$IREN 2026 Model --> OK this is complex to put in a full thread, as my models runs on an Excel sheet through 2030 (link at the end)

It starts with megawatts.

It starts with megawatts.

$IREN goes from 60 MW deployed today to 500 MW by year-end 2026. Sweetwater: one of the largest AI campuses globally, is getting energized this month.

At $7.4M/MW/year and 57% revenue recognition (capacity ramps through the year):

2026 AI ARR: $3.7B

2026 Recognized revenue: $2.1B

At $7.4M/MW/year and 57% revenue recognition (capacity ramps through the year):

2026 AI ARR: $3.7B

2026 Recognized revenue: $2.1B

EBITDA margins in this business are 80%+. Once a datacenter is built and energized, incremental operating cost is minimal. This isn't SaaS. This is infrastructure.

2026 EBITDA: $1.9B

Plus $200M BTC mining cash (winding down, bridge capital, not the thesis)

2026 EBITDA: $1.9B

Plus $200M BTC mining cash (winding down, bridge capital, not the thesis)

Building 500 MW costs $15.4B in capex. How does $IREN fund it?

→ EBITDA cash: $1.9B

→ MSFT prepayment: $1.2B

→ ATM equity: $2.5B (68M new shares)

→ Net new debt: $9.8B

Yes, that's dilution, shares go from 332M to 400M. Every price target below is fully diluted. No games.

→ EBITDA cash: $1.9B

→ MSFT prepayment: $1.2B

→ ATM equity: $2.5B (68M new shares)

→ Net new debt: $9.8B

Yes, that's dilution, shares go from 332M to 400M. Every price target below is fully diluted. No games.

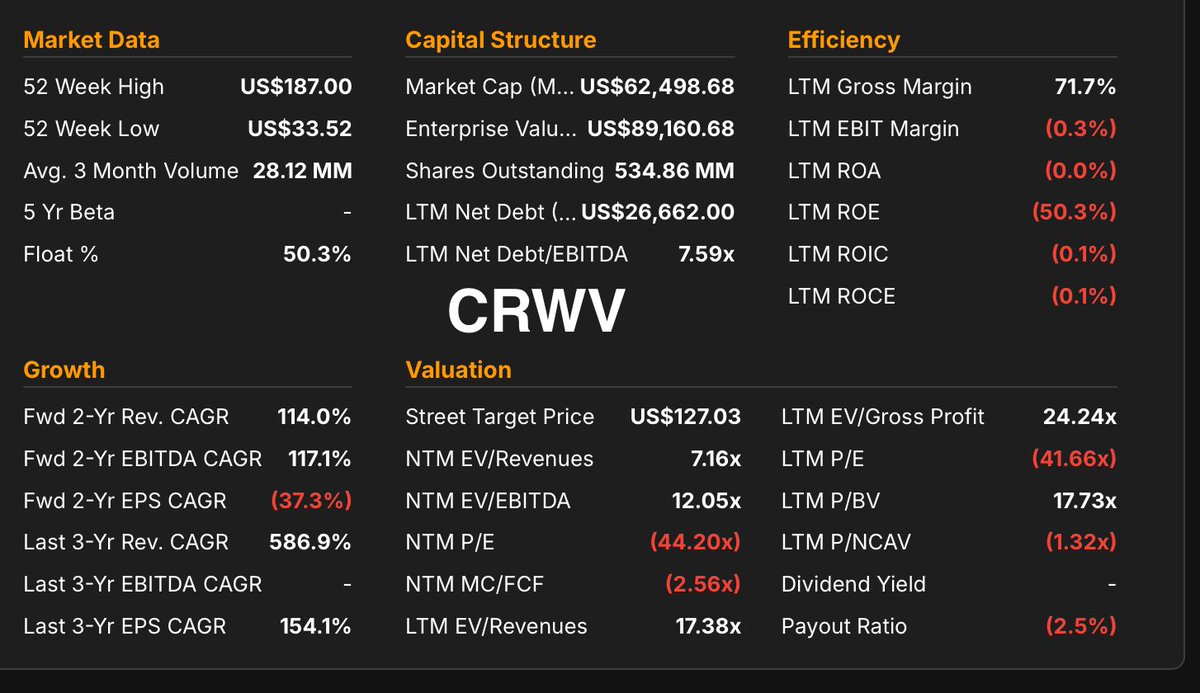

Now the multiple. This is where $CRWV is the reference point.

Right now from TIKR:

CRWV: 12.05x NTM EV/EBITDA on 117% fwd 2-yr EBITDA CAGR

IREN: 13.85x NTM EV/EBITDA on 181% fwd 2-yr EBITDA CAGR

IREN is growing 55% faster but trading at nearly the same multiple.

On my model's numbers (more aggressive than consensus), IREN's 2-yr EBITDA CAGR is higher. Growth-adjusting CRWV's multiple = 31x

I use 33x for 2026 -> the +2x premium is the vertical integration.

Right now from TIKR:

CRWV: 12.05x NTM EV/EBITDA on 117% fwd 2-yr EBITDA CAGR

IREN: 13.85x NTM EV/EBITDA on 181% fwd 2-yr EBITDA CAGR

IREN is growing 55% faster but trading at nearly the same multiple.

On my model's numbers (more aggressive than consensus), IREN's 2-yr EBITDA CAGR is higher. Growth-adjusting CRWV's multiple = 31x

I use 33x for 2026 -> the +2x premium is the vertical integration.

Why does $IREN deserve a multiple premium over $CRWV?

$CRWV rents power. Rents land. Depends on third parties.

$IREN owns 4.5GW+ of secured power. Owns the land. Builds the DCs. Controls the entire stack.

When a hyperscaler deployment needs to be fast and reliable, $IREN controls every variable. That optionality is worth something.

It shows up as slower multiple compression: 33x in 2026, 23.5x in 2027, vs what would be 22x and 16x for $CRWV at equivalent scale.

$CRWV rents power. Rents land. Depends on third parties.

$IREN owns 4.5GW+ of secured power. Owns the land. Builds the DCs. Controls the entire stack.

When a hyperscaler deployment needs to be fast and reliable, $IREN controls every variable. That optionality is worth something.

It shows up as slower multiple compression: 33x in 2026, 23.5x in 2027, vs what would be 22x and 16x for $CRWV at equivalent scale.

2026 base case:

EBITDA: $1.9B × 33x = $62.3B EV

Net debt: $9.8B

Market cap: $52.5B

Fully diluted shares: 400M

Target: $131/share

From $48.12 today, that's 172% upside.

Street target is $72. I'm nearly 2x the Street, because the Street is using consensus EBITDA, not a model built from MW capacity up.

EBITDA: $1.9B × 33x = $62.3B EV

Net debt: $9.8B

Market cap: $52.5B

Fully diluted shares: 400M

Target: $131/share

From $48.12 today, that's 172% upside.

Street target is $72. I'm nearly 2x the Street, because the Street is using consensus EBITDA, not a model built from MW capacity up.

Even my defensible/conservative case at 18x 2026 EBITDA gives you $60/share; 25% upside from here.

And 2026 is just the beginning. By 2027, $IREN is at 850 MW with $4B+ in EBITDA. I'll share that model when we get closer.

At $48, the market is pricing IREN like Sweetwater might not get built. It's getting energized this month.

And 2026 is just the beginning. By 2027, $IREN is at 850 MW with $4B+ in EBITDA. I'll share that model when we get closer.

At $48, the market is pricing IREN like Sweetwater might not get built. It's getting energized this month.

Full excel link here:

ps: I do one of these for each of my holdings…iles-prod.s3.eu-north-1.amazonaws.com/company-fundam…

ps: I do one of these for each of my holdings…iles-prod.s3.eu-north-1.amazonaws.com/company-fundam…

• • •

Missing some Tweet in this thread? You can try to

force a refresh