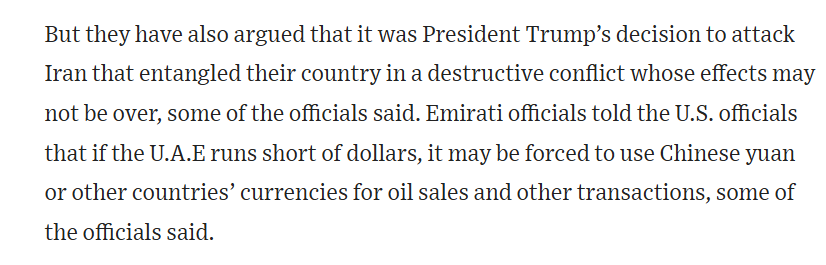

Interesting WSJ story about the Emirates request for a swap line --

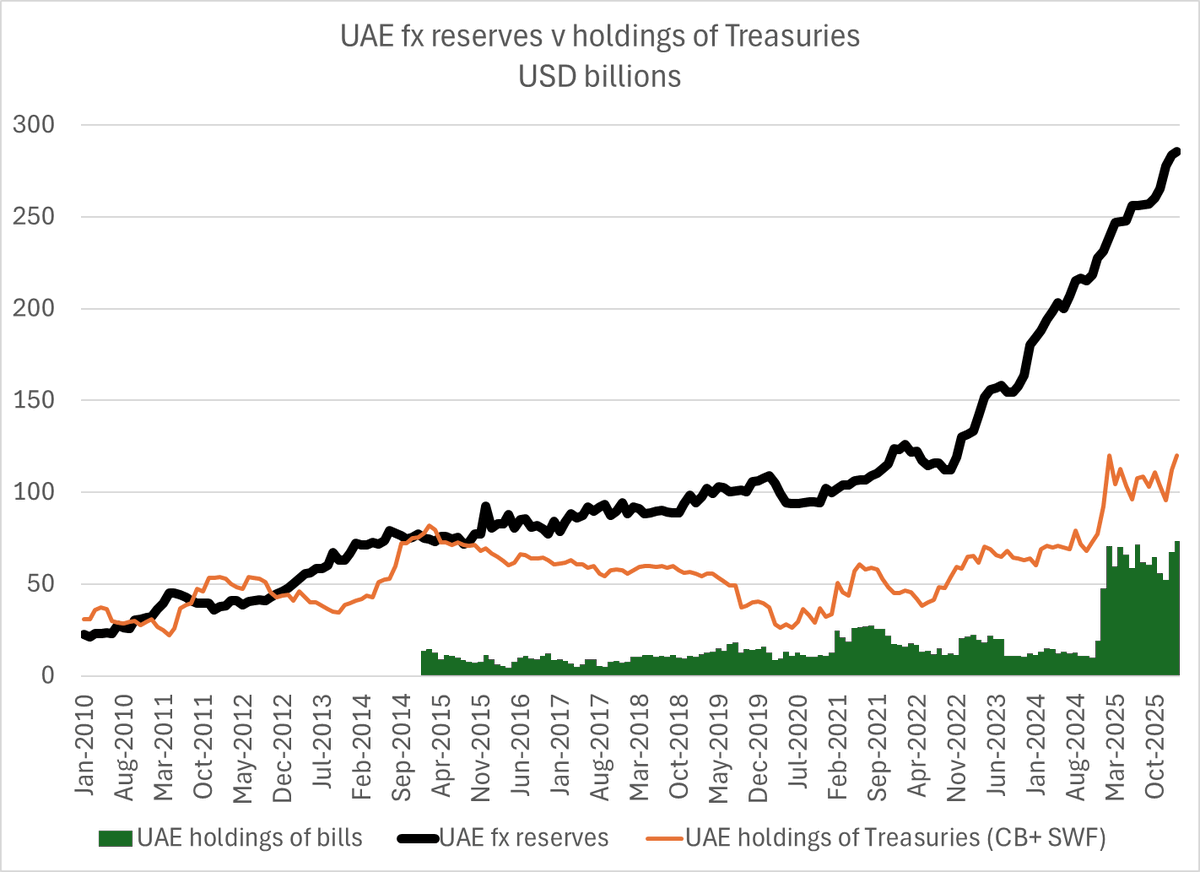

the UAE hasn't reported its end March reserves but it went into the conflict with tons of reserves and no shortage of liquid bills in US custodians

1/

the UAE hasn't reported its end March reserves but it went into the conflict with tons of reserves and no shortage of liquid bills in US custodians

1/

Given the central bank's ample apparent liquidity, the immense assets of Abu Dhabi's sovereign funds and the UAE/ Abu Dhabi's clear ability to borrow dollars, I am not sure there is a realistic prospect that the UAE will ever run short of dollars

2/

2/

But the fact that they have asked is interesting -- and they clearly think the threat of using yuan is a way to get the attention of the United States (my sense is that the Trump Administration is a bit too concerned about this ... )

3/

wsj.com/world/middle-e…

3/

wsj.com/world/middle-e…

I rather doubt that the Fed would give the Emirates a swap line -- they are keen to limit the use of Fed swaps to G-10 countries with long-standing ties to the Fed ... and clearly don't want to fund geopolitical risks or a shortfall in oil revenues

4/

4/

And the Treasury's exchange stabilization fund has fewer resources than the UAE's central bank (at the end of February) and certainly fewer resources than the central bank, ADIA and the other sovereign funds ...

But the UAE might still want the symbolic vote of confidence

5/

But the UAE might still want the symbolic vote of confidence

5/

to my mind though there is a significant substantive issue with any swap line with the UAE -- namely the UAE's horrible balance of payments data and long history of limited transparency about its finances/ the size of its sovereign funds ...

6/

6/

And there isn't anything obviously "America first" about a financial lifeline to one of the richest oil sheikdoms (if not the richest) just so it doesn't have to borrow in the market/ sell assets ...

7/

7/

But very interesting that this request was both made and that it made its way into the WSJ ...

Clear that parts of the UAE aren't happy about being asked to absorb the full financial costs of Trump's bombing campaign

8/8

wsj.com/world/middle-e…

Clear that parts of the UAE aren't happy about being asked to absorb the full financial costs of Trump's bombing campaign

8/8

wsj.com/world/middle-e…

• • •

Missing some Tweet in this thread? You can try to

force a refresh