Three big picture observations about the oil surplus (petrodollars/ petroeuros/ petroequities are all downstream of this) pre Hormuz

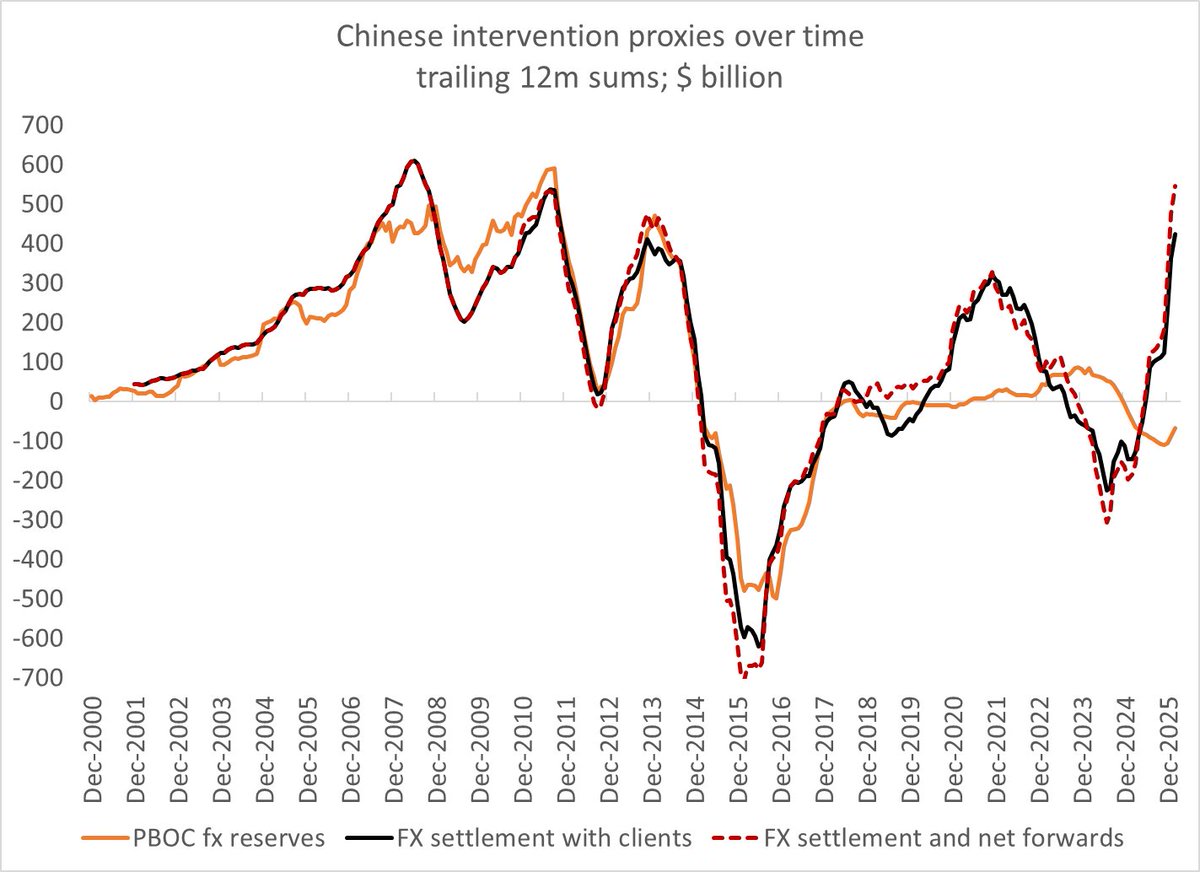

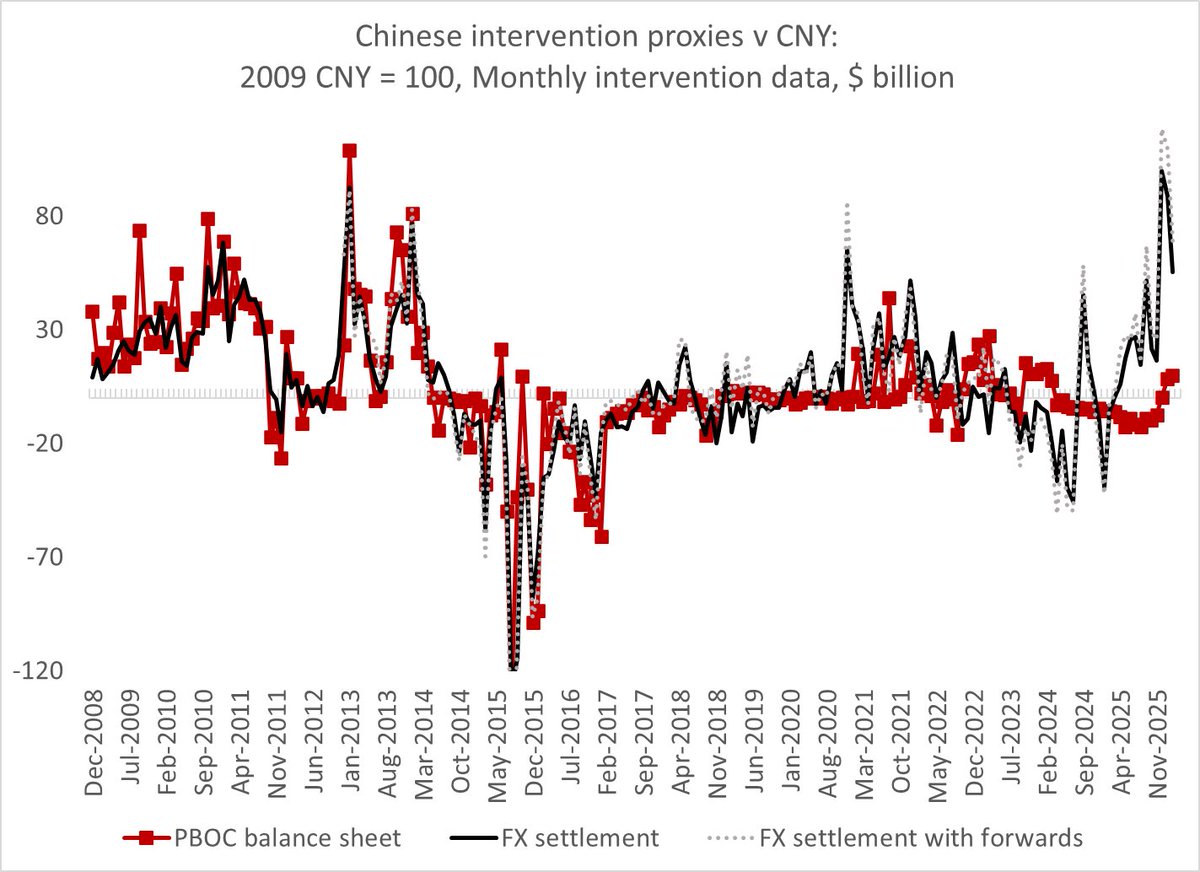

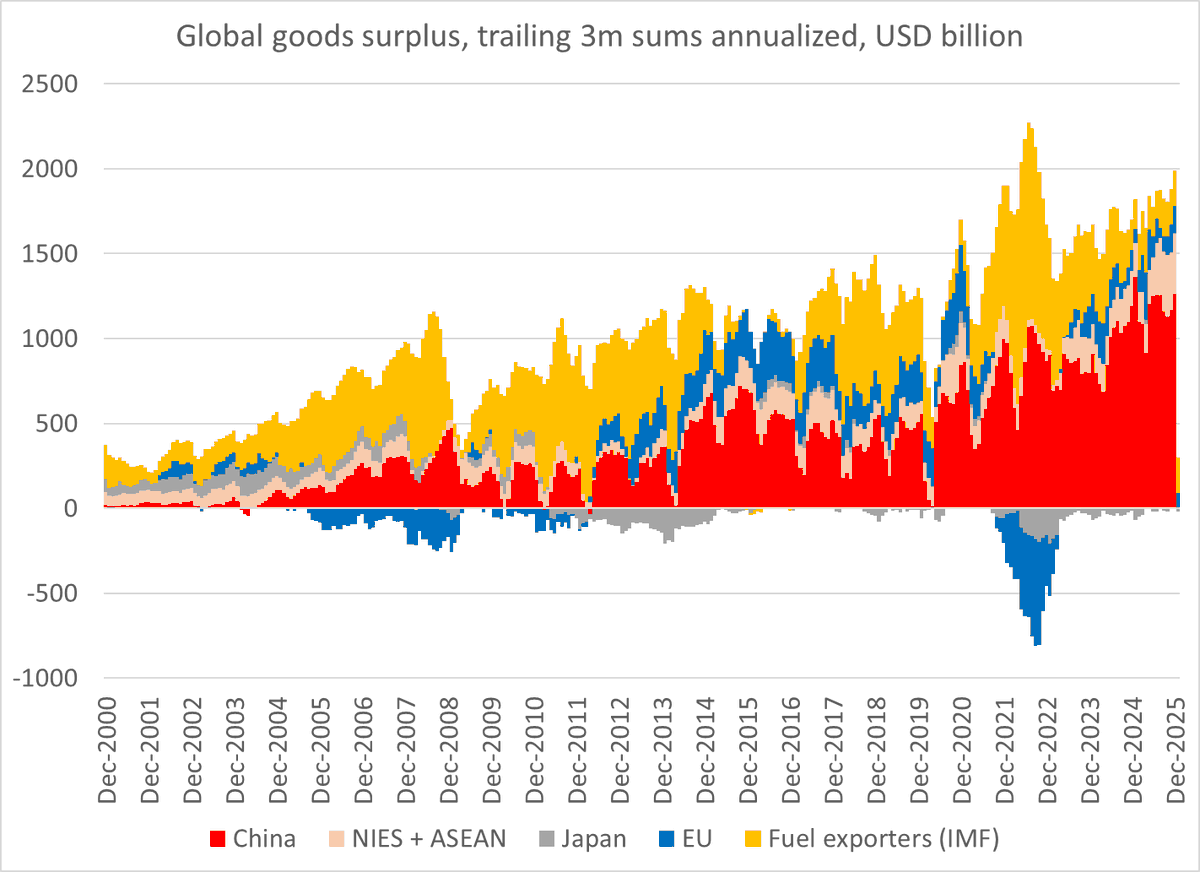

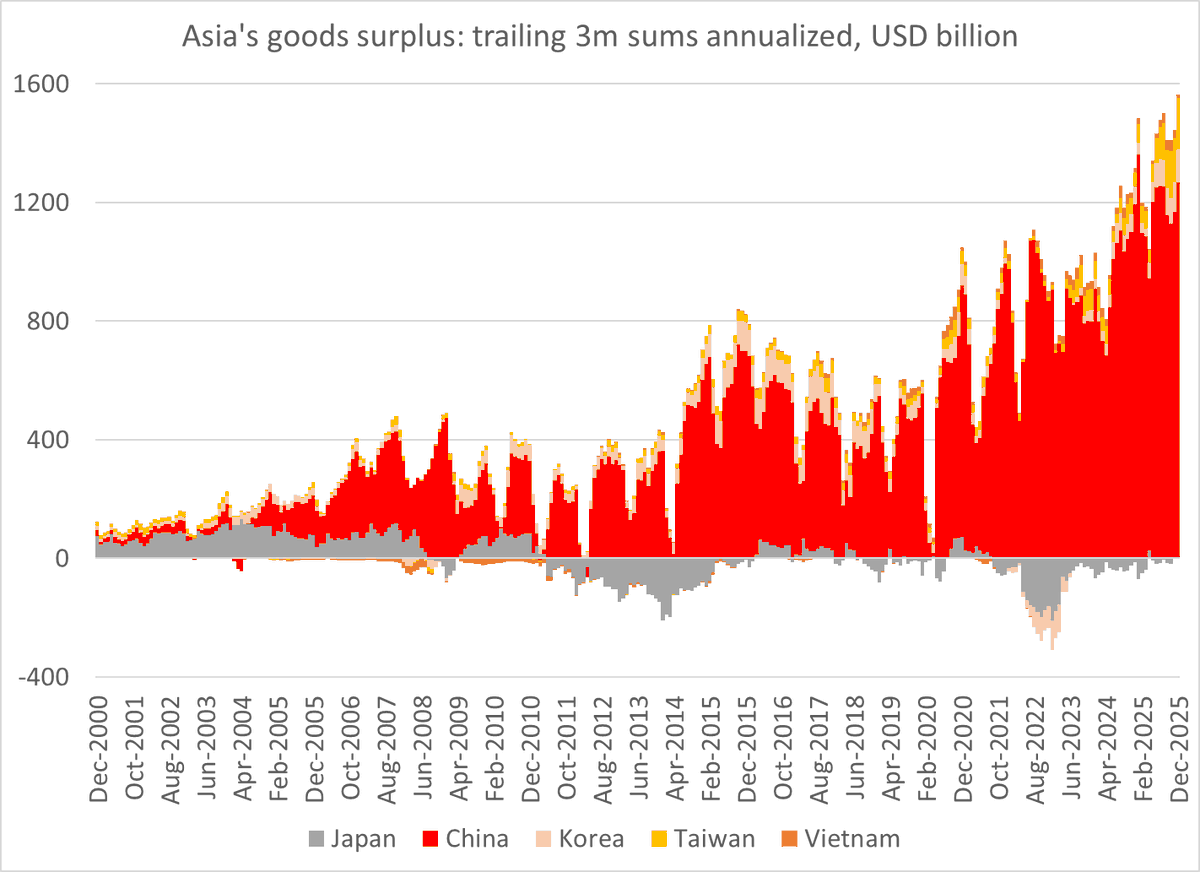

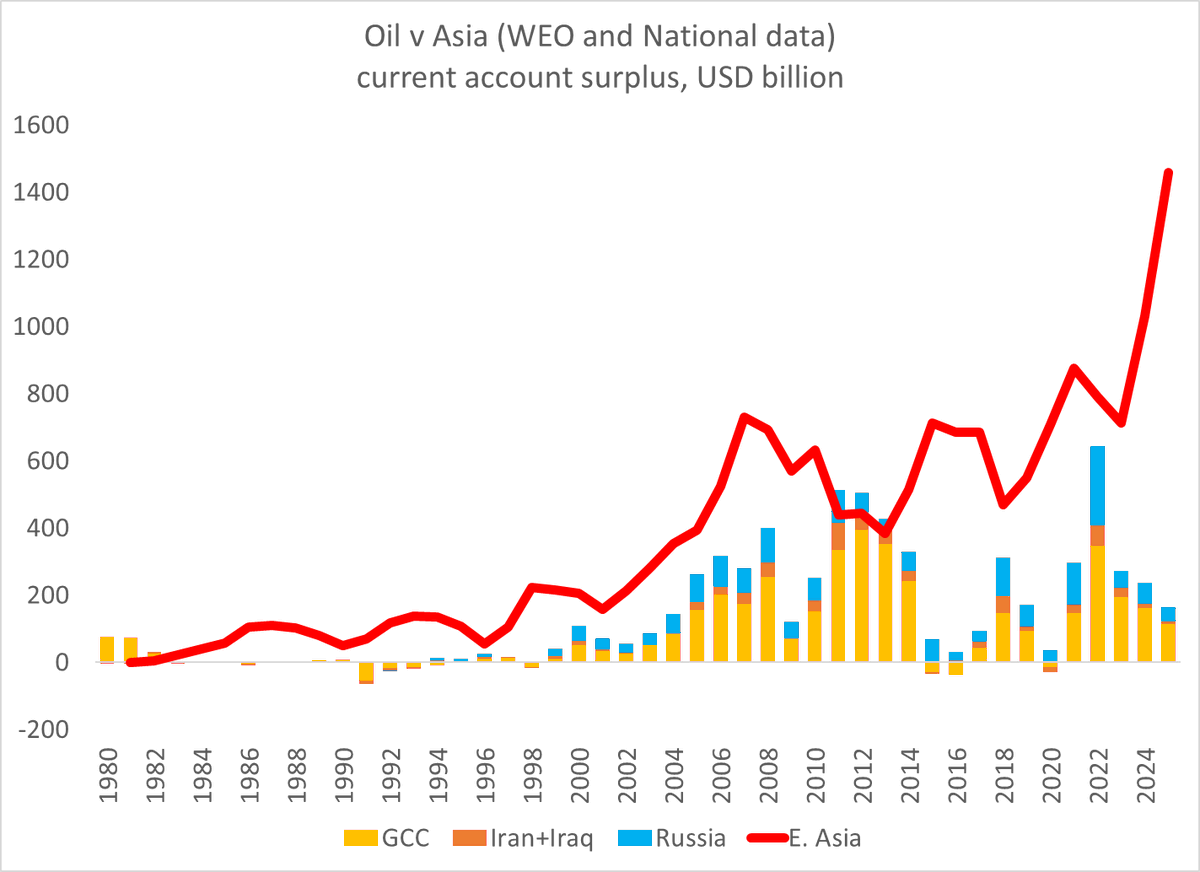

A) The oil surplus is modest relative to the surplus in Asia. Chinese state banks and offshore deposits of Chinese exporters are way bigger

1/

A) The oil surplus is modest relative to the surplus in Asia. Chinese state banks and offshore deposits of Chinese exporters are way bigger

1/

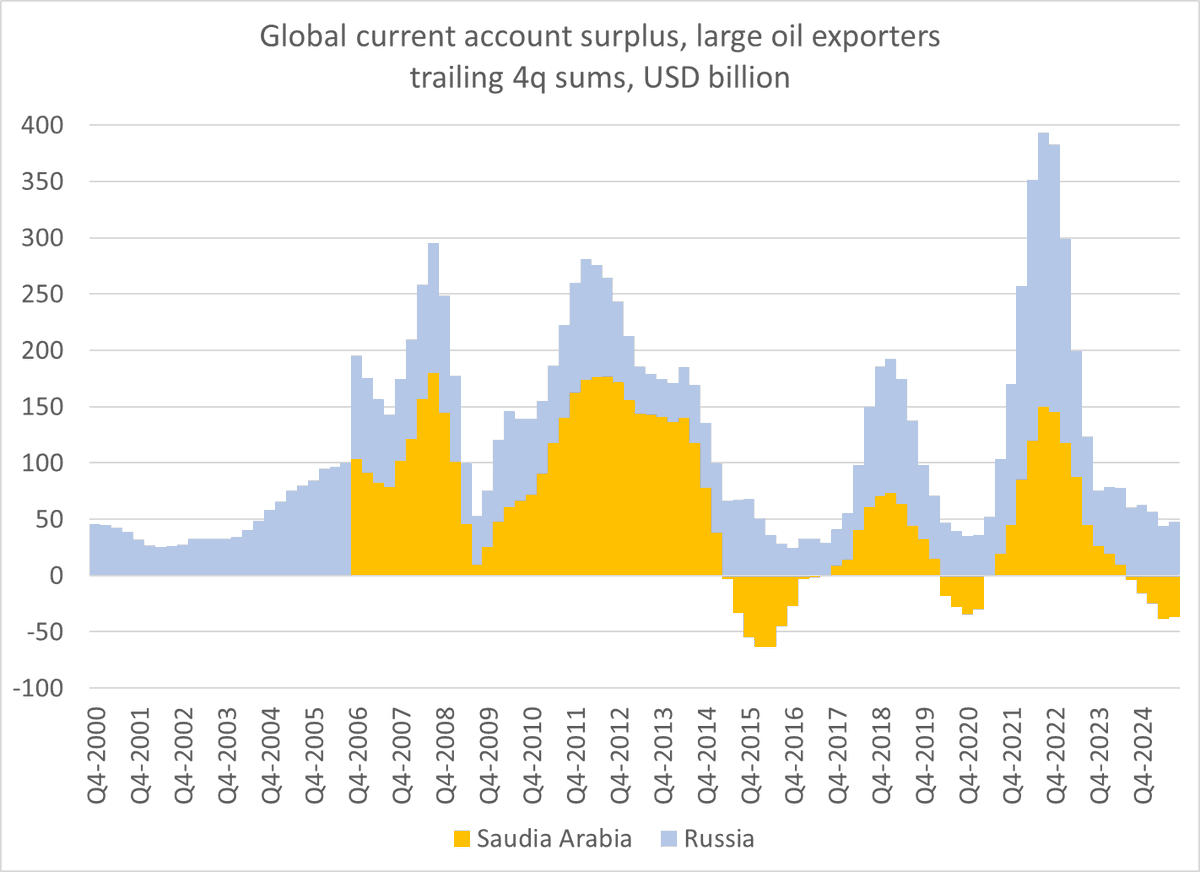

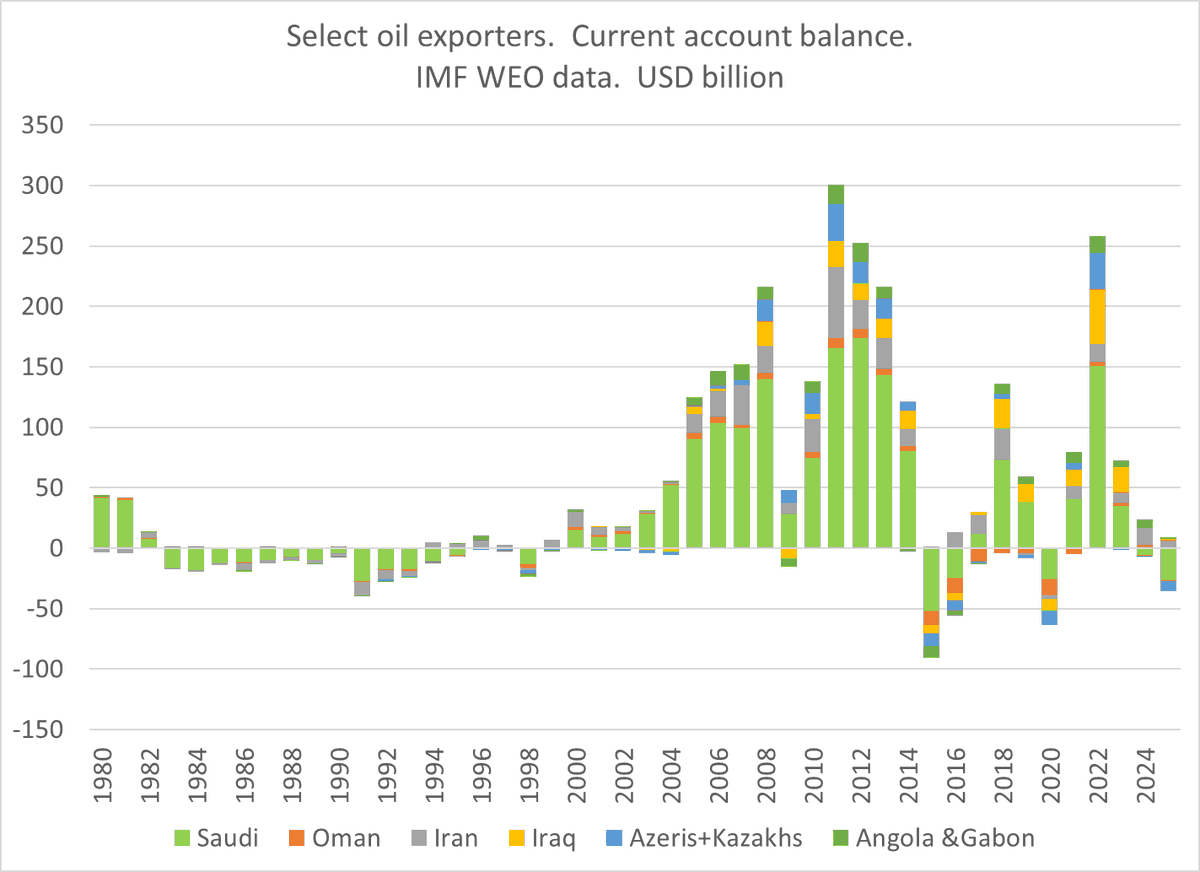

B) Most oil exporters are in deficit or run only modest surpluses with oil in the 60s or 70s. That importantly includes Saudi Arabia, which now has a BoP break even in the 90s

2/

2/

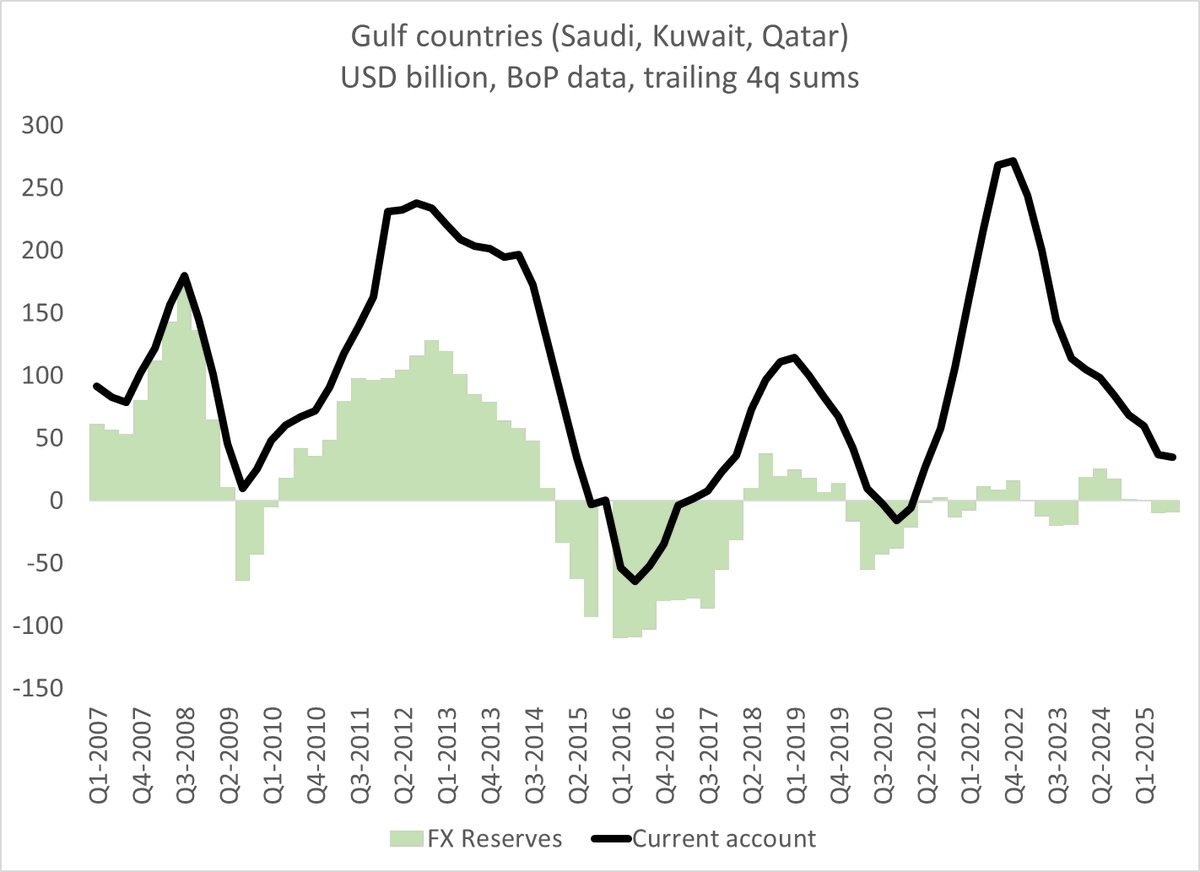

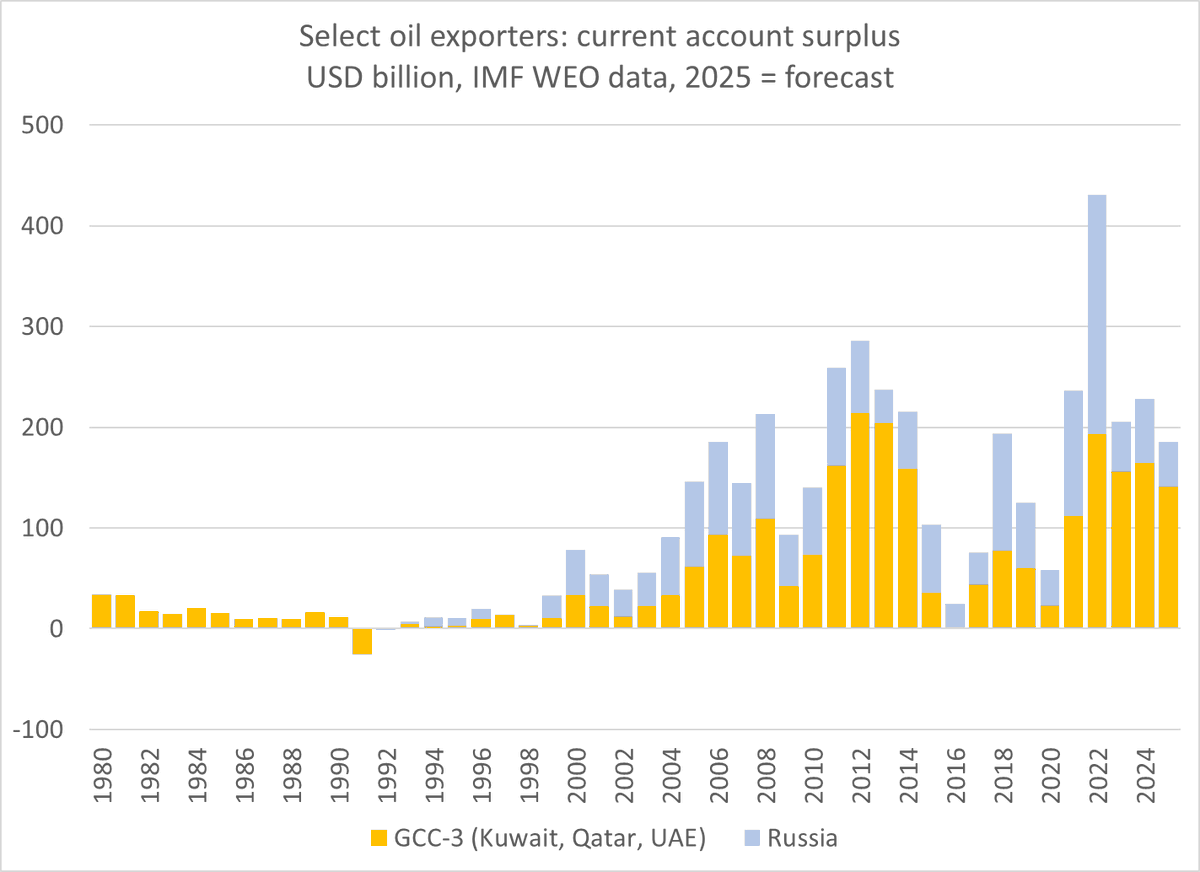

C) The remaining surpluses are concentrated in Russia (tho its surplus has fallen), frugal Norway and the GCC countries with large SWFs -- who tend to invest most of their surplus in equities (Kuwait is a bit of an exception, recent bond inflows

3/

3/

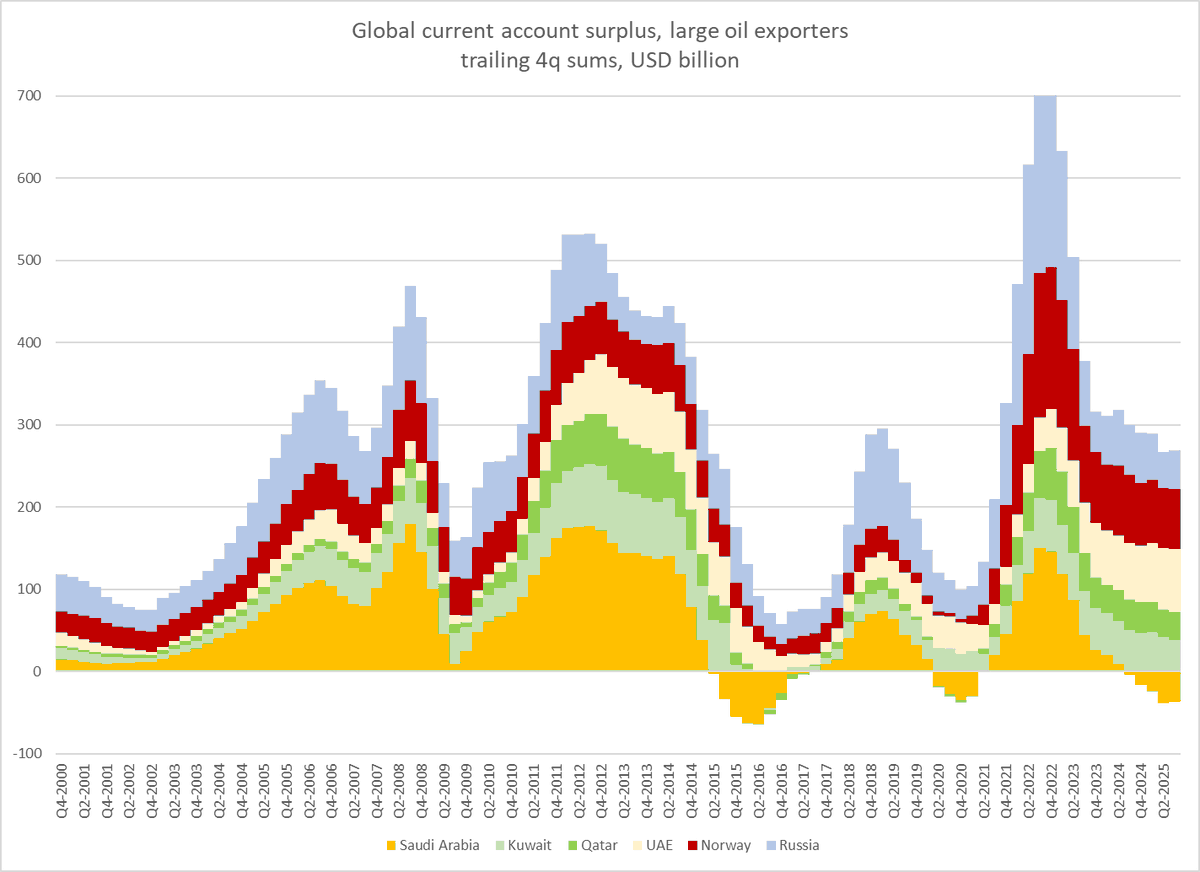

Obviously, the Gulf countries with large SWFs are among the countries most impacted by the de facto closing of the strait -- the winners from the current oil shock will be the oil exporting countries outside the GCC

4/

4/

And the biggest data gap comes from the UAE.

The IMF WEO data implies it has among the biggest remaining surpluses, but the UAE's BoP data is thin and out of date, so the IMF forecast could be off. And I would bet the bulk of its surplus now is investment income

5/5

The IMF WEO data implies it has among the biggest remaining surpluses, but the UAE's BoP data is thin and out of date, so the IMF forecast could be off. And I would bet the bulk of its surplus now is investment income

5/5

• • •

Missing some Tweet in this thread? You can try to

force a refresh