Net zero advocates love to claim renewables are cheaper than gas by waving around Levelised Cost of Energy (LCOE) models from Lazard, IRENA, and the UK Government’s Generation Cost 2025 report. But these models are junk. Here’s why. (1/19)

LCOE sums up all capital and operating costs over a plant’s lifetime, discounts them, and divides by total electricity generated. Result: £/MWh or p/kWh in a chart like Lazard's below. Sounds scientific… until you look closer. (2/19)

Classic LCOE compared dispatchable sources (gas, coal, nuclear, hydro) that match demand. Now it’s used for wind & solar, whose output depends on weather, not demand. A midday solar kWh when supply>demand is worthless. Peak-hour gas power is priceless. LCOE ignores this. (3/19)

LCOE does NOT compare like-with-like. Some models try adding “firming” costs for intermittency, but these fixes are partial and inadequate. (4/19)

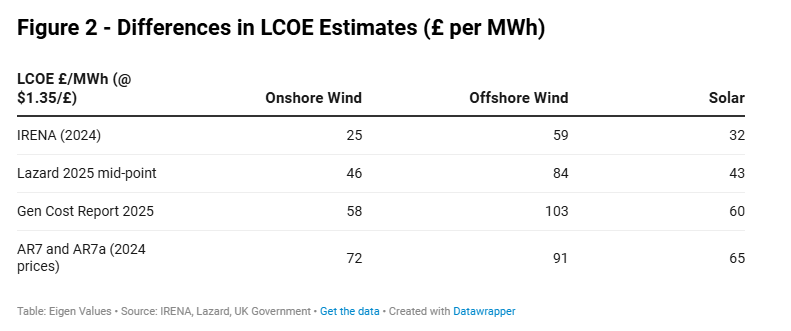

Different organisations produce wildly different LCOE numbers (itself a 🚩). IRENA uses global averages, Lazard focuses on the US, UK Govt on Britain. Geography matters — solar load factor might be 25% in Texas but only ~10% in the UK. (5/19)

IRENA claims onshore wind at just £25/MWh and solar at £32/MWh globally. Reality in UK AR7a auctions? £72/MWh for onshore wind and £65/MWh for solar.

Lazard mid-points are lower than auctions; UK Govt figures closer to reality. Global averages mislead. (6/19)

Lazard mid-points are lower than auctions; UK Govt figures closer to reality. Global averages mislead. (6/19)

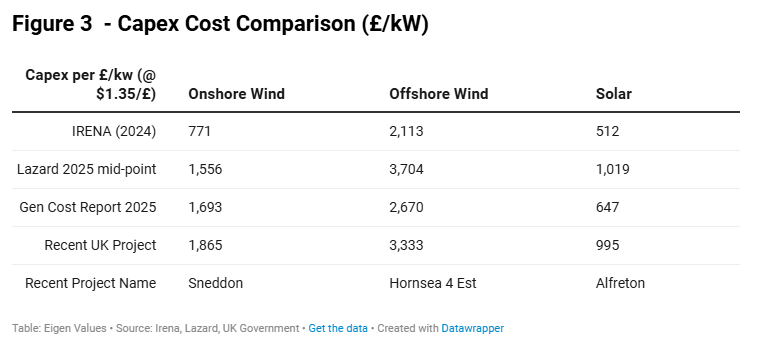

LCOE is extremely sensitive to capital cost (capex) assumptions because most costs are paid upfront. IRENA assumes onshore wind capex at just £771/kW. UK Govt: £1,693/kW. Real project (Sneddon 2024): £1,865/kW. Huge gaps distort results. (7/19)

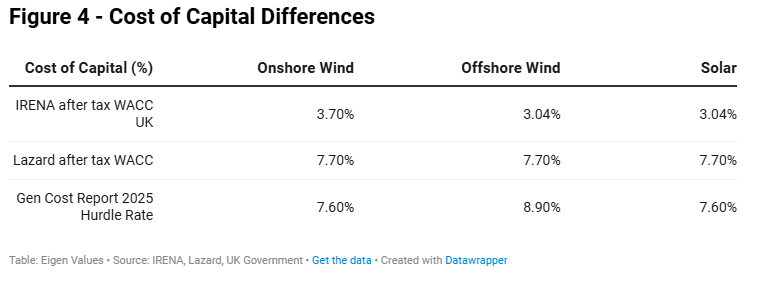

Cost of capital assumptions are another delusion. IRENA uses unrealistically low 3–3.7%. Lazard & UK Govt use 7.6–8.9%. The Govt even applies a higher hurdle rate to gas, artificially inflating its cost. The CCCs 3.5% rate makes offshore wind look 2.5× cheaper than AR7 (8/19)

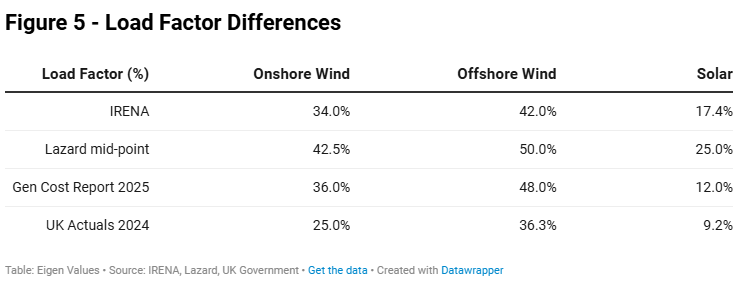

Load factor fantasies: Higher assumed load factors spread costs over more MWh, lowering LCOE. IRENA, Lazard and UK Govt all assume much higher load factors than the actual UK renewables fleet achieved in 2024. Result: systematic under-estimation of costs. (9/19)

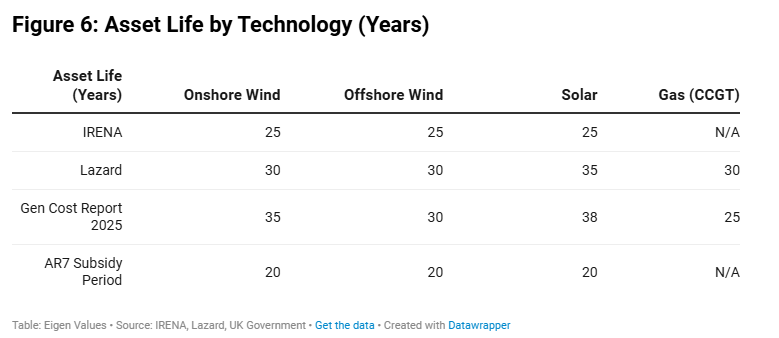

Asset life optimism makes things worse. Govt uses 35yrs for onshore wind, 30 for offshore, 38 for solar. AR7 contracts are 20 years. After that, with lots of renewables, solar & wind often produce when prices are near zero, making them uneconomic without subsidies. (10/19)

Gas plants get the opposite treatment: assumed 25 years, but often run longer as backup. This overstates gas LCOE while understating renewables. (11/19)

Carbon costs tilt the field further. UK Govt adds massive “target-consistent” carbon prices (£44/t rising to £235/t) that make gas look far more expensive. (12/19)

Even when Lazard adds batteries (e.g. 2-hour storage), solar LCOE jumps significantly. But assumptions are still optimistic — charging batteries at artificially low prices and ignoring full replacement & losses. (13/19)

Real-world UK 2024 costs: £1.96bn balancing + £1.25bn capacity market for backup = ~£33/MWh extra just for wind & solar. Plus grid expansion. These system integration costs are usually ignored in standard LCOE. (14/19)

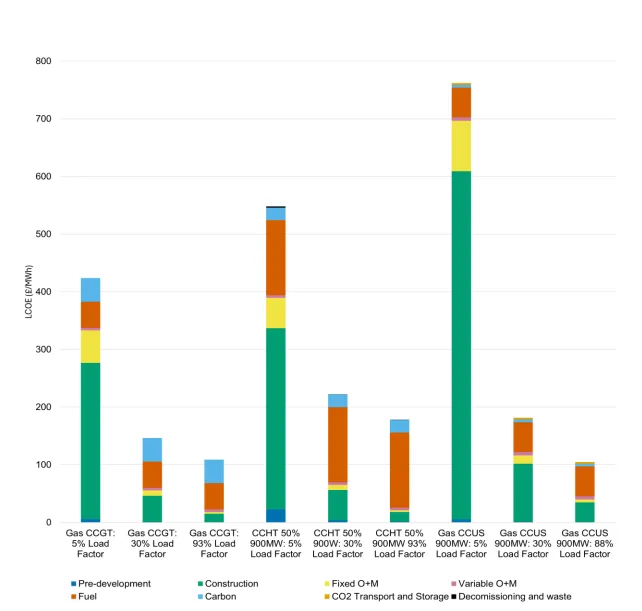

Renewables also force gas plants to run at low load factors (e.g. 30% instead of 93%), dramatically raising their per-MWh cost. The system as a whole gets more expensive. (15/19)

A better approach is Levelised Full System Cost of Energy (LFSCOE). Bank of America analysis showed a 100% wind grid in Germany at ~£373/MWh and 100% solar at ~£1,146/MWh. Even at 95% renewables, costs remain very high. (16/19)

LCOE is classic “garbage in, garbage out.” Optimistic or manipulated inputs (low capex, low discount rates, high load factors, long asset lives) produce conveniently low renewable costs that policymakers love to cite. But they don’t reflect reality. (17/19)

True costs of intermittent renewables only appear when you account for firming, backup, balancing, and system integration. LCOE models are misleading junk science that poison the energy debate. We need honest full-system costing instead.

(18/19)

(18/19)

If you enjoyed this thread, please like and share. You can sign up for free to read the full article on the link below. (19/19)

open.substack.com/pub/davidturve…

open.substack.com/pub/davidturve…

Hi @threadreaderapp unroll please.

• • •

Missing some Tweet in this thread? You can try to

force a refresh