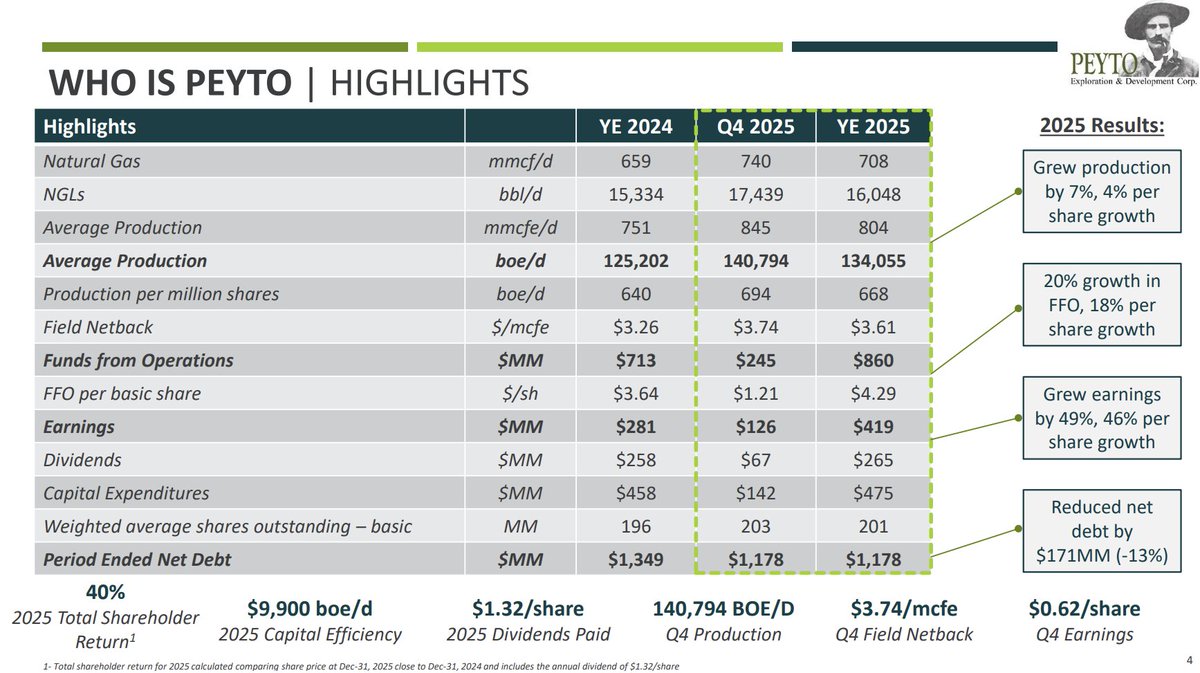

🚨New $PEY.to Presentation 🚨

Lots of 2025 Comps

Here are some of the highlights 🧵1/x

✅Production up 4%

✅FFO up 18%

✅Earnings up 46%

✅Debt down $171 million 13%

Lots of 2025 Comps

Here are some of the highlights 🧵1/x

✅Production up 4%

✅FFO up 18%

✅Earnings up 46%

✅Debt down $171 million 13%

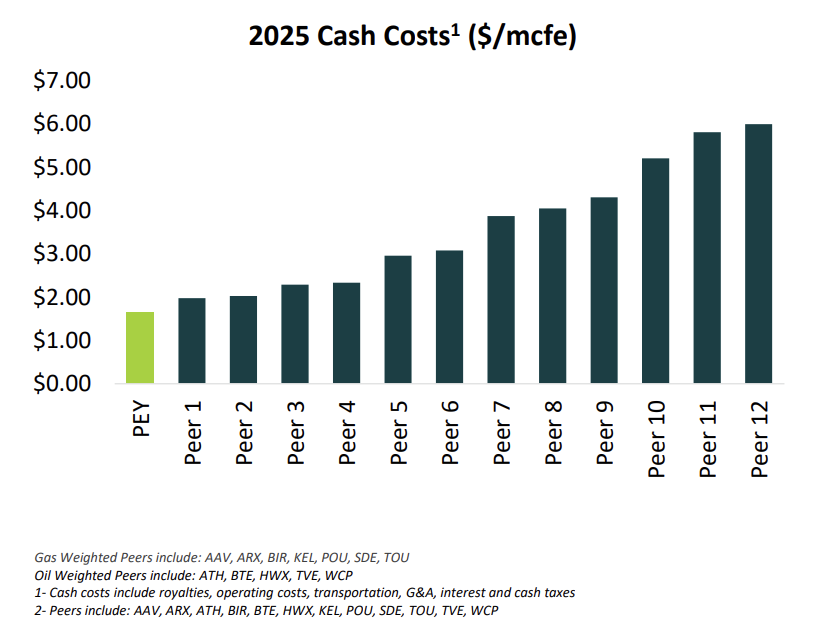

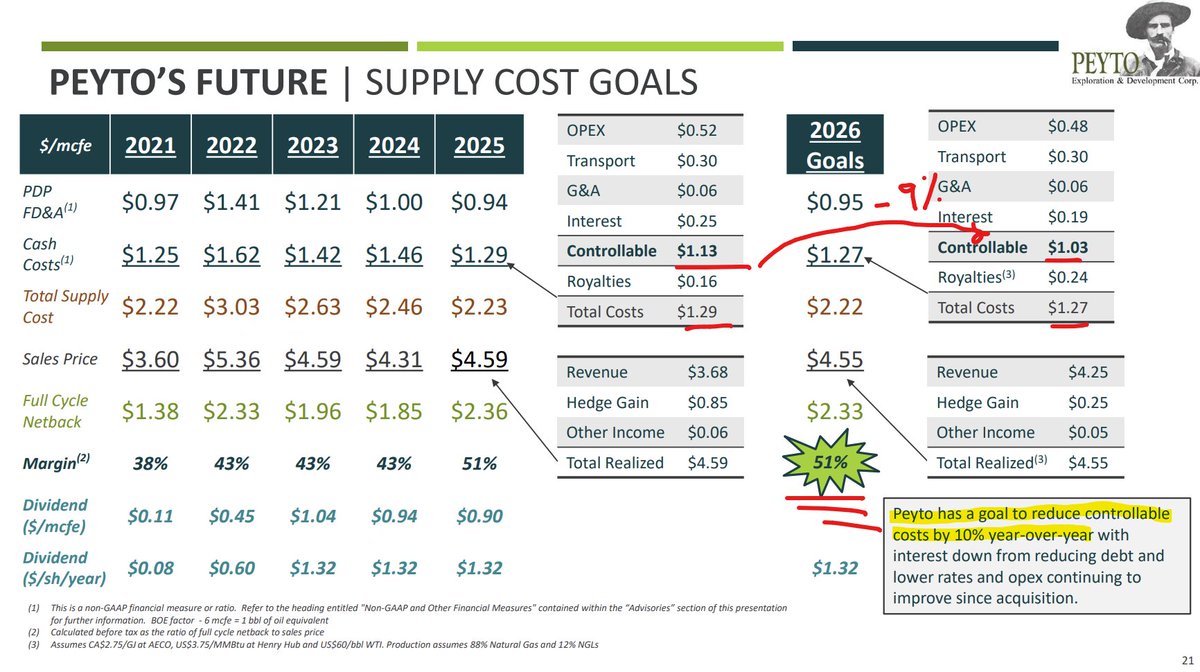

Cash Cost are still the lowest in the industry & they reduced Op Costs by 10% last year.

Which leads too... higher returns 🚀

2/x

Which leads too... higher returns 🚀

2/x

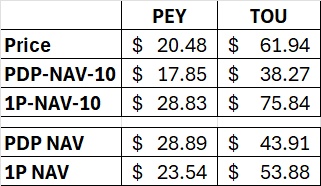

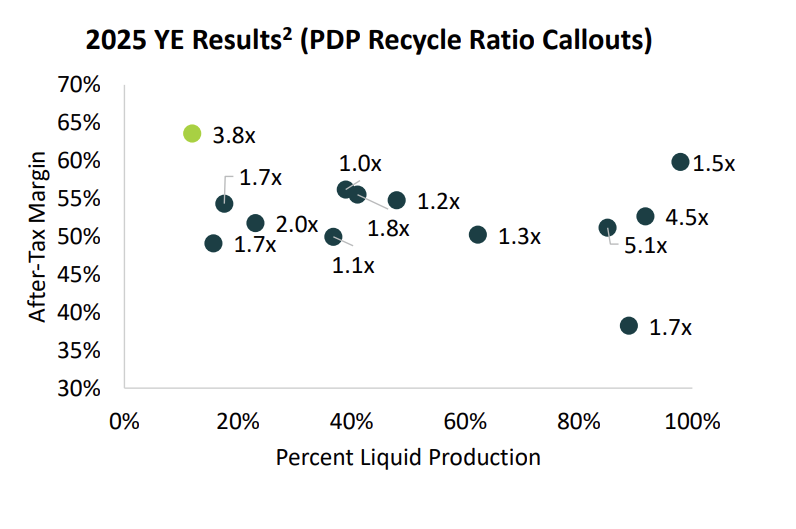

PDP recycle ratios are not even close. After tax margins are a runaway - even when compared to the oil names.

Don't forget -> Profitability drives returns!

Even unhedged $PEY.to PDP recycle ratio was 2.9x - double their gas peers 😂

3/x

Don't forget -> Profitability drives returns!

Even unhedged $PEY.to PDP recycle ratio was 2.9x - double their gas peers 😂

3/x

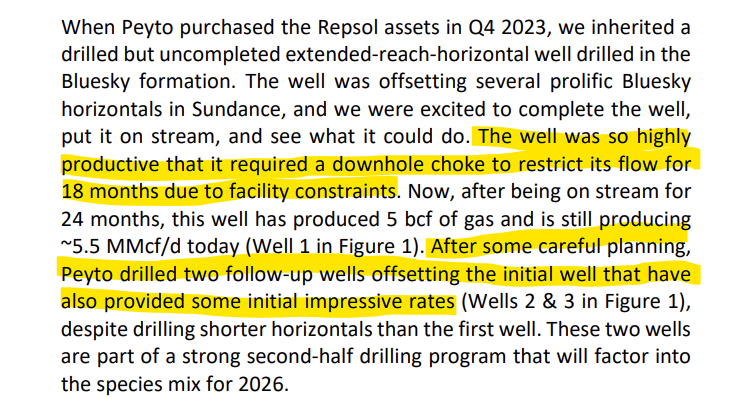

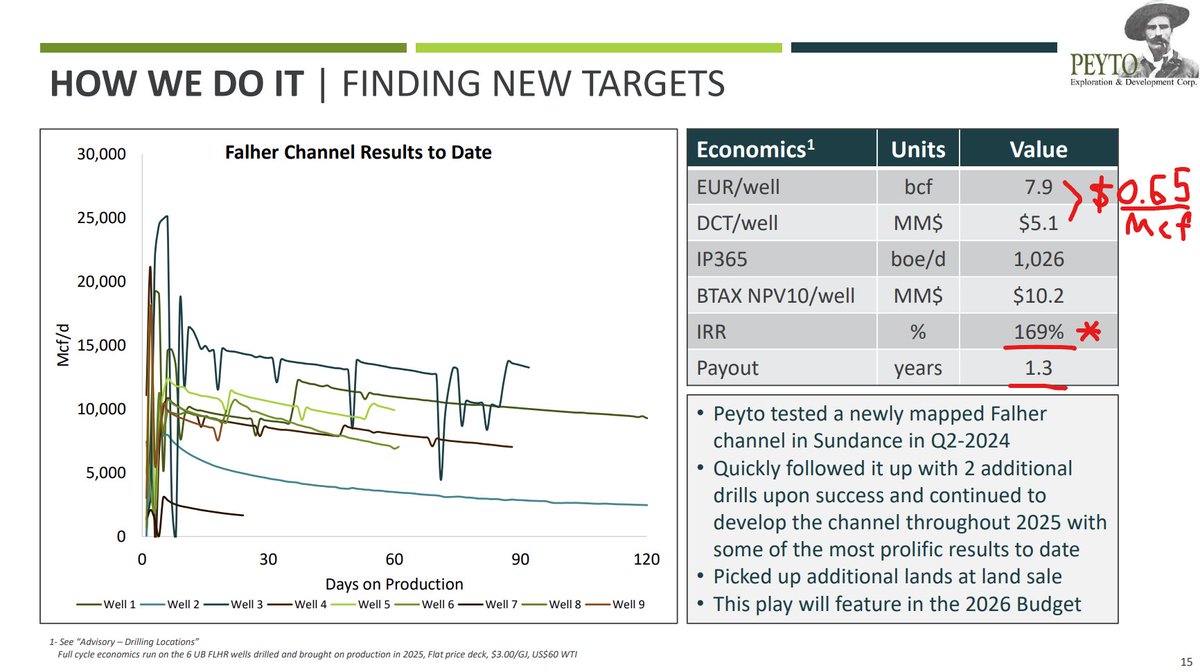

$PEY.to highlights the new Falher channel found in the middle of Sundance

This new trend is adding reserves very, very cheap at $0.65/mcf

These wells are generating a 169% rate of return & Payout in 1.3 yrs 🚀

4/x

This new trend is adding reserves very, very cheap at $0.65/mcf

These wells are generating a 169% rate of return & Payout in 1.3 yrs 🚀

4/x

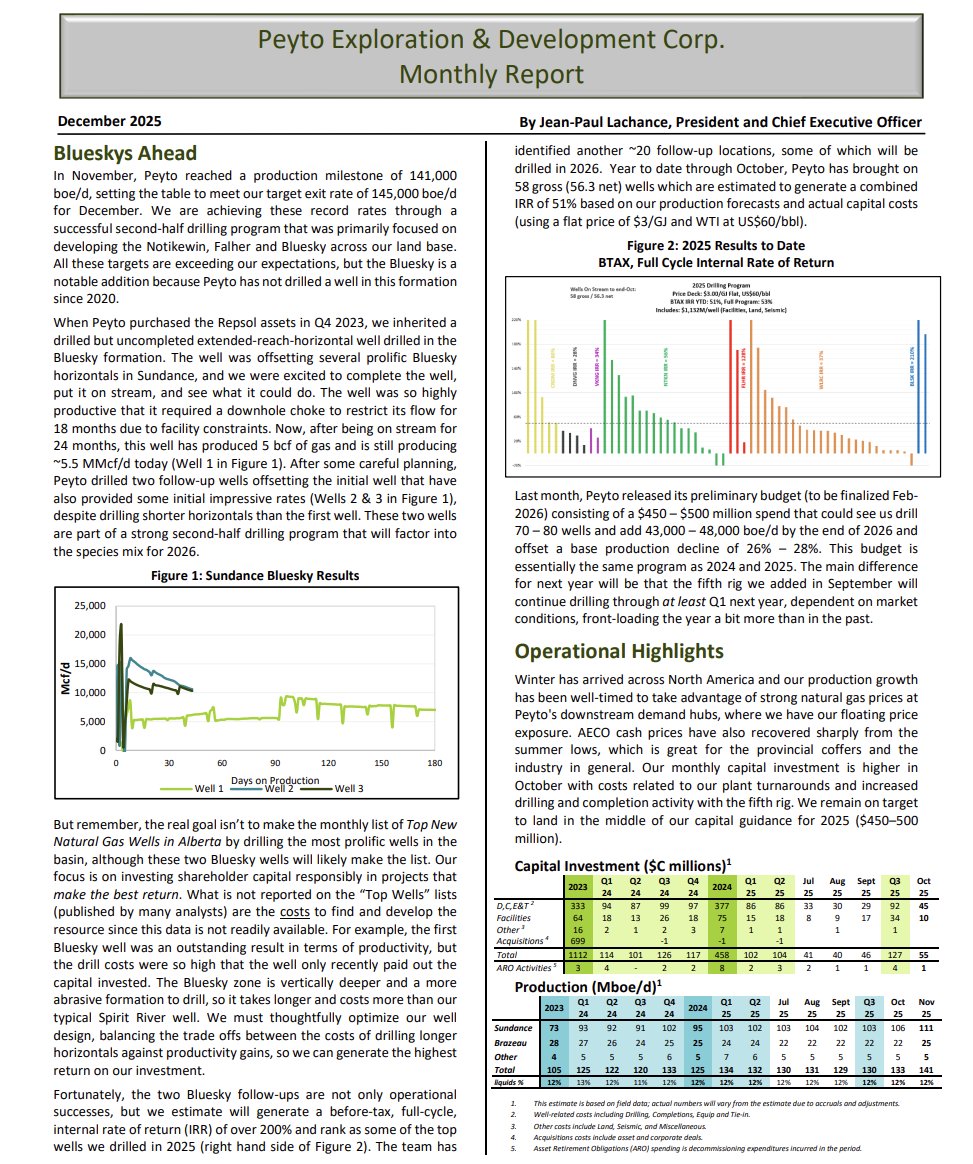

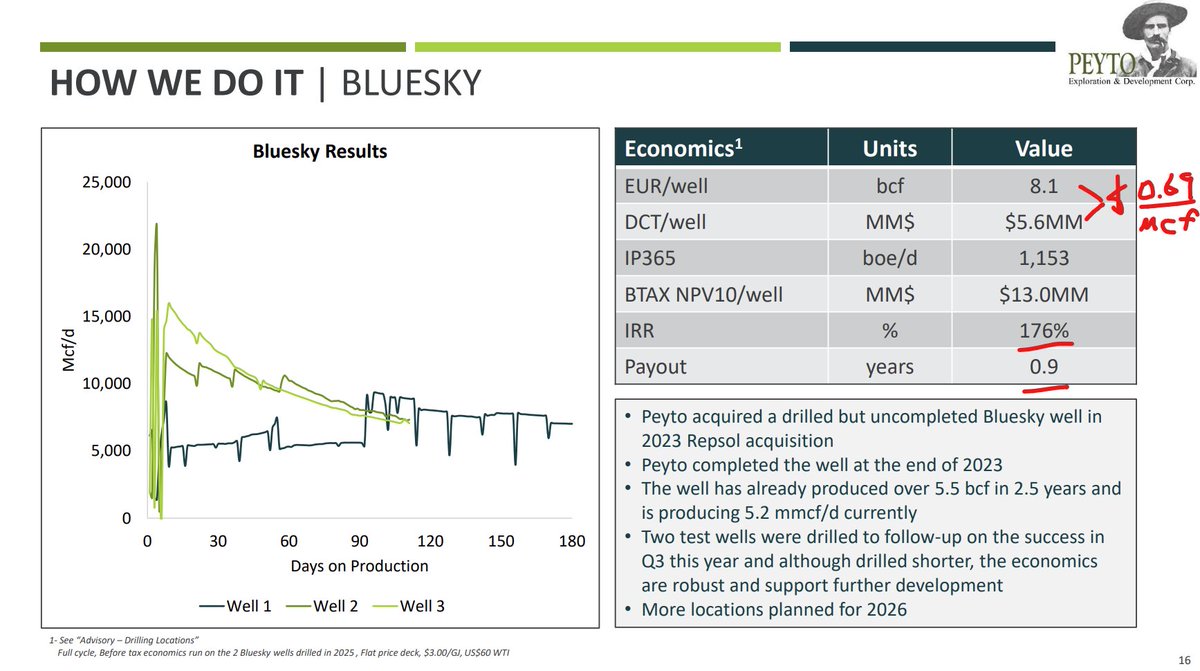

This was a gift from Repsol - an acquired but uncompleted Bluesky well - Peyto completed in 2023

That initial well was choked but has already produced 5.5 bcf in 2.5 yrs & still producing 5.2mmcfd

Follow up wells at $0.69/mcf, 176% IRR & payout in under a year 🚀

5/x

That initial well was choked but has already produced 5.5 bcf in 2.5 yrs & still producing 5.2mmcfd

Follow up wells at $0.69/mcf, 176% IRR & payout in under a year 🚀

5/x

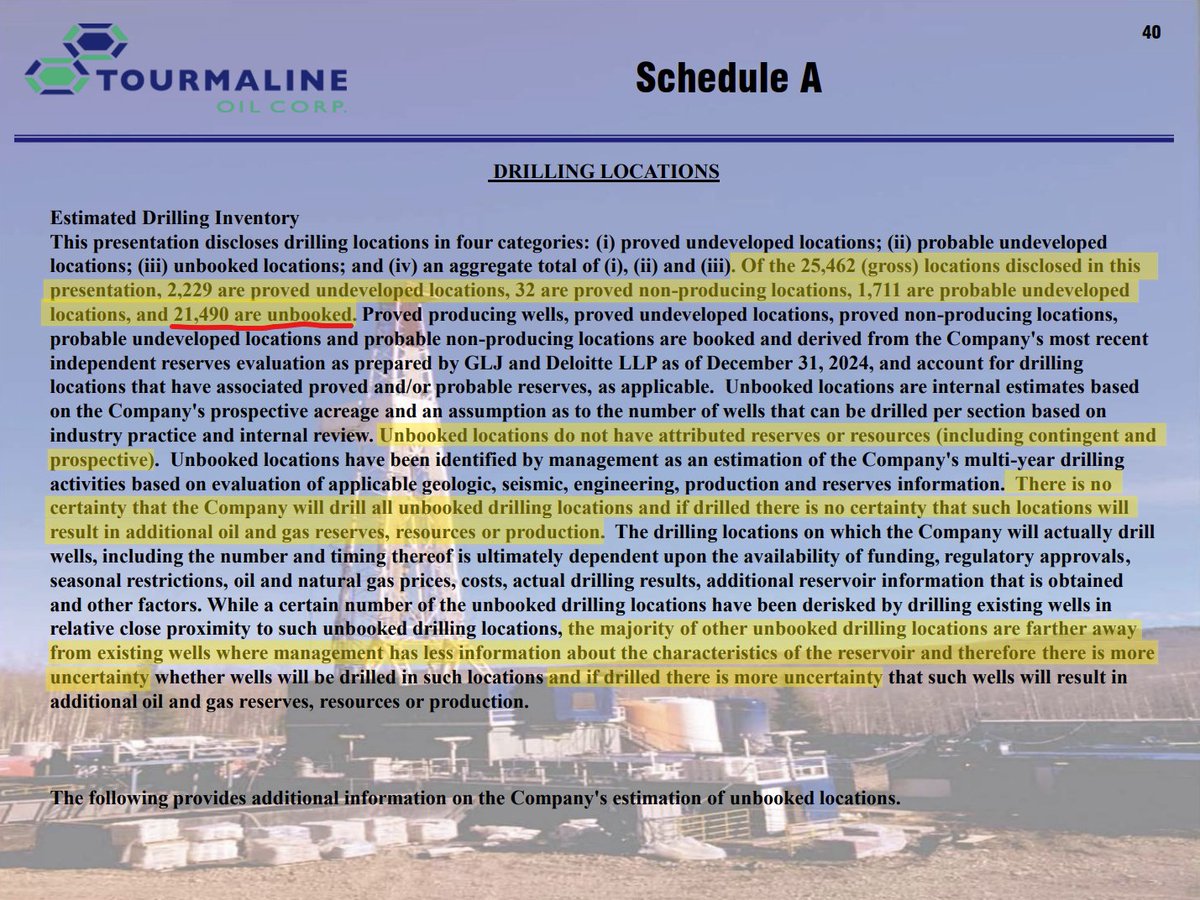

Despite what the haters say, Peyto has over 1600 booked locations across the deep basin stack - enough for 20-25 years of inventory

No need for 75 years of inventory b/c that would waste cash today. The NPV at 10% of a CF in 75 years is precisely $0.00 (not a typo🤣)

6/x

No need for 75 years of inventory b/c that would waste cash today. The NPV at 10% of a CF in 75 years is precisely $0.00 (not a typo🤣)

6/x

🚨Very Important Slide - 2026 Goals🚨

2026 looks like a repeat of 2025. Goal is to cut controllable cash costs by 10% - keeping total costs flat on higher royalties ✅

Intelligent investors will note here that $Pey.to earnings are understated by about $110 million 😀

7/x

2026 looks like a repeat of 2025. Goal is to cut controllable cash costs by 10% - keeping total costs flat on higher royalties ✅

Intelligent investors will note here that $Pey.to earnings are understated by about $110 million 😀

7/x

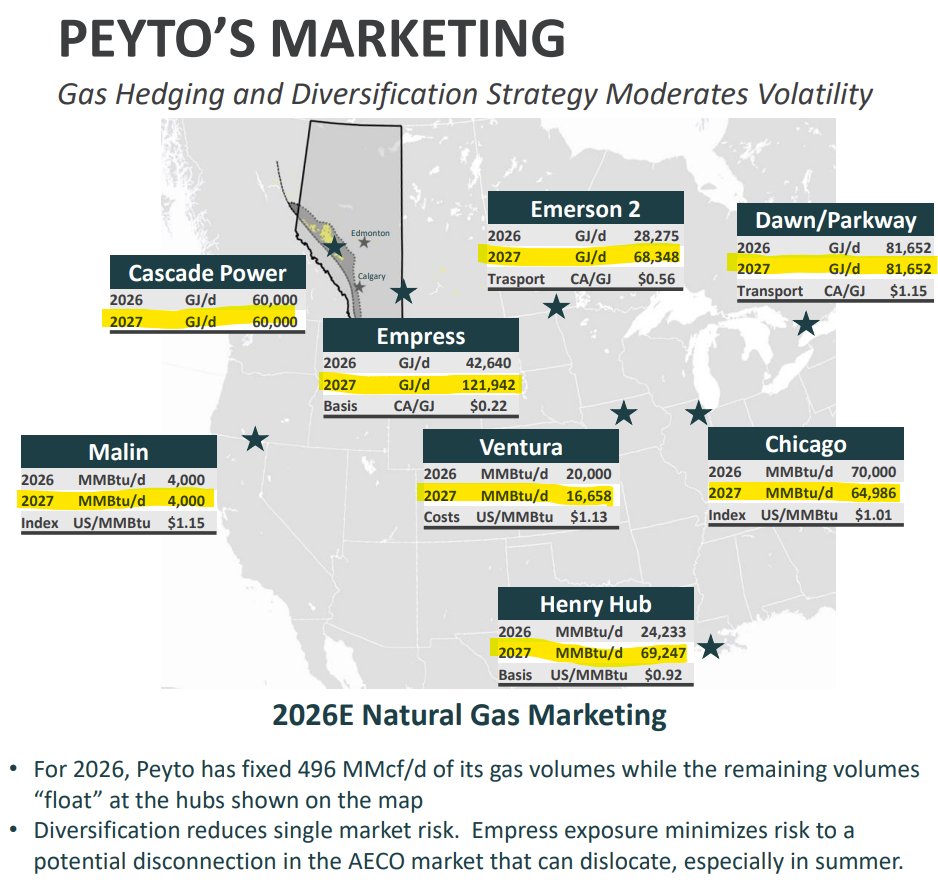

Like many predictions in the energy space, the recovery of AECO gas prices with LNG Canada startup has failed to materialize.

Good news is $PEY.to doesn't have AECO exposure in 2026 and marginal exposure in 2027.

And almost 500 mmcfd hedged in 2026 at $4.16/mcf 🔥

8/x

Good news is $PEY.to doesn't have AECO exposure in 2026 and marginal exposure in 2027.

And almost 500 mmcfd hedged in 2026 at $4.16/mcf 🔥

8/x

• • •

Missing some Tweet in this thread? You can try to

force a refresh