Good at math. Read a lot. Financial statements tell a story. Novice excel user.

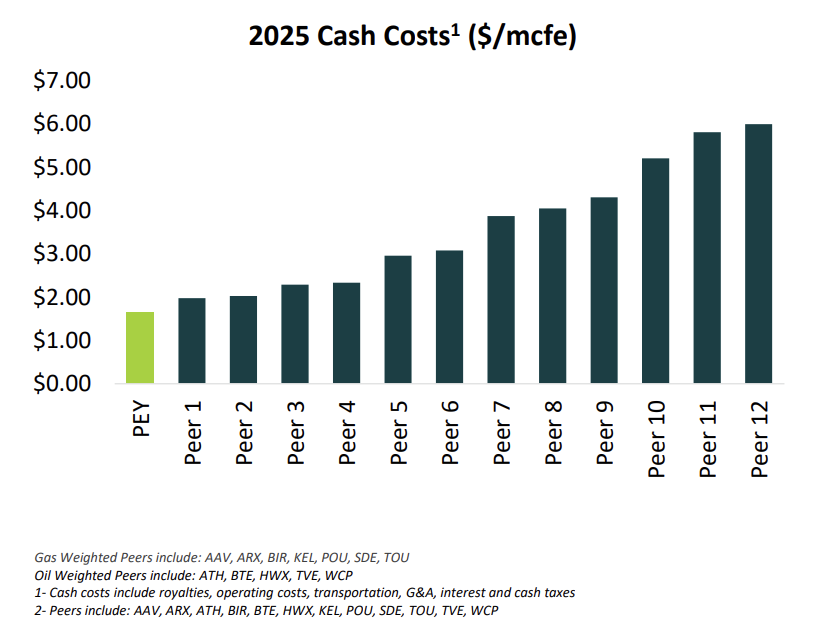

Cash Cost are still the lowest in the industry & they reduced Op Costs by 10% last year.

Cash Cost are still the lowest in the industry & they reduced Op Costs by 10% last year.

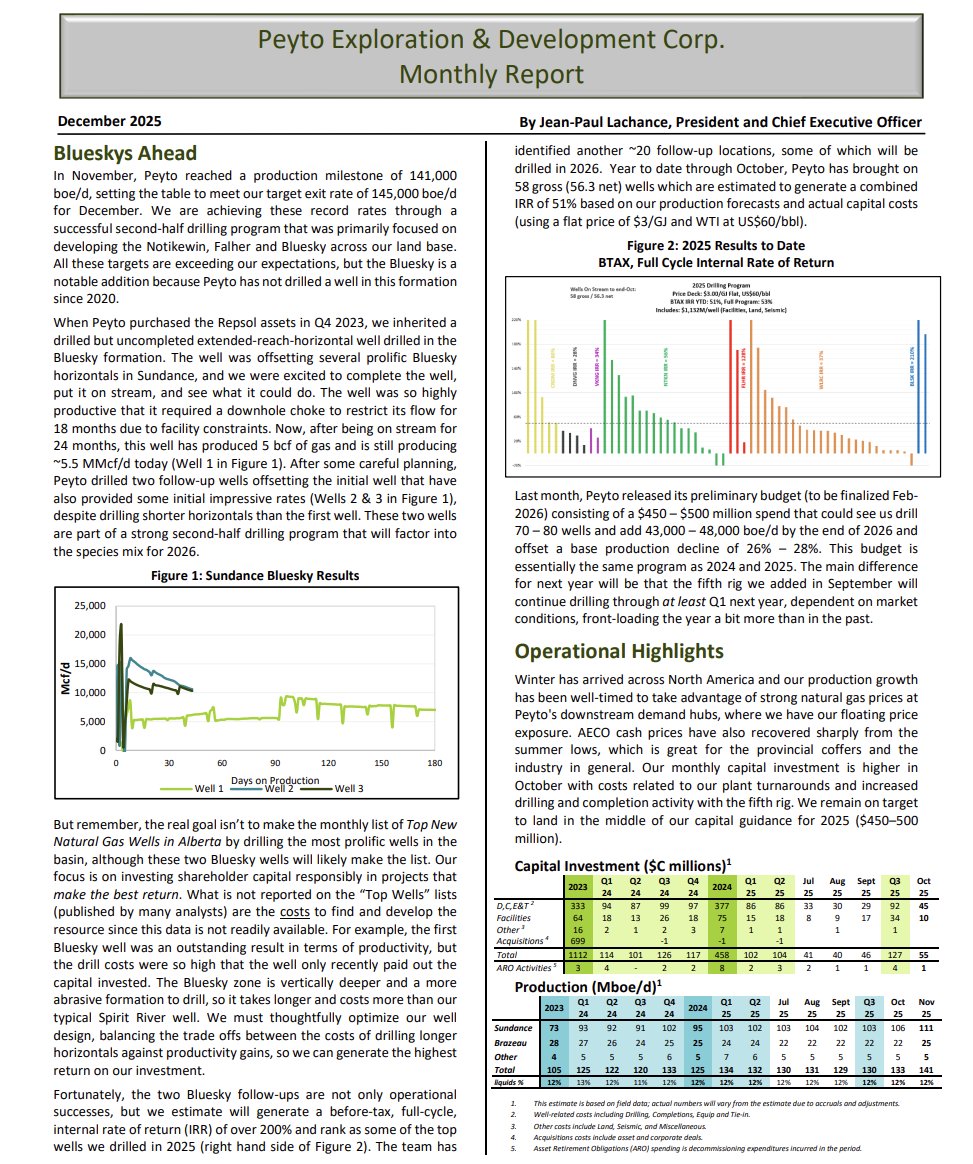

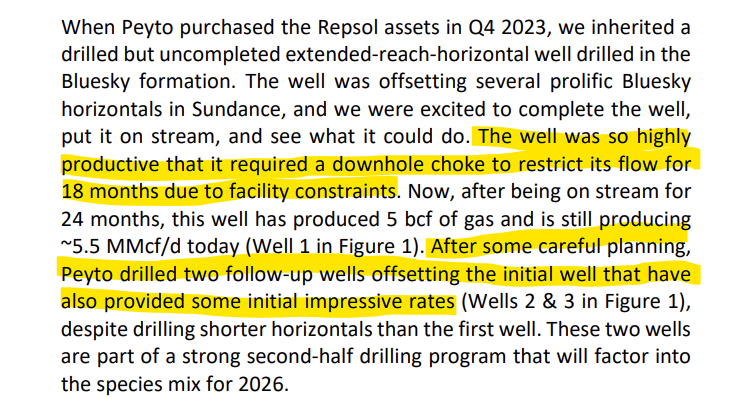

When Peyto aquired Repsol they inherited a drilled but uncompleted Bluesky ERH.

When Peyto aquired Repsol they inherited a drilled but uncompleted Bluesky ERH.

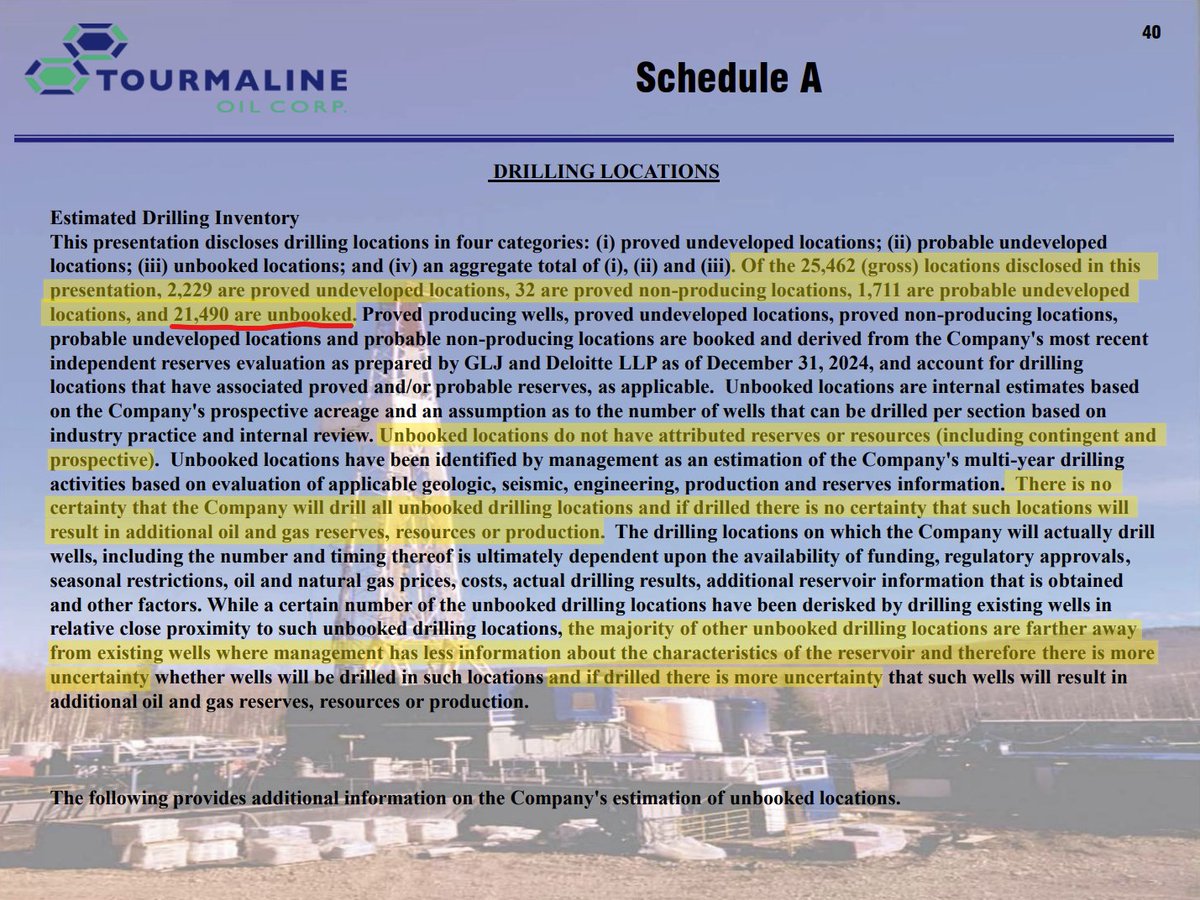

The first step of a proper analysis is to read the fine print and understand the assumptions.

The first step of a proper analysis is to read the fine print and understand the assumptions.

Breakdown of Repsol

Breakdown of Repsol

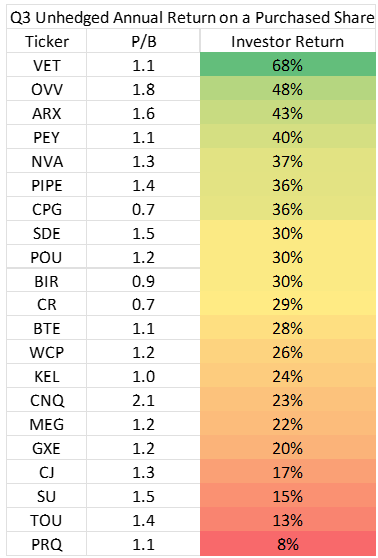

But commodity prices today are a lot lower than in Q3 2022.

But commodity prices today are a lot lower than in Q3 2022.