UAE would be total economic annihilation there. It would be 2x as bad as Great Depression & lead to massive contagion, bank runs & currency collapse across GCC countries, b4 spreading to global banking sector.

A massive outflow of foreign capital from UAE would be total economic annihilation there. It would be 2x as bad as Great Depression & lead to massive contagion, bank runs & currency collapse across GCC countries, b4 spreading to global banking sector.

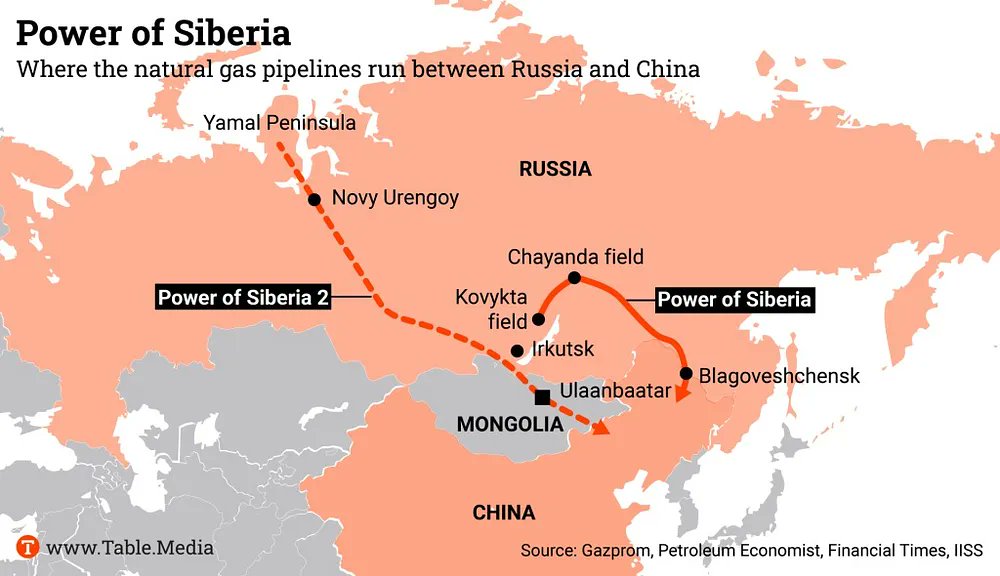

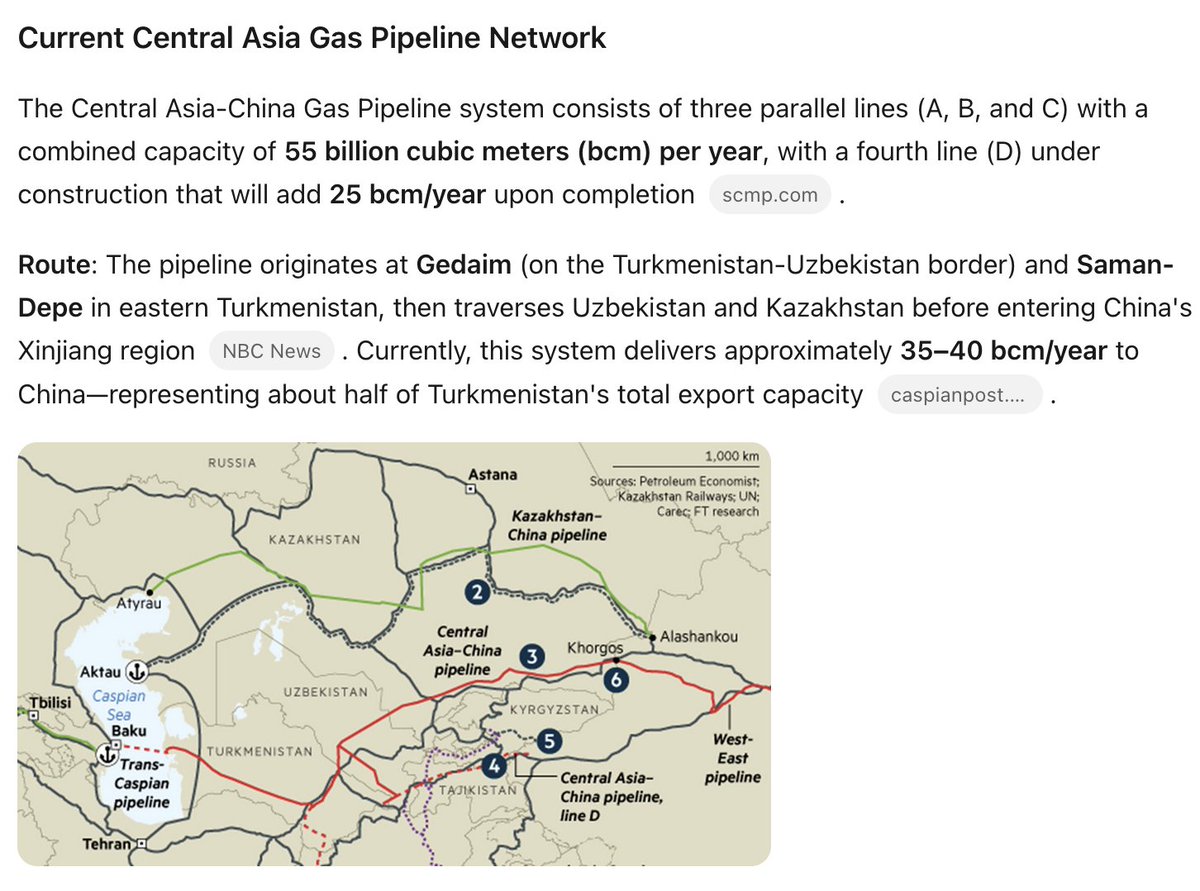

There are 2 major gas pipeline projects under way to China:

There are 2 major gas pipeline projects under way to China:

If you need to know how things are going:

If you need to know how things are going:

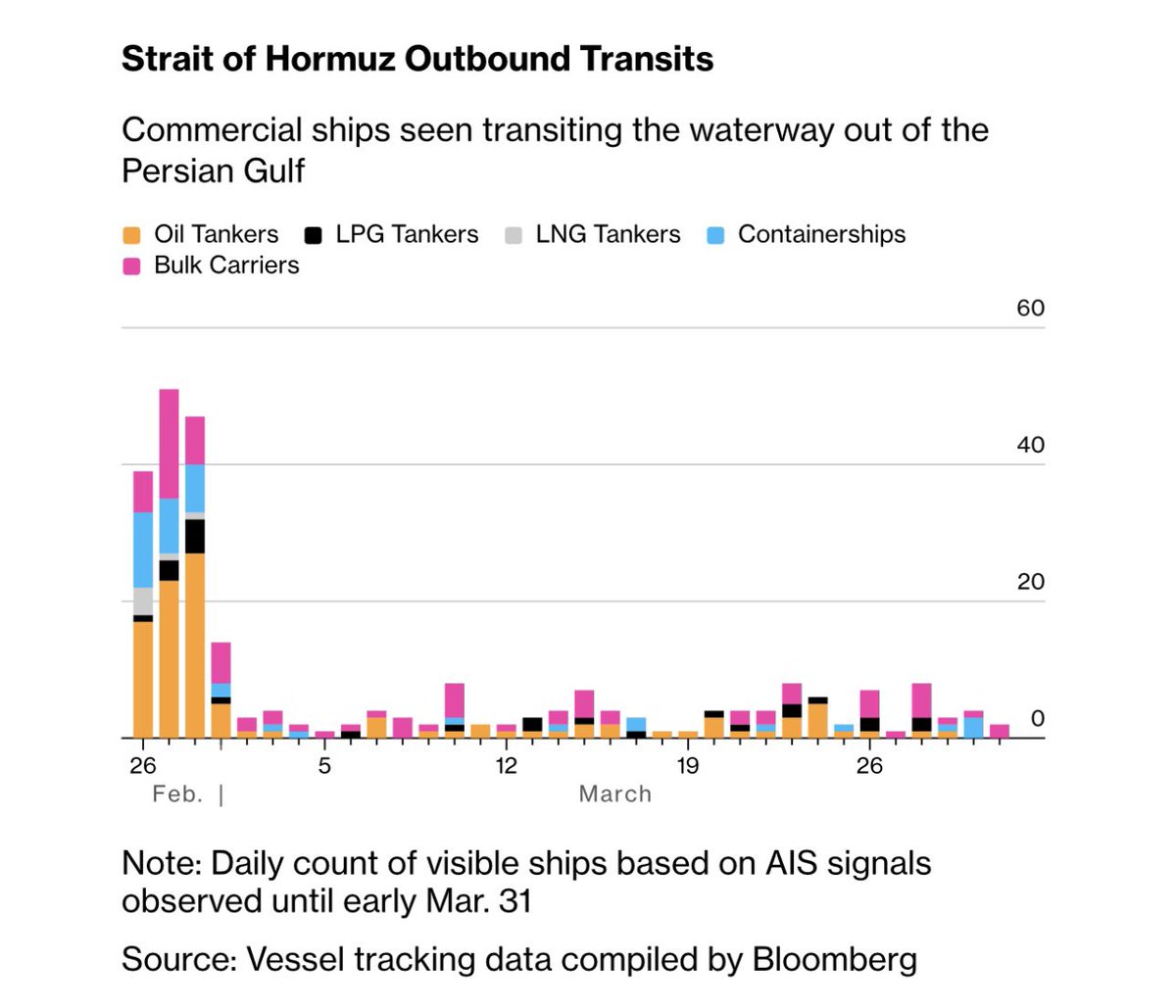

A simple look at the US tanker fleet action would point to the importance of Saudi Arabia, Jordan & Iraq toward continually supporting Coalition strikes on Iran.

A simple look at the US tanker fleet action would point to the importance of Saudi Arabia, Jordan & Iraq toward continually supporting Coalition strikes on Iran.

Most common use is fertilizers.

Most common use is fertilizers.

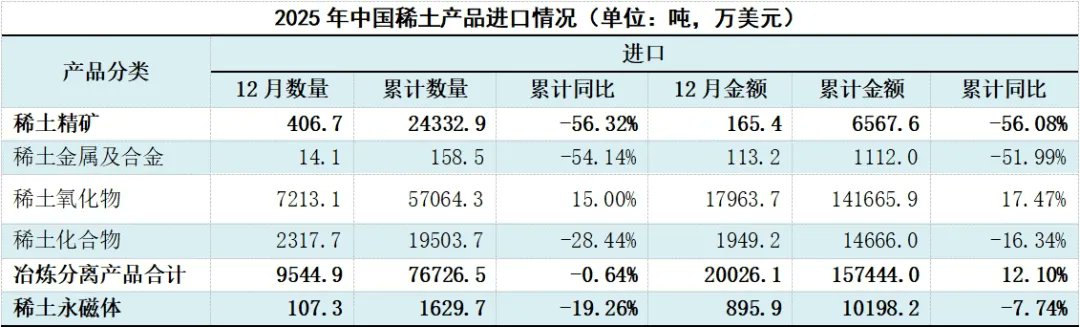

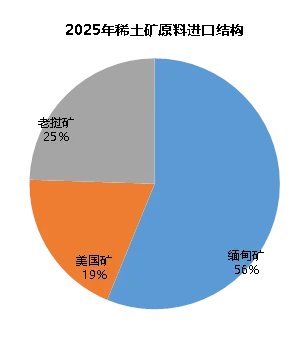

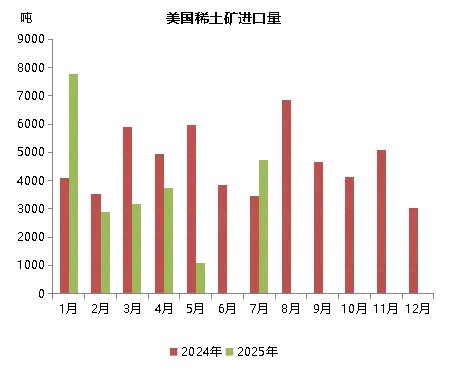

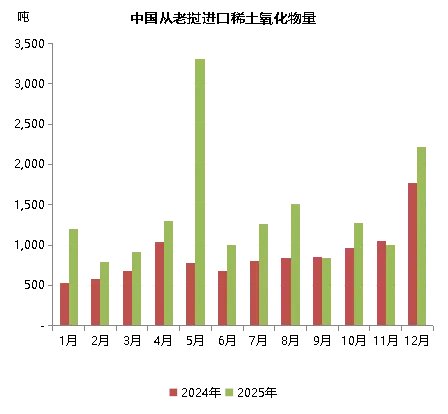

Big change in import this yr is caused by no longer getting Rare earth ore from US (for obvious reasons), but more RE Oxide from Myanmar & ore from Laos.

Big change in import this yr is caused by no longer getting Rare earth ore from US (for obvious reasons), but more RE Oxide from Myanmar & ore from Laos.

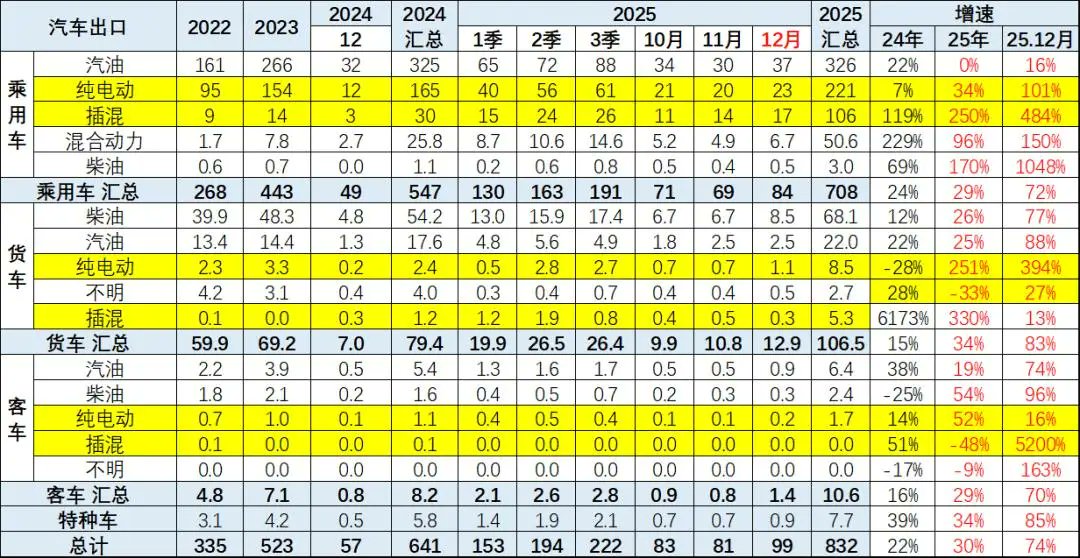

Overall, the goal of China's auto industry is to surpass Japan. Composition of China's oversea sales need to shift from export to local production.

Overall, the goal of China's auto industry is to surpass Japan. Composition of China's oversea sales need to shift from export to local production.

For renewables, it plans to add 40GW to the grid for 170GW in cumulative installation & generate 300 TWh of electricity.

For renewables, it plans to add 40GW to the grid for 170GW in cumulative installation & generate 300 TWh of electricity.

See below for wind installations in 2024 (yellow) & 2025 (green).

See below for wind installations in 2024 (yellow) & 2025 (green).