The Guardian is reporting Angela Rayner has now paid £40,000 of extra stamp duty, but HMRC accepted she wasn't "careless" and so she didn't pay a penalty.

On the public facts, that’s hard to understand.

Here’s why:

On the public facts, that’s hard to understand.

Here’s why:

The background, in short:

1. Ms Rayner sold her remaining interest in her Ashton-under-Lyne family home to a trust set up for her disabled son, and bought a flat in Hove.

2. She paid stamp duty at the standard rate of around £30,000.

1. Ms Rayner sold her remaining interest in her Ashton-under-Lyne family home to a trust set up for her disabled son, and bought a flat in Hove.

2. She paid stamp duty at the standard rate of around £30,000.

3. Stamp duty is 5% higher if you are buying a second home; Ms Rayner didn't pay that higher rate.

4. Her conveyancer and a trusts lawyer had both told her standard rate applied – but both had explicitly said this was not specialist tax advice. One "suggested" she obtain specialist tax advice; the other "recommended" it. However Ms Rayner did not obtain tax advice.

5. After the story broke in the press, Ms Rayner instructed a tax KC, who advised that the higher rate for additional dwellings did in fact apply, because a "deeming rule" meant that Ms Rayner was deemed to herself own the house that the trust held for her son.

6. Ms Rayner therefore had to pay an additional £40,000 (and, we expect, about £3,000 of interest).

Our team doesn't understand the "not careless" finding. We've spoken to other senior lawyers, including a retired judge, and we're a bit mystified.

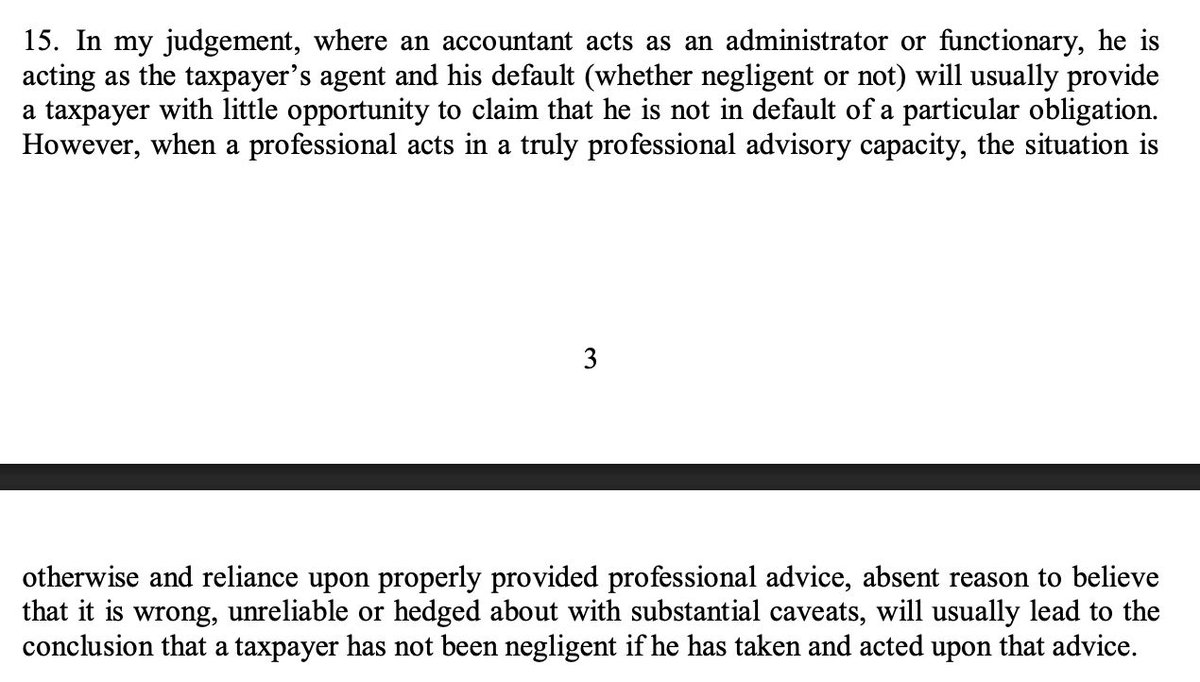

The legal test is whether Ms Rayner failed to take the care a "prudent and reasonable person in her position" would have taken. The leading caselaw is clear that you can rely on professional advice – but not where it is "hedged about with substantial caveats".

It is hard to see how a taxpayer, undertaking a complex transaction involving a court-ordered trust for a disabled child and the purchase of a second property, and twice told to obtain specialist tax advice, can be said to have taken reasonable care by not doing so.

That conclusion is even harder where the taxpayer was Deputy Prime Minister and Secretary of State for Housing.

There are three possibilities:

(a) Our view of the law is wrong, and on the facts set out above, Ms Rayner was not "careless". That of course is possible, but we remain confident of our position.

(a) Our view of the law is wrong, and on the facts set out above, Ms Rayner was not "careless". That of course is possible, but we remain confident of our position.

(b) HMRC have misapplied the law. That would be surprising - particularly in a high profile case. We don't expect HMRC would be influenced by Ms Rayner's position - they were, after all, able to independently investigate a sitting Chancellor of the Exchequer.

(c) There are facts of which we are unaware which mean that Ms Rayner was not careless. Perhaps the caveats were not as blunt as Sir Laurie's summary suggests. Perhaps there were other circumstances which made it reasonable for Ms Rayner not to obtain specialist tax advice..

So I have to say at present I don't know why HMRC accepted Ms Rayner was not "careless". On the facts as they have been publicly stated, that conclusion seems generous.

None of this is to suggest any impropriety on Ms Rayner's part. There is no evidence she tried to avoid or evade tax – this was (in our view, and on the facts as we know them) a careless mistake.

The higher-rates-for-additional-dwellings regime is a mess in numerous respects, and this is far from the only time we've seen it produce results which appear unfair.

Ms Rayner's mistake looks like exactly the kind of thing that happens when people with complicated personal arrangements don't obtain specialist tax advice.

But the "careless" test in Schedule 24 is not about morality, or the fairness of a policy. It asks a narrow question: did the taxpayer take the care that a reasonable person would take?

On the publicly stated facts, the answer to that question still looks to us like "no".

On the publicly stated facts, the answer to that question still looks to us like "no".

HMRC's contrary conclusion will be welcomed by Ms Rayner, but it raises a question of consistency: ordinary taxpayers who ignore explicit advice to consult a specialist routinely receive careless penalties.

It is not obvious why this case is different.

It is not obvious why this case is different.

Our full analysis here, including our view of the legal "ambiguity" and potential appeal grounds mentioned in the Guardian article. We don't agree there would have been a realistic prospect of appeal: taxpolicy.org.uk/2026/05/14/why…

And the Guardian's article here: theguardian.com/politics/2026/…

Happy to discuss any aspect of this, and if anyone identifies any error in our analysis I'll correct asap.

But I fear lots of people will whine I'm biased in favour of or against Ms Rayner. I'm just going to block whiners straight away.

But I fear lots of people will whine I'm biased in favour of or against Ms Rayner. I'm just going to block whiners straight away.

• • •

Missing some Tweet in this thread? You can try to

force a refresh