An exploration of the February US trade data -- which got buried a bit by the anniversary of liberation day.

A key question -- will the weakness in non "AI" imports in the last 12ms reverse now that uncertainty around tariff levels has disappeared.

A key question -- will the weakness in non "AI" imports in the last 12ms reverse now that uncertainty around tariff levels has disappeared.

https://twitter.com/Brad_Setser/status/2039909366103523351

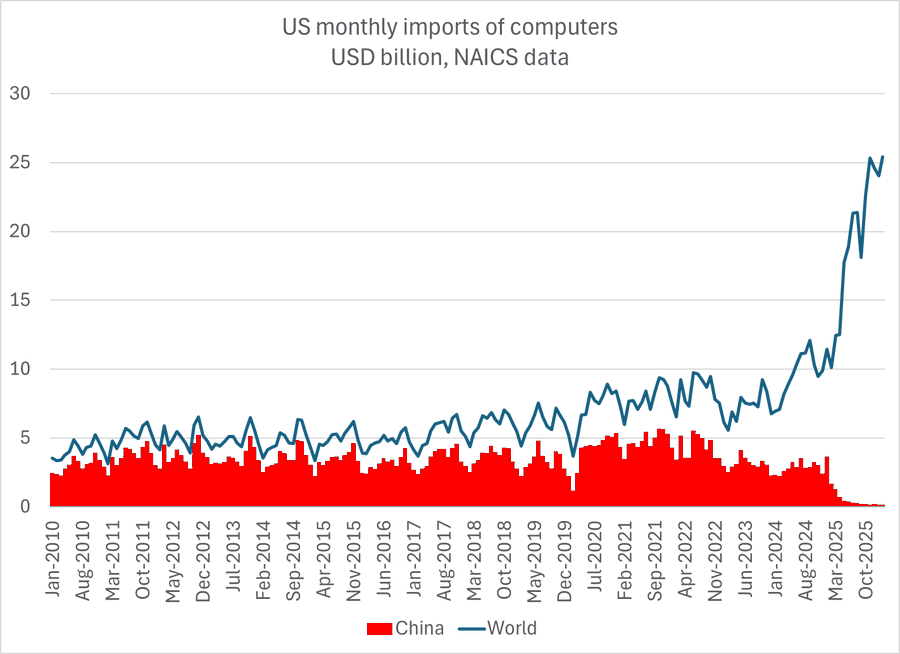

Imports of computers are up massively (tho not from China) and show no sign of slowing down -- that will mechanically pull the true trade deficit (setting gold flows aside) w/o a big sustained fall in other imports

Pharma/ Irish imports have been weak for a few months now -- probably unwinding front running but I also wonder if the tariff threat led some companies to "unbundle" pricing at the border, & lower their declared import price while charging more for the IP separately

this was under consideration before the Trump team started doing the Trump Rx deals -- it would preserve "Irish" tax structures but lower Irish goods exports/ US customs imports and raise Irish service exports/ US services imports ... too soon to tell if it is happening

• • •

Missing some Tweet in this thread? You can try to

force a refresh