Dear #econtwitter, a few words on my new @nberpubs Working Paper, w/ Junyuan Chen, Marc Muendler, and Fabian Trottner.

Motivation: trade flows and global supply chains adjust slowly. That matters for how we measure the impact of shocks on economic welfare.

Motivation: trade flows and global supply chains adjust slowly. That matters for how we measure the impact of shocks on economic welfare.

https://twitter.com/nberpubs/status/2040504875964866931

Canonical trade models are static. We compare LR steady states. But supply chains are sticky. Contracts, relationships, search, logistics, and sunk costs all slow down adjustment. Empirically, trade elasticities are small in the short run and much larger in the long run.

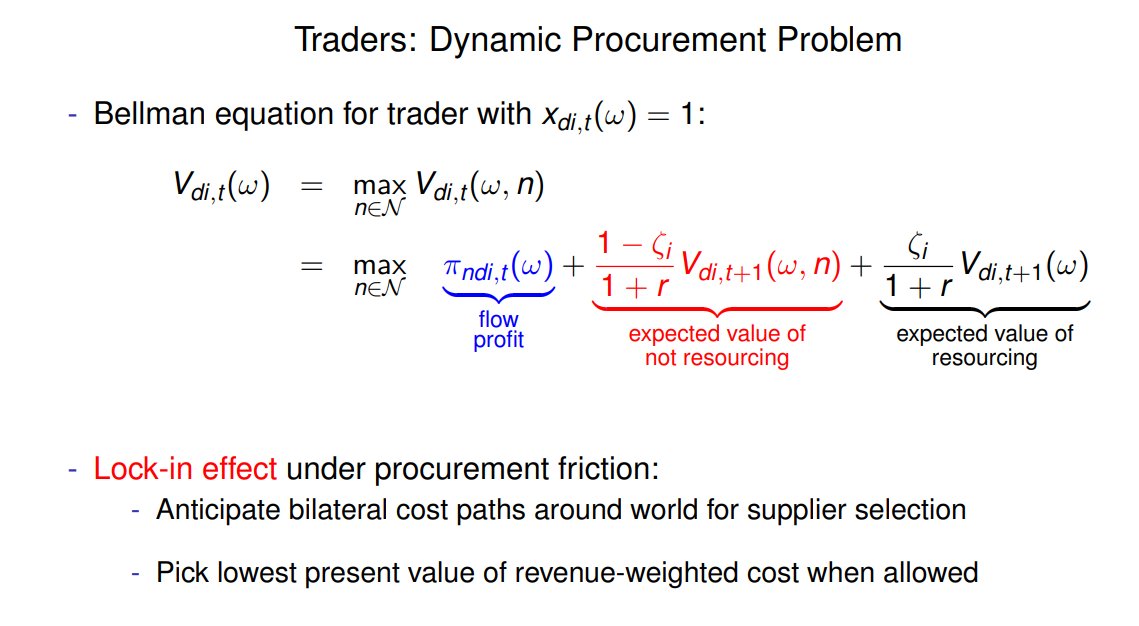

To rationalize this fact, we build a dynamic Ricardian trade model where firms are forward-looking but can switch suppliers only occasionally.

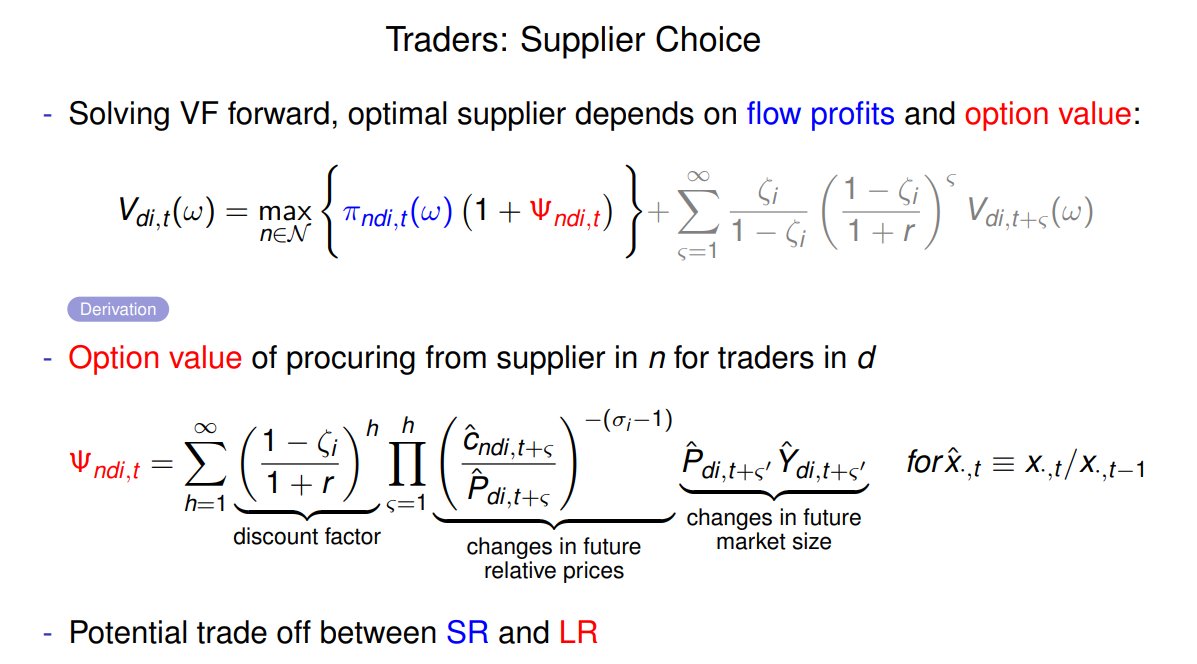

When they can switch, they think about today’s costs and future costs.

That creates gradual adjustment and anticipation.

When they can switch, they think about today’s costs and future costs.

That creates gradual adjustment and anticipation.

The model nests Eaton-Kortum (EK) in the long run.

But along the transition path, trade flows reflect a mix of:

- old supplier relationships

- new sourcing decisions

- expected future trade costs

So one static elasticity is not enough.

But along the transition path, trade flows reflect a mix of:

- old supplier relationships

- new sourcing decisions

- expected future trade costs

So one static elasticity is not enough.

The result, which a commenter called "beautiful" in a conference 🫡, is a horizon-specific trade elasticity that is the weighted average of two canonical elasticities: the SR Armington elasticity (σ-1) on the intensive margin & the LR EK elasticity (θ) on the extensive margin.

We estimate these horizon-specific elasticities. Agriculture, food, and textiles adjust faster. Metals, machinery, and transport equipment more slowly

Supplier relationships are highly persistent. About 93% of procurement relationships carry over from one year to the next.

Supplier relationships are highly persistent. About 93% of procurement relationships carry over from one year to the next.

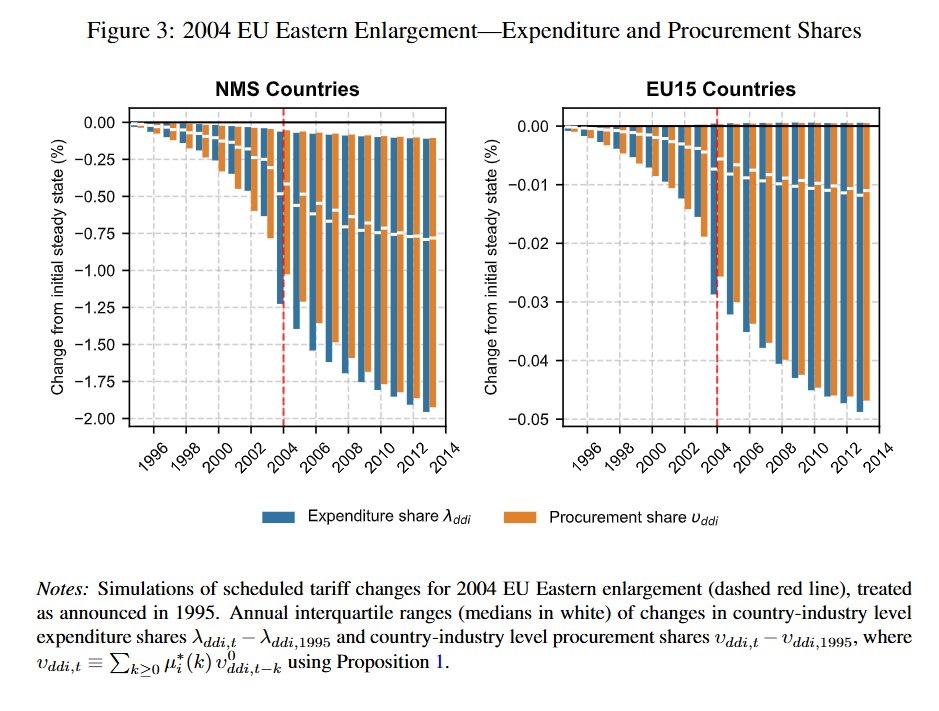

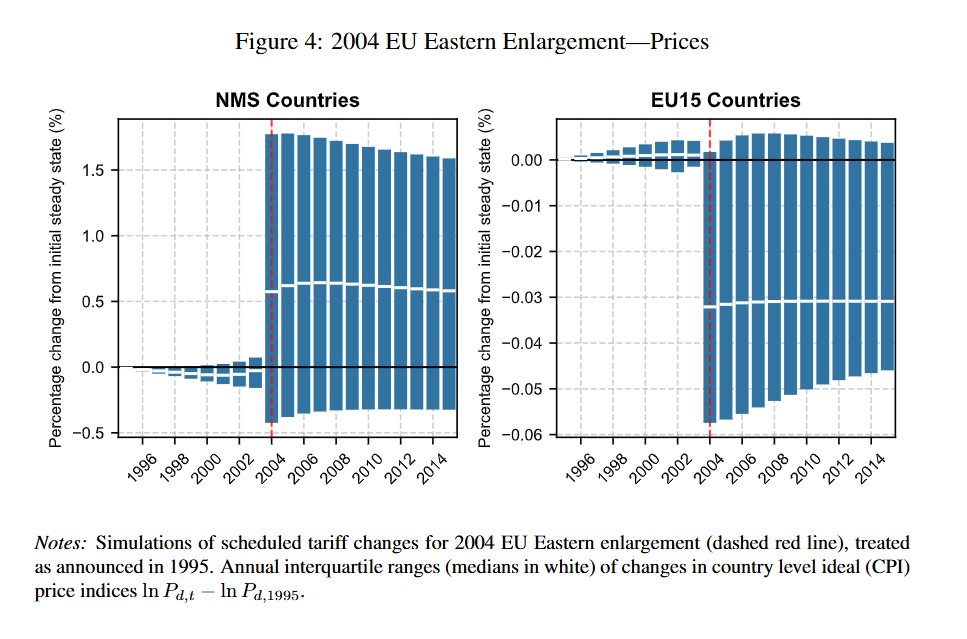

We then quantify the model. First application: the 2004 EU Eastern enlargement. This was announced years in advance, so firms had time to adjust before tariffs actually changed. Before tariffs fall, some firms switch early to suppliers that are not yet cheap. Trade flows and welfare can decouple during the transition.

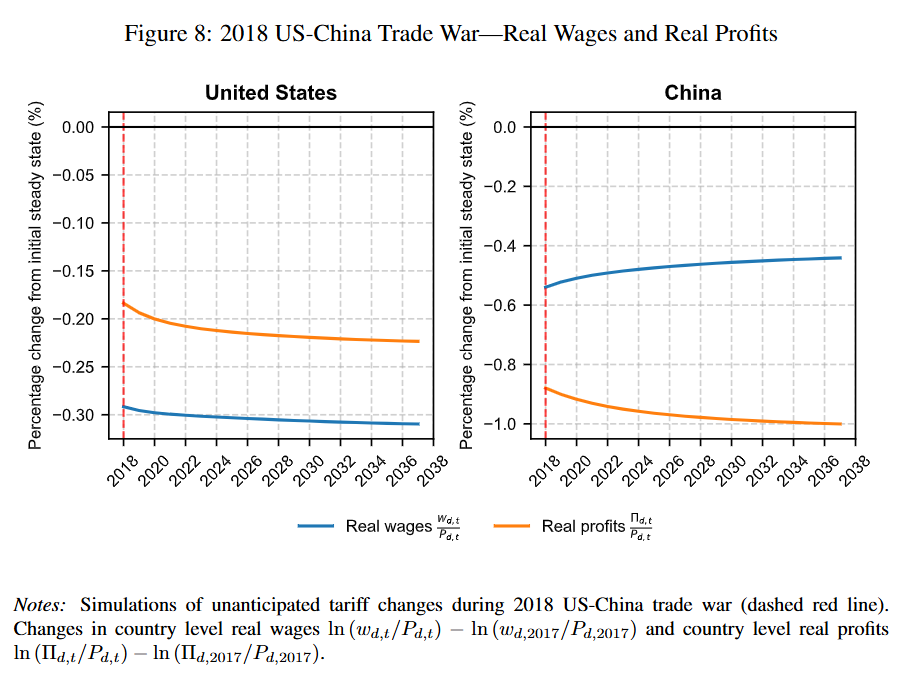

Second application: the 2018 US-China trade war. Unlike EU enlargement, this shock was largely unanticipated. So there is no pre-adjustment. But the transition path takes quite a while. Legacy supply chains erode gradually after tariffs rise.

This is mostly an (applied) theoretical contribution but it has quite important policy-implications as these models are widely used. For policy-relevant horizons, supply-chain frictions and expectations matter. We hope the trade community enjoys and takes advantage if the paper.

@threadreaderapp unroll

• • •

Missing some Tweet in this thread? You can try to

force a refresh