Petrodollars! Nothing produces more heated discussion and, in my experience, less insight. Myths trump facts, because the actual data is a bit obscure --

But here is the most important thing to know. Before the Hormuz crisis, the flow of petrodollars had more or less dried up

1/many

But here is the most important thing to know. Before the Hormuz crisis, the flow of petrodollars had more or less dried up

1/many

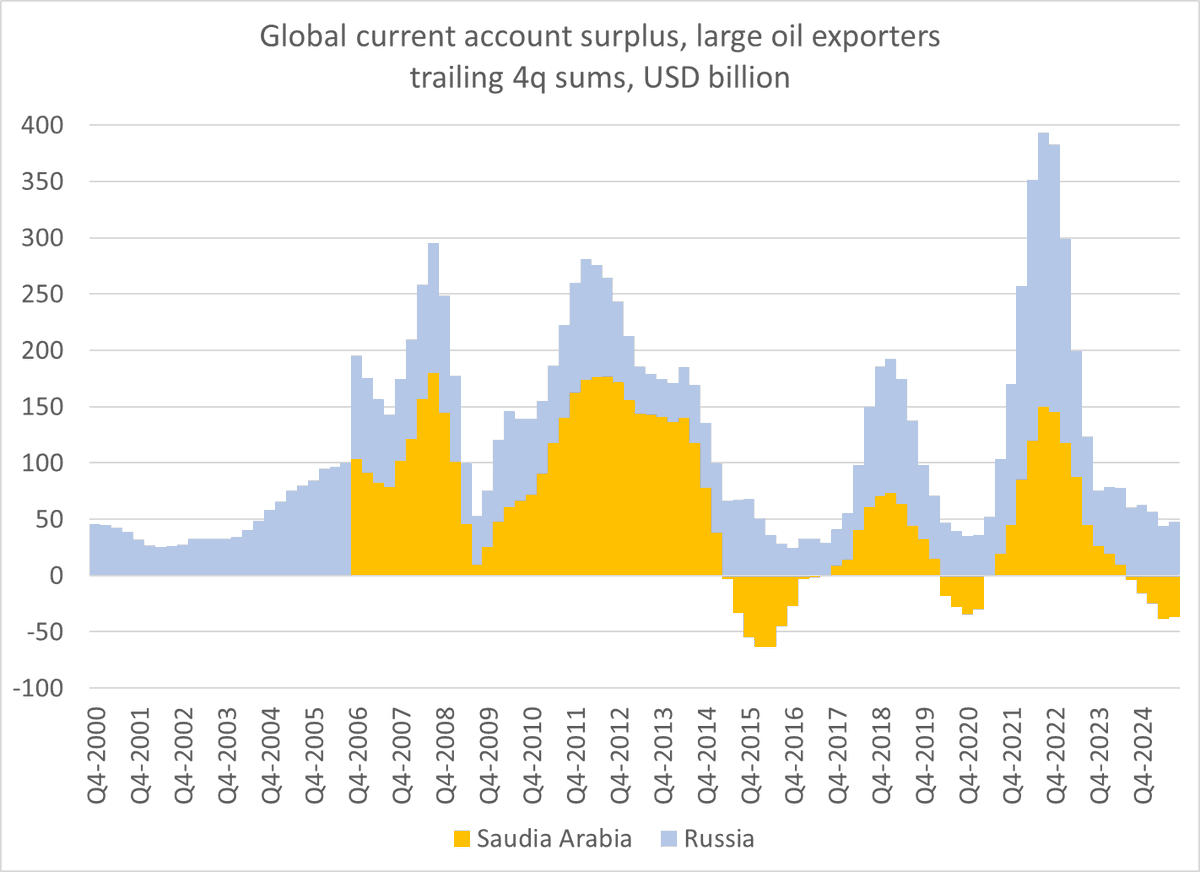

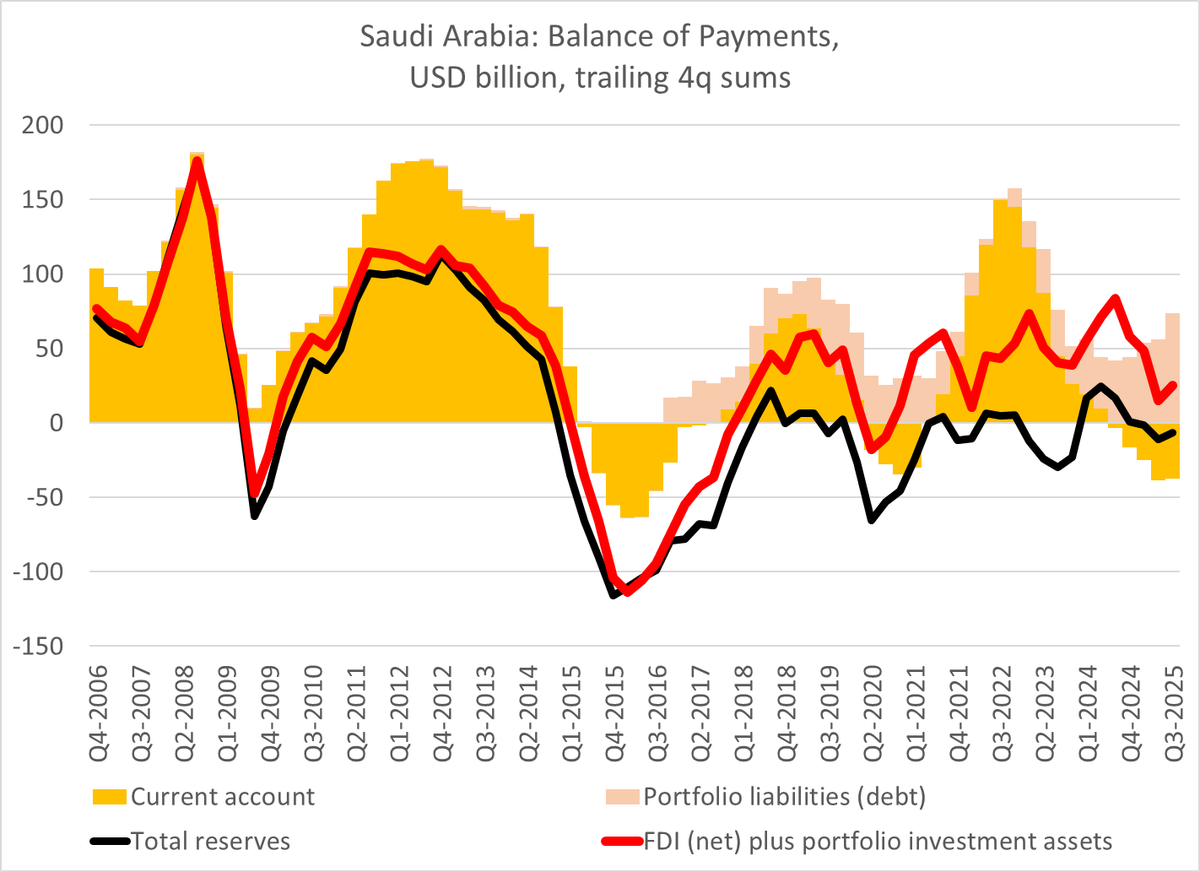

At $60-70 a barrel, the oil exporters just weren't generating large surpluses --

Saudi Arabia's external deficit offset Russia's surplus, so the two biggest oil exporters (~ 15mbd of exports together) were not generating petrodollars, petroeuros or petroyuan

2/

Saudi Arabia's external deficit offset Russia's surplus, so the two biggest oil exporters (~ 15mbd of exports together) were not generating petrodollars, petroeuros or petroyuan

2/

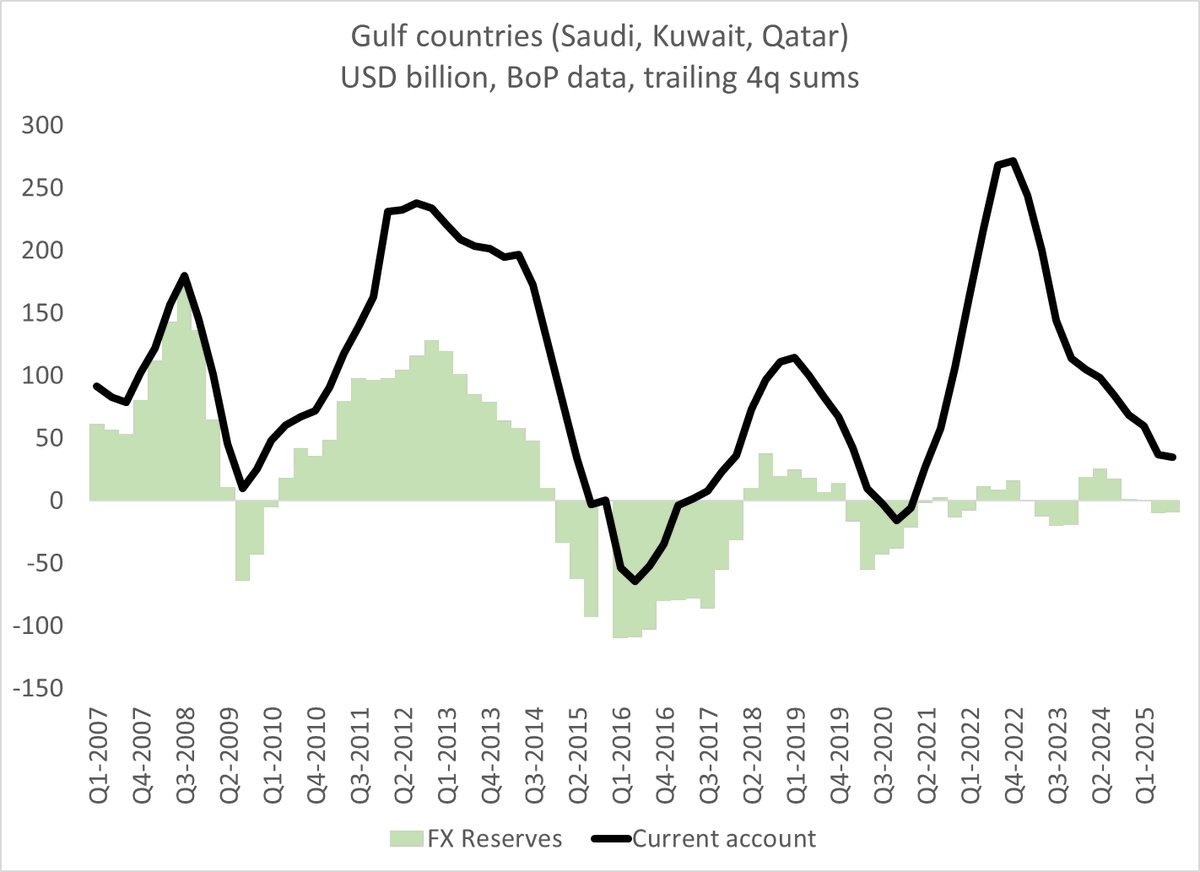

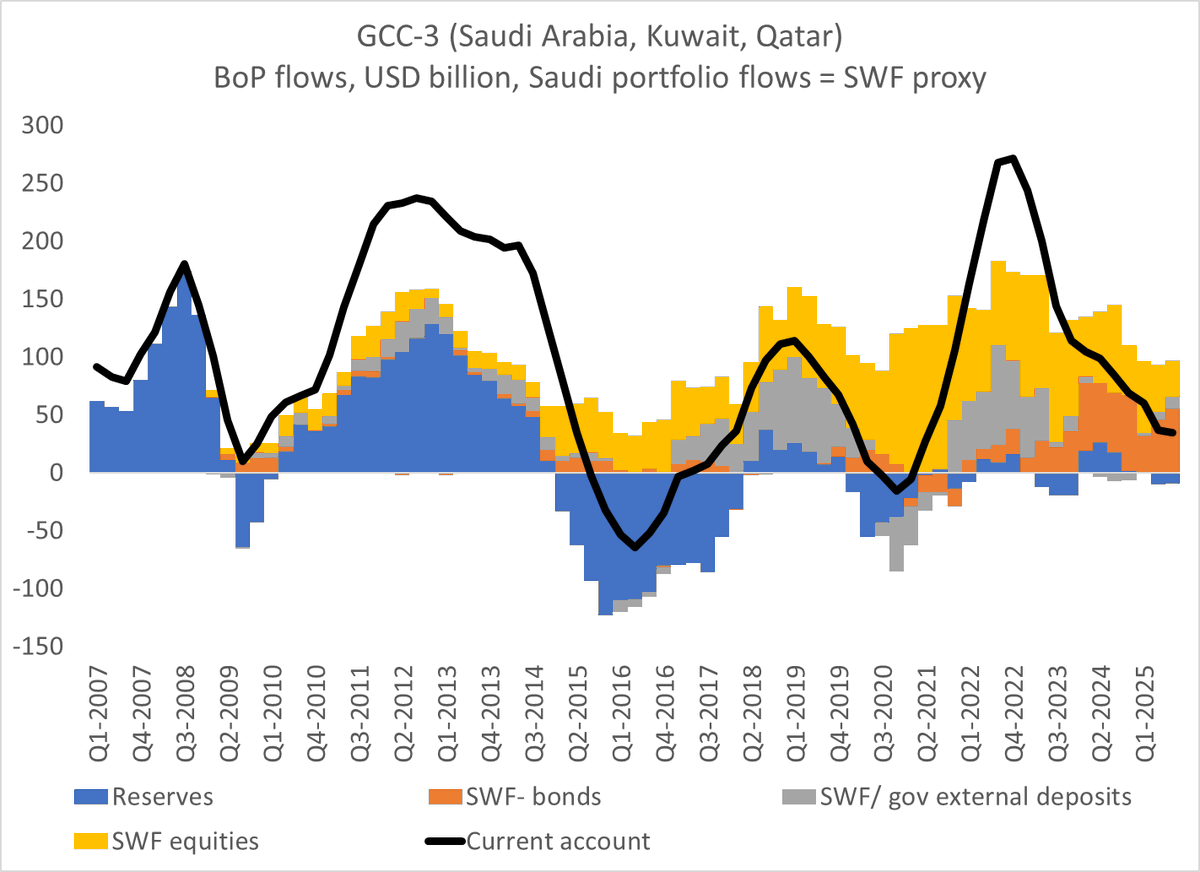

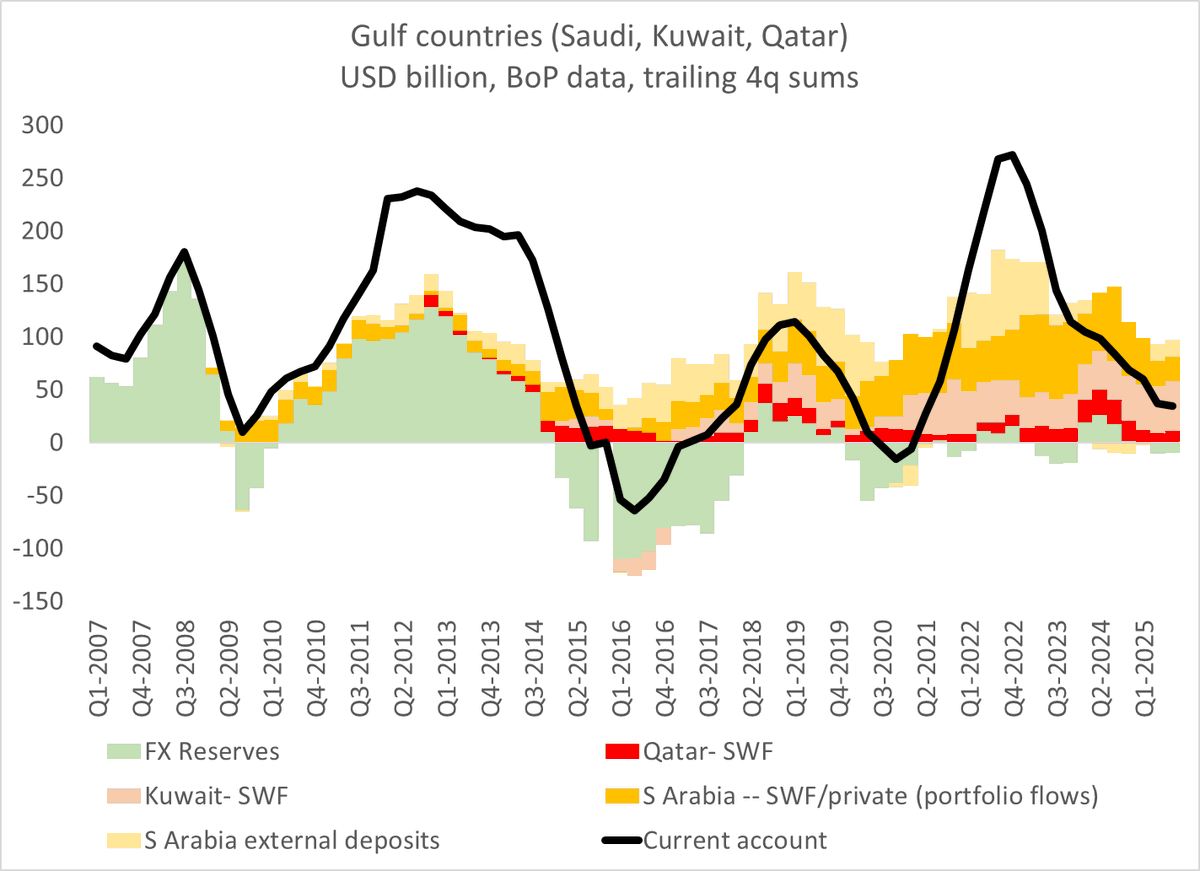

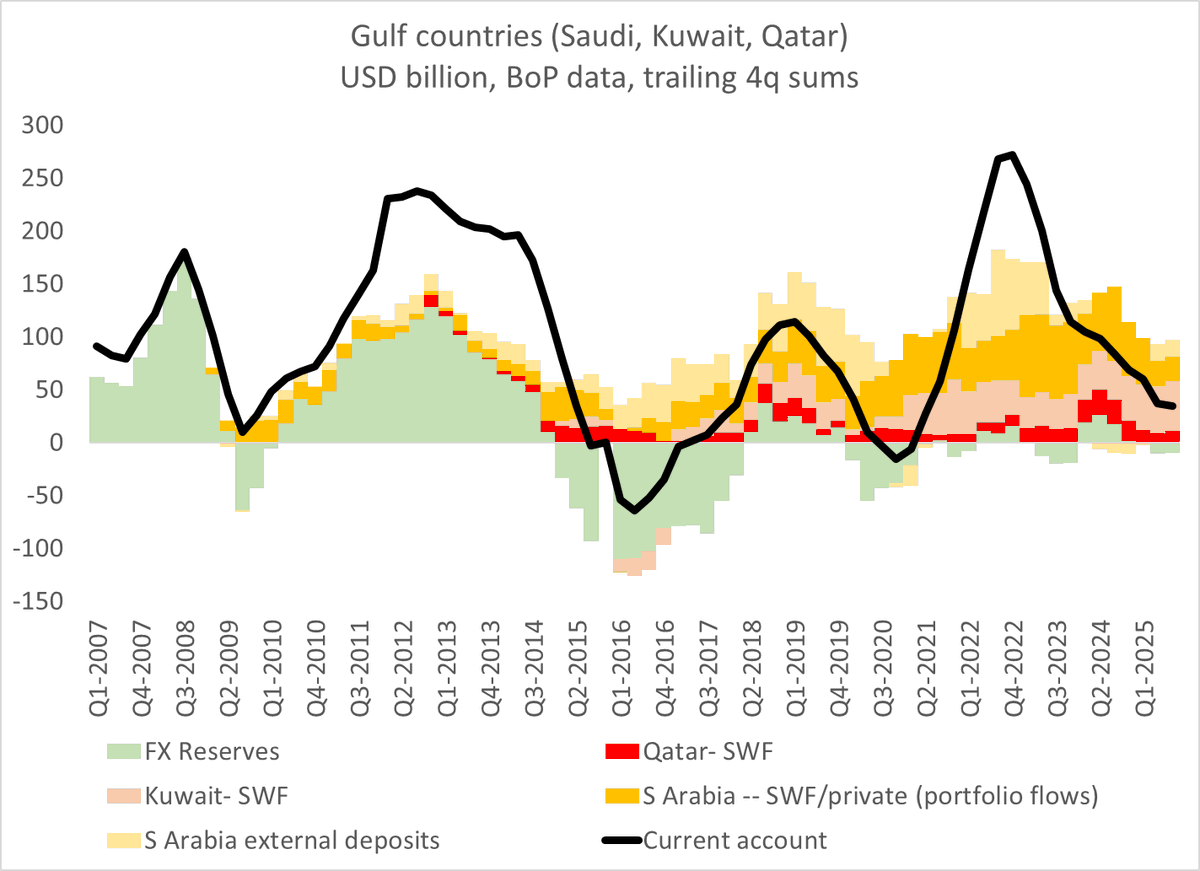

And the GCC countries (no quarterly data for the Emirates, but its surplus is roughly the size of Qatar and Kuwait combined) no longer really stash away their oil surplus in liquid dollar reserves --

3/

3/

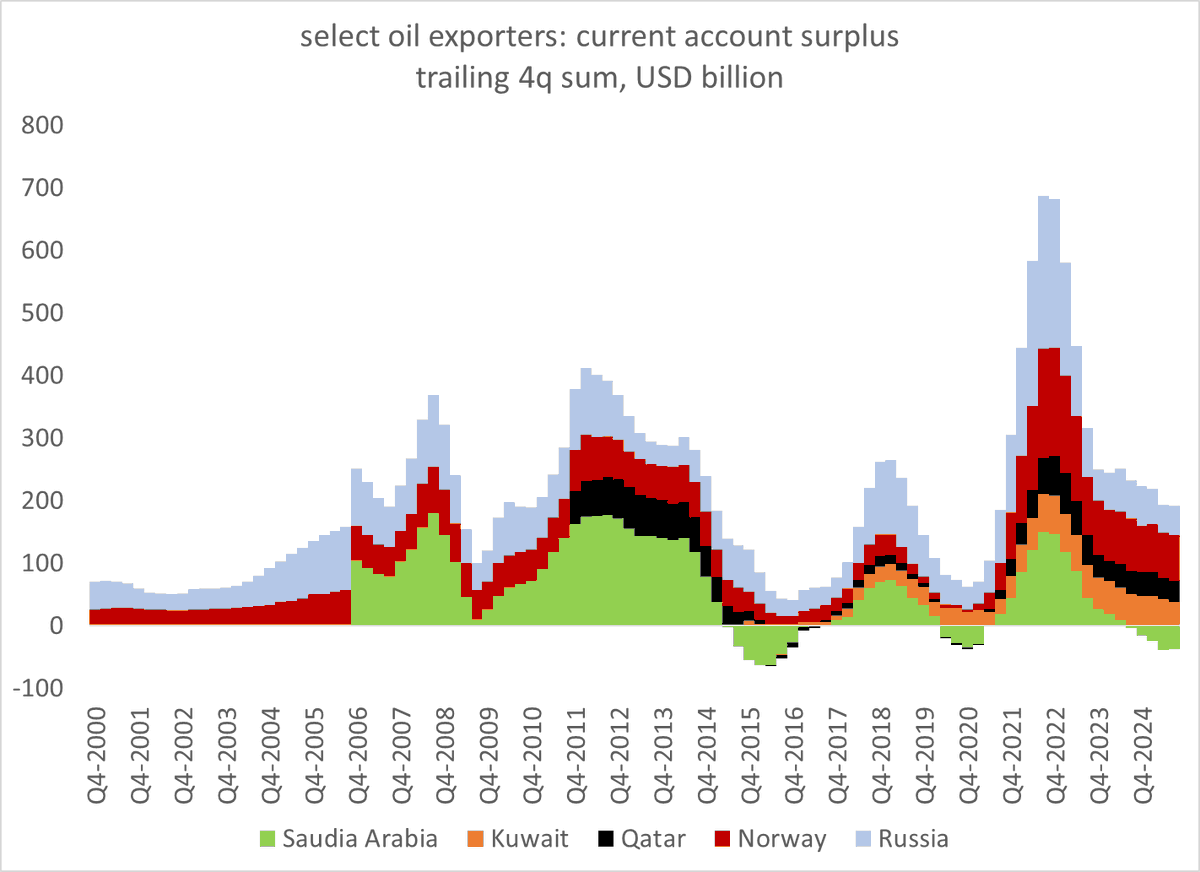

The remaining oil surplus is really found in the GCC-3 (Emirates = no data, but roughly another $70b) and Norway, and that is down to ~ $200-250b a year ...

4/

4/

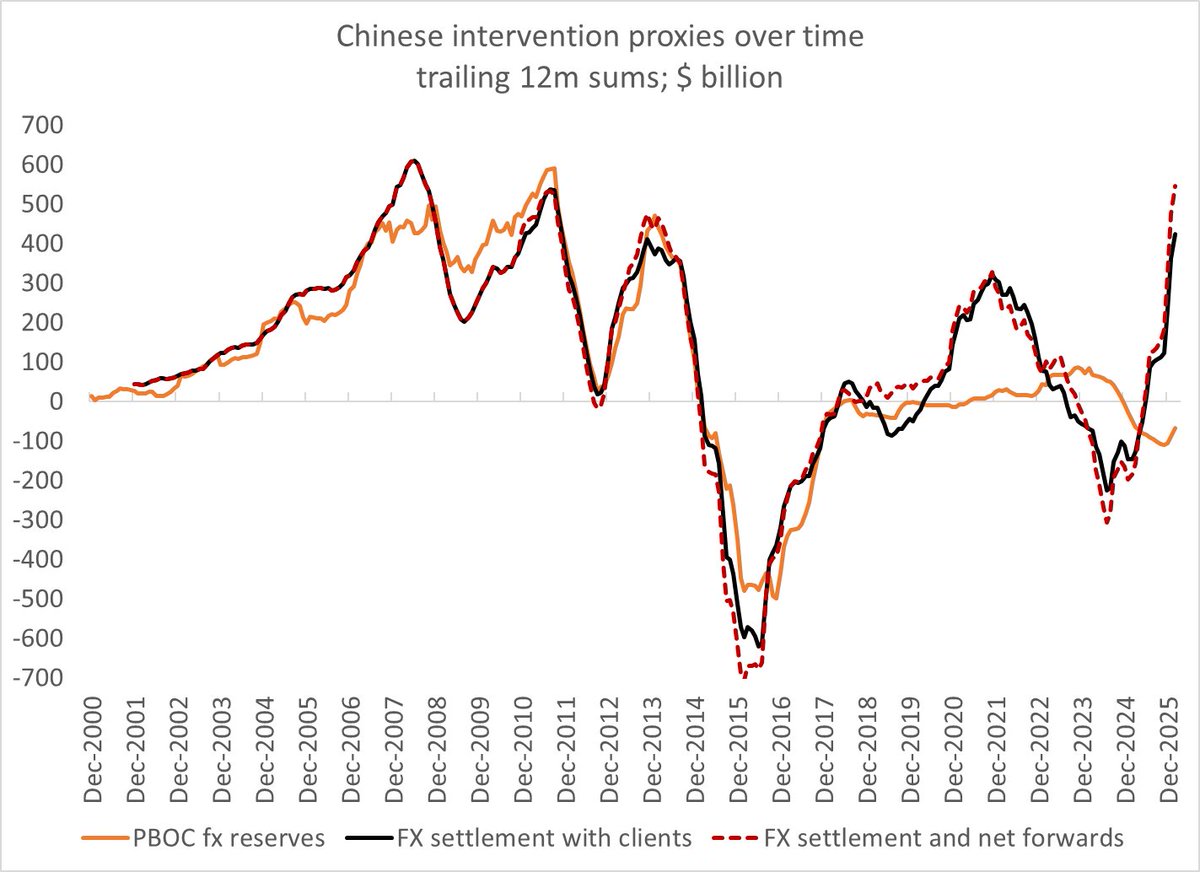

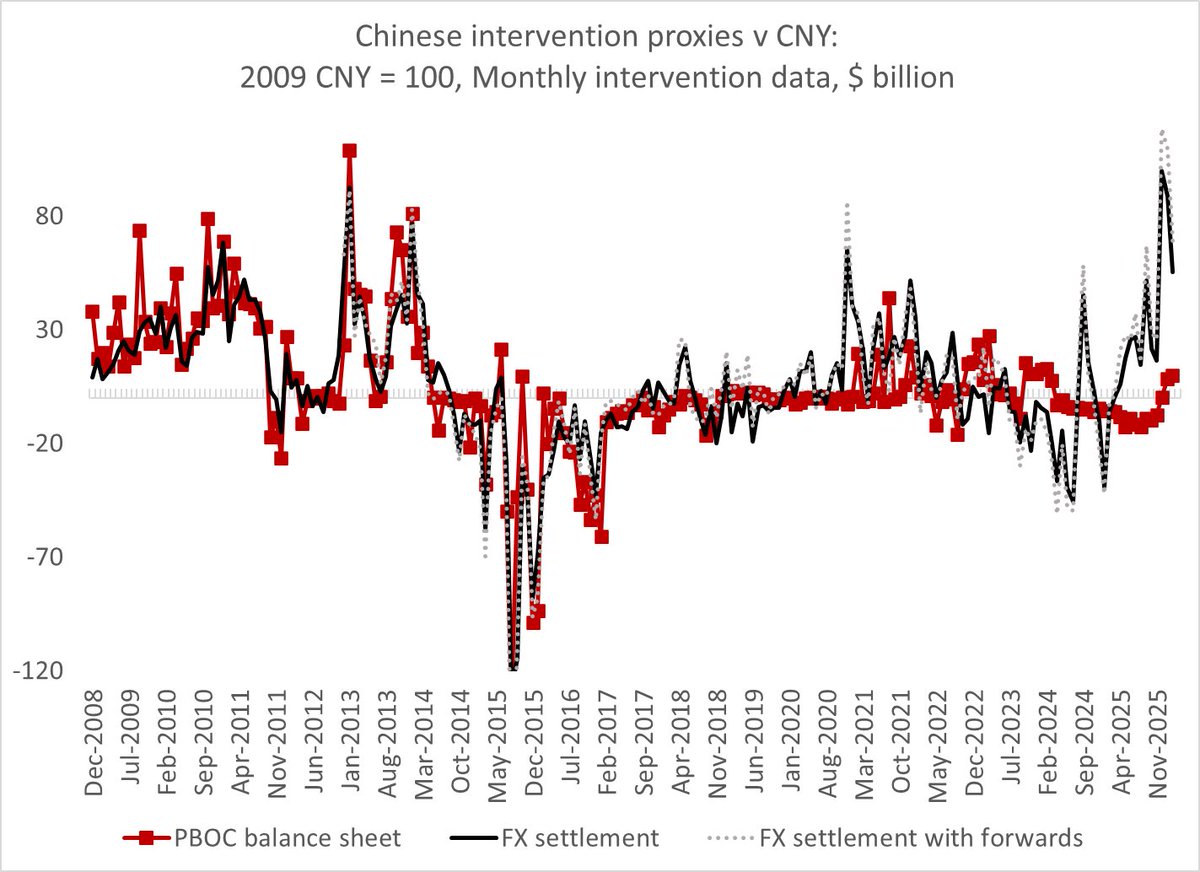

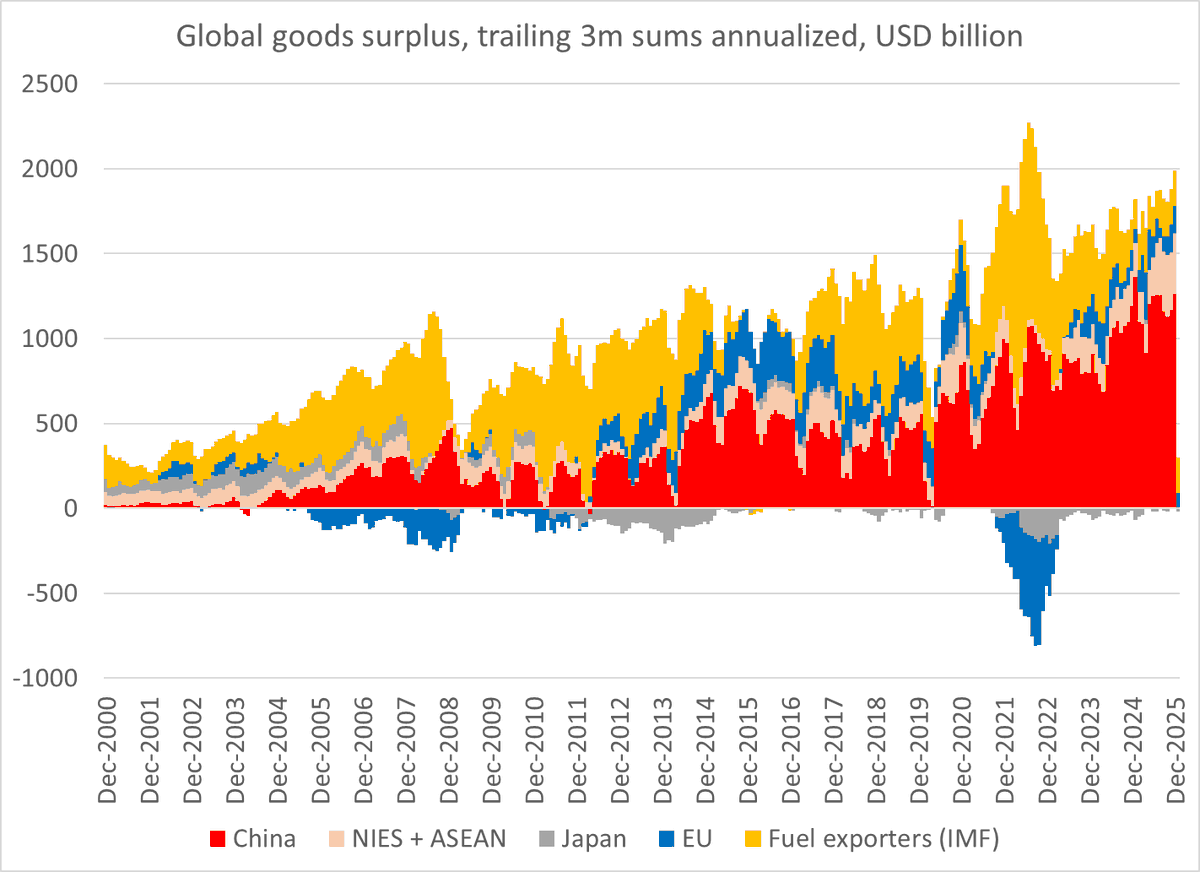

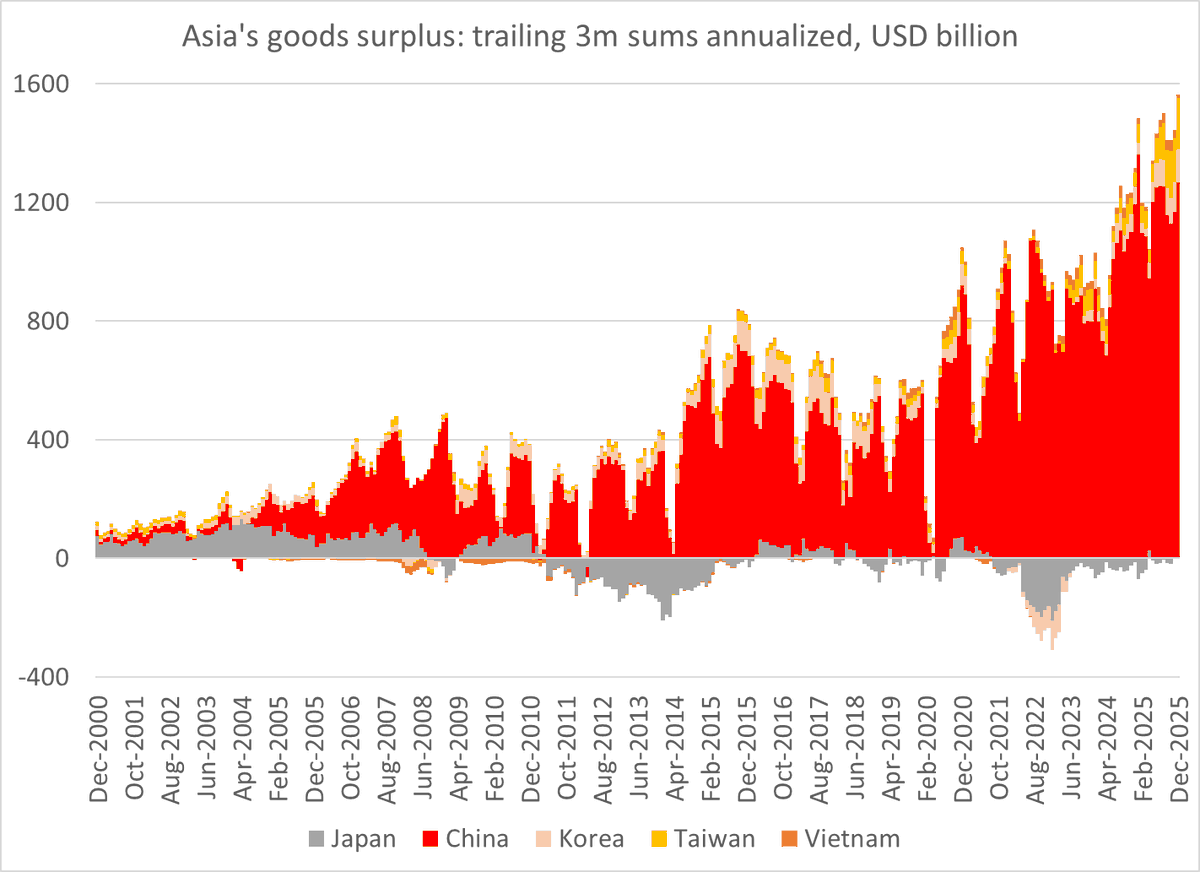

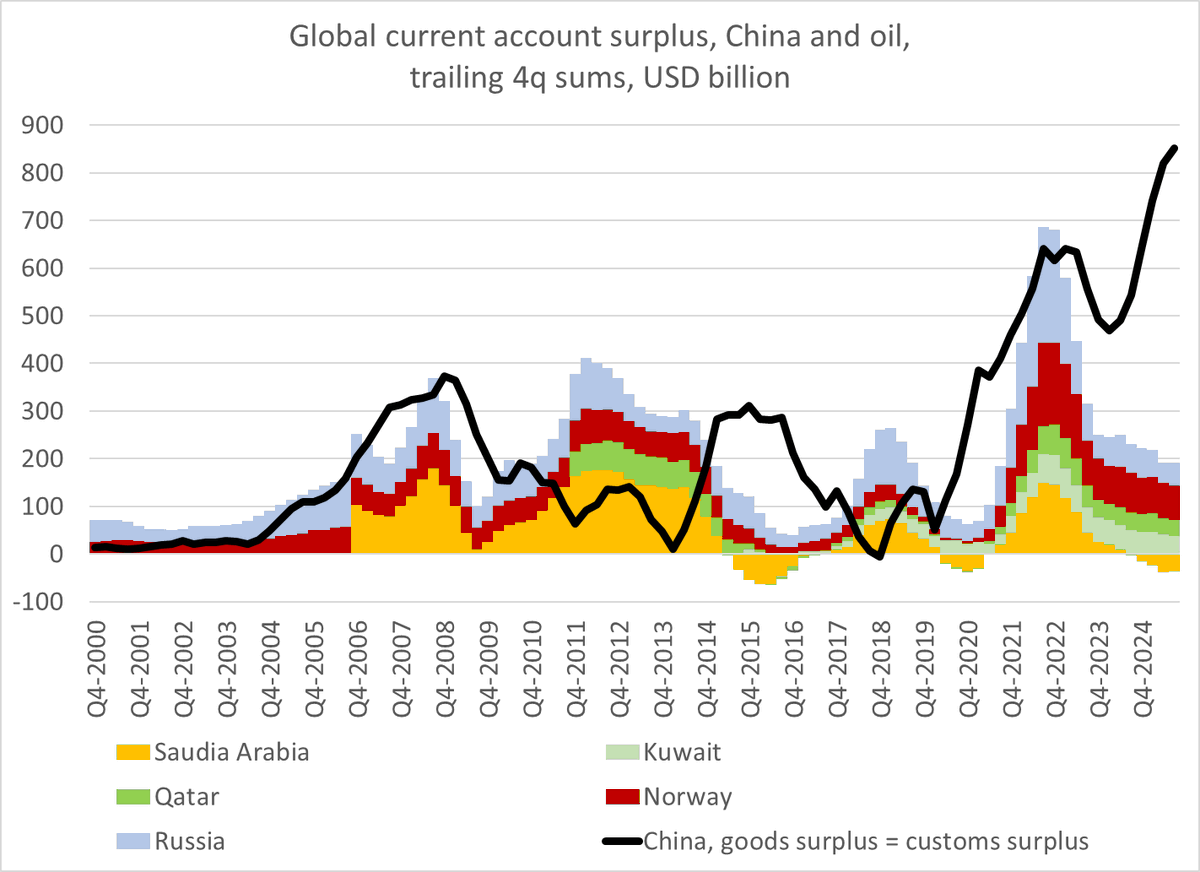

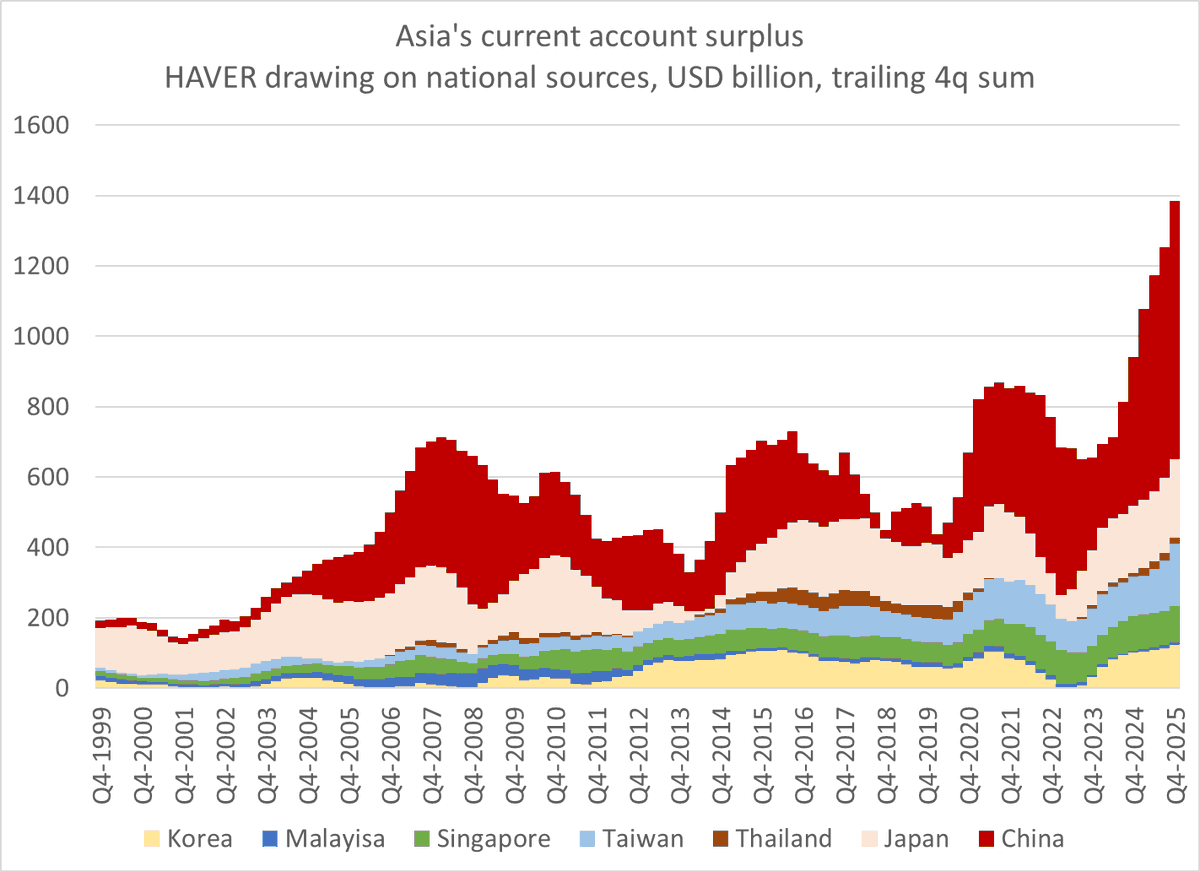

China's surplus (measured correctly) likely approached $1 trillion pre oil shock, and there was another $500b plus in the main Asian surplus economies.

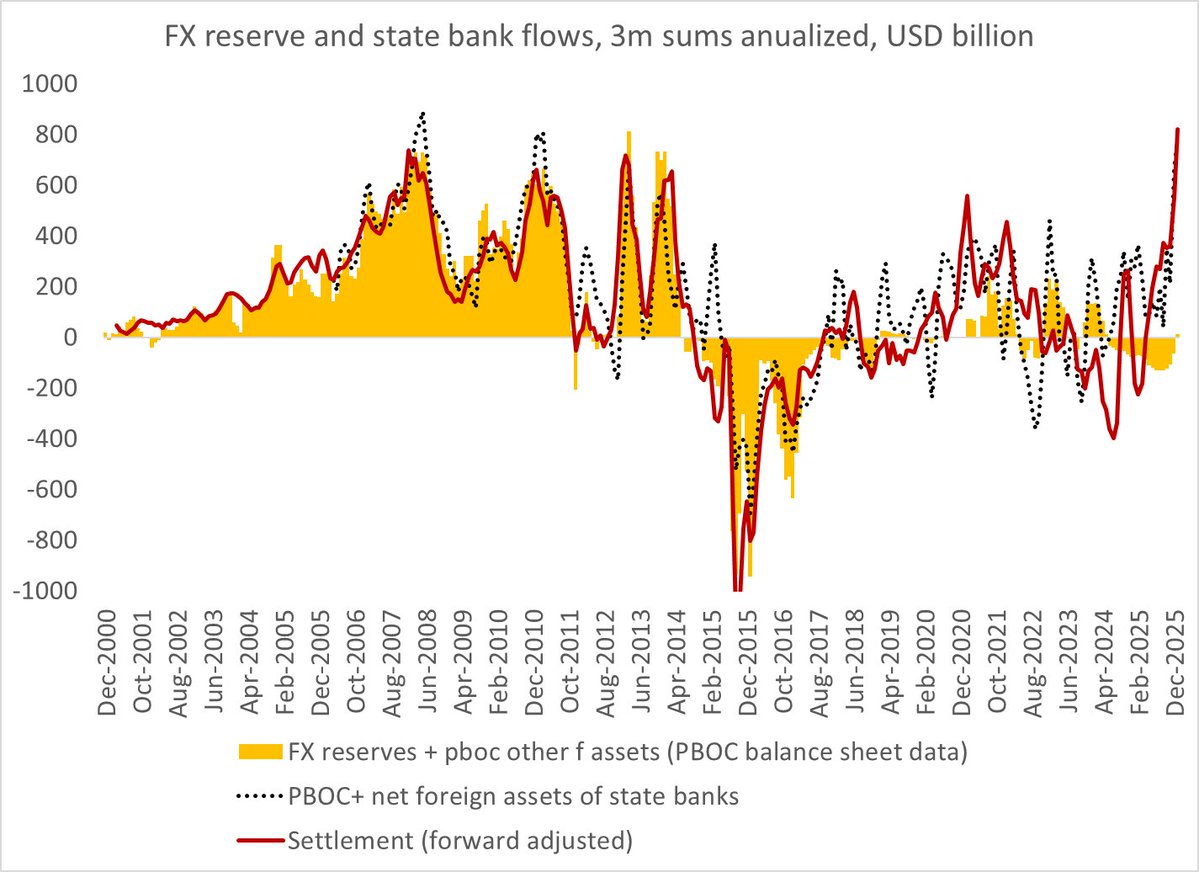

The big source of eurodollars (offshore dollars) were the Chinese exporters offshore funds, & now the SCBs

5/

The big source of eurodollars (offshore dollars) were the Chinese exporters offshore funds, & now the SCBs

5/

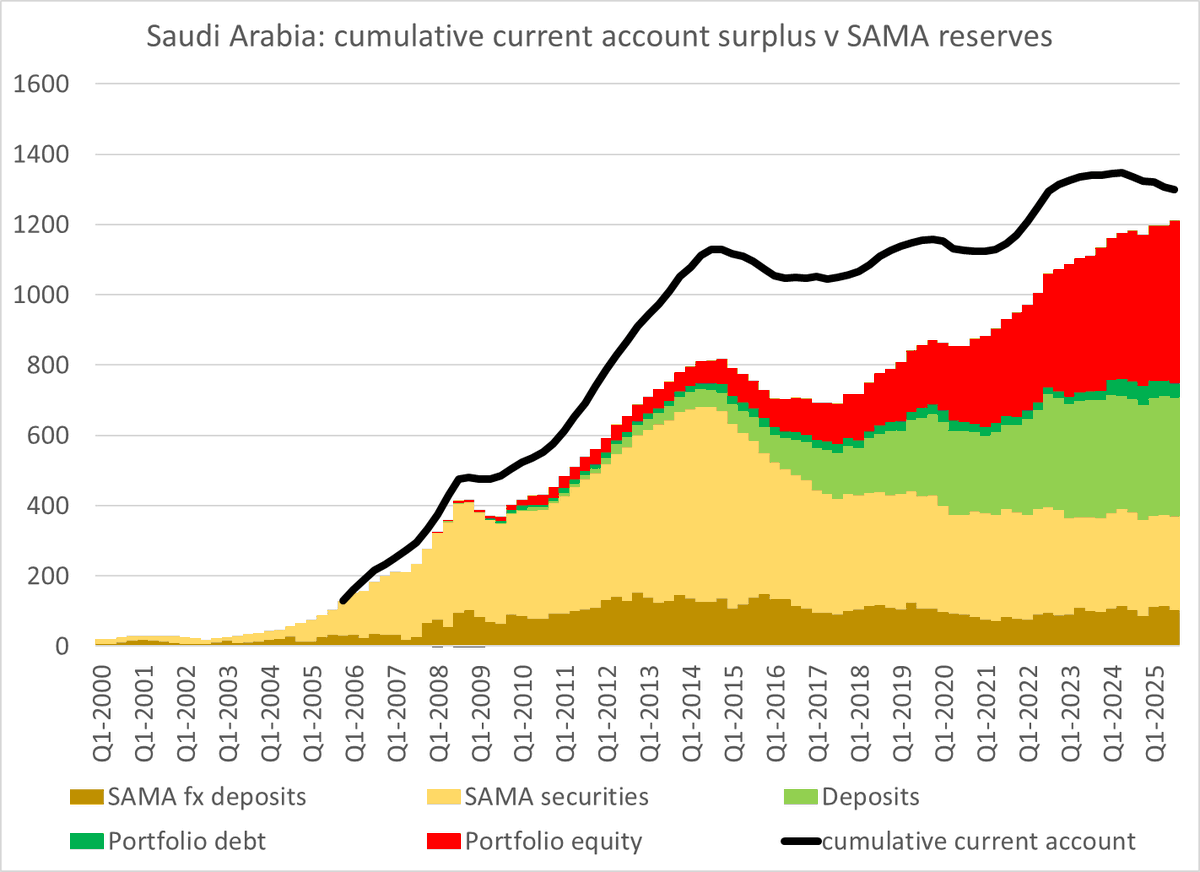

And most "petro-dollars" were actually "petro-equities" -- the GCC countries put the bulk of their funds not in liquid deposits/ bonds but in public equities (and in private equity via SWFs)

6/

6/

The Saudis have been so desperate to build up the size of their SWF (they have a bit of QIA/ KIA/ ADIA envy) that they borrowed in the global bond market to buy equities (not just to build NEOM, etc)

7/

7/

So its actually been a while since the Saudis were generating spare dollars for global banks to intermediate, or providing stable funding for the US fiscal deficit ... (the same is obviously also true of Russia)

8/

8/

And b/c of Saudi borrowing, the "SWF" flow (mostly an equity flow) exceeded the reduced GCC current account surplus (the UAE isn't in the quarterly IMF data, but it is a bigger version of Qatar)

9/

9/

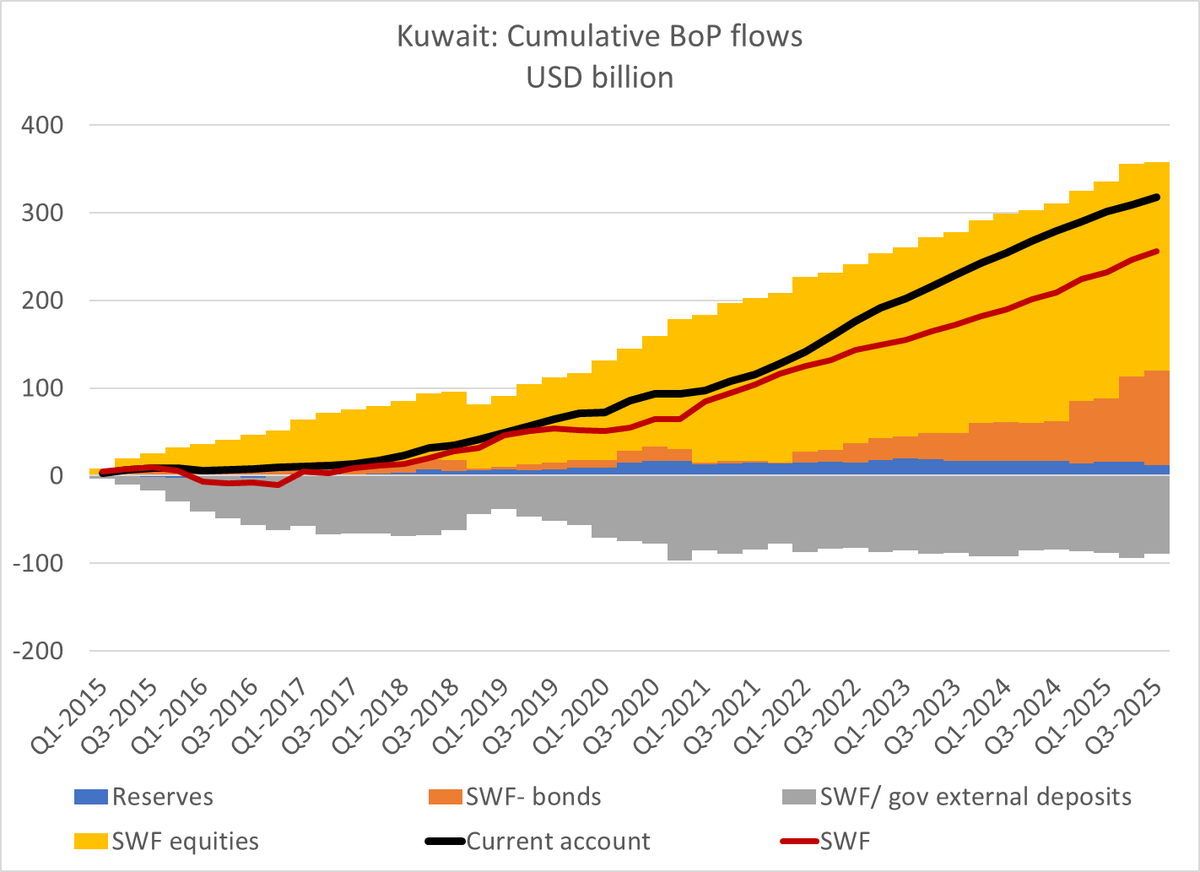

Now there are some interesting subplots inside the global data -- while most of the GCC flow is into equities, Kuwait has been buying some bonds for its SWF in the past couple of years

10/

10/

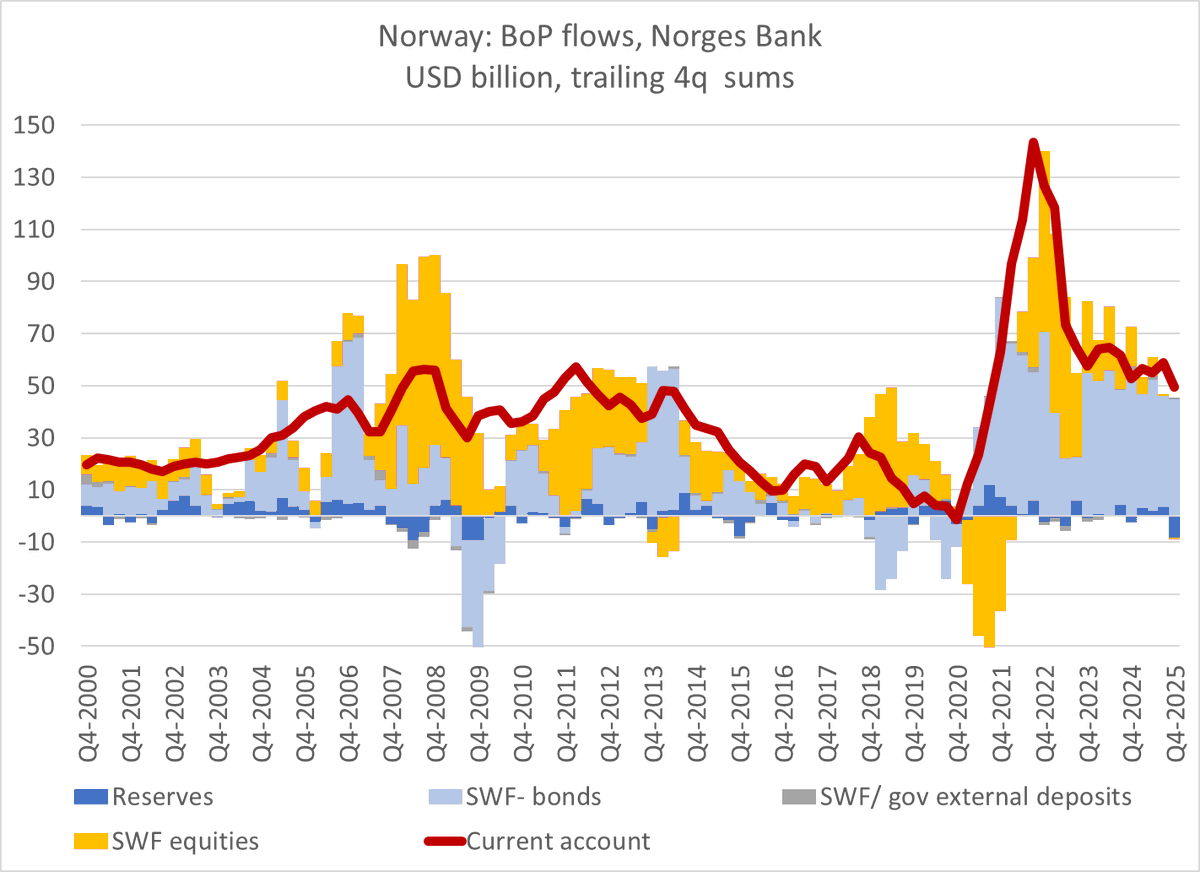

And Norway's gas driven flow (petro-krone?) has been directed toward bonds (to slightly tilted towards euros relative to its equities I think) as Norges Bank Investment Management portfolio balanced in the face of the global equity market run-up

11/

11/

But the bottom line is that going into this shock, the big surpluses were in Asia not the oil exporters ... and there wasn't a big flow into liquid offshore dollar markets from the oil exporters (there was a modest flow into equities & "AI" investments)

12/

12/

The dynamics of this shock also will be interesting -- some of the biggest winners from a standard oil shock are the Gulf countries whose exports are now cut off (Iraq, Kuwait, Qatar, UAE = ~ 10 mbd of exports). Some may need to dip into reserves and other buffers .

13/

13/

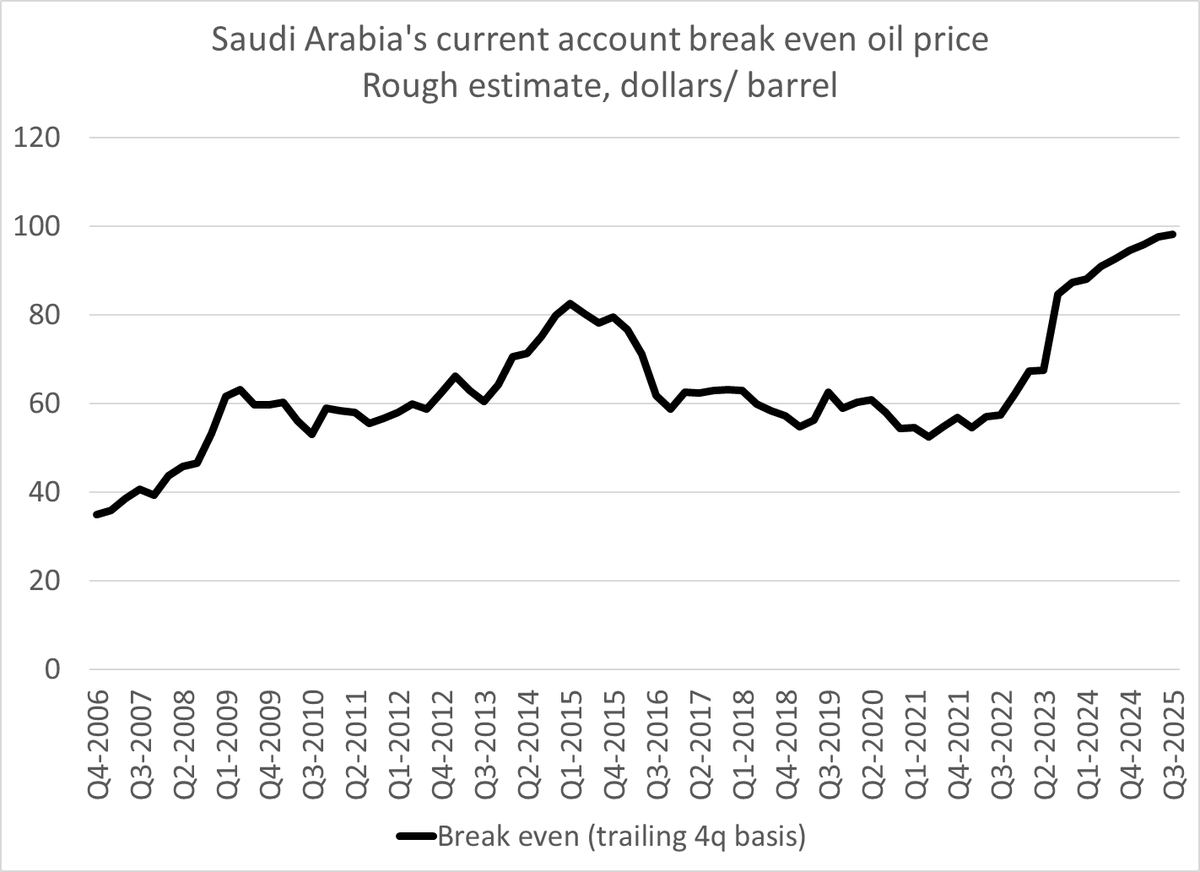

The Saudis may be OK despite a high break even oil price if they can move enough oil through the East-West pipeline to keep their oil exports above 5 mbd ... a higher price offsets lower volumes. But they don't be generating a big surplus unless oil moves a lot higher

14/

14/

The big windfall gains go to Russia (of course), and the central Asian oil exporters (Kazakhs, Azeris, etc) -- Central Asia and Russia generate like 10 mbd of exports, so every $10 increase in traded oil = $35 b in additional proceeds over a year

15/

15/

Other big winners -- Norway of course, especially with the loss of Qatari gas. The Norwegians might want to consider stepping up their financial contributions to say Ukraine and otherwise using their windfall to do more than just buy US bonds!

16/

16/

Canada and the oil exporting countries of South America (Colombia, Ecuador, Brazil even Argentina modestly) also will get a windfall -- collectively they export ~ 10 mbd ...

17/

17/

Now the Canadians use their oil proceeds mostly to buy manufactured goods, and given Trump's rhetoric, it isn't clear that the "51st state/ fastest path to Greenland" won't put its financial elbows up and limit any increase in US exposure ...

18/

18/

And for Brazil and Colombia the funds will go to cover their current account deficits (which in Brazil's case is a lot of interest on its existing external debt) ... they aren't gonna generate petrodollars in big sums ...

19/

19/

And if higher prices lead the US to, well, drive a bit less and conserve energy, the US could become a meaningful oil exporter (now most of its energy exports are LNG) ... and reduce its external borrowing need ...

20/

20/

But the first order impact of this shock is a bigger surplus in (for now sanctioned except for the oil at sea) Russia -- which won't be stashing its loot in dollars (at least not until Witkoff works some magic ... ) ...

21/

21/

And a smaller surplus in Europe (investment income will go to paying the energy import bill) and a much smaller surplus in Asia ...

22/

22/

That means fewer offshore dollars sloshing around Hong Kong and Singapore and making their way into global markets ... so fewer eurodollars ...

23/

23/

But the Asian surplus is so big ($1.4 trillion using the reported Chinese data) & was rising before the shock on the back of AI chip demand. So it won't go away. $10 a barrel is ~$70b on the Asian surplus ballpark so even a $100 a barrel shock only cuts the aggregate in 1/2

That's my take on the big first order effects on the big regions of the global economy --

There will of course also be important impacts on all the middle powers that are oil importers (Turkey, India, Pakistan, etc) ...

25/25

There will of course also be important impacts on all the middle powers that are oil importers (Turkey, India, Pakistan, etc) ...

25/25

• • •

Missing some Tweet in this thread? You can try to

force a refresh