$1,000 per month invested in a custodial account can create a $65,000 annual income stream by the time your kid is 18.

Here’s how. 🧵👇

Here’s how. 🧵👇

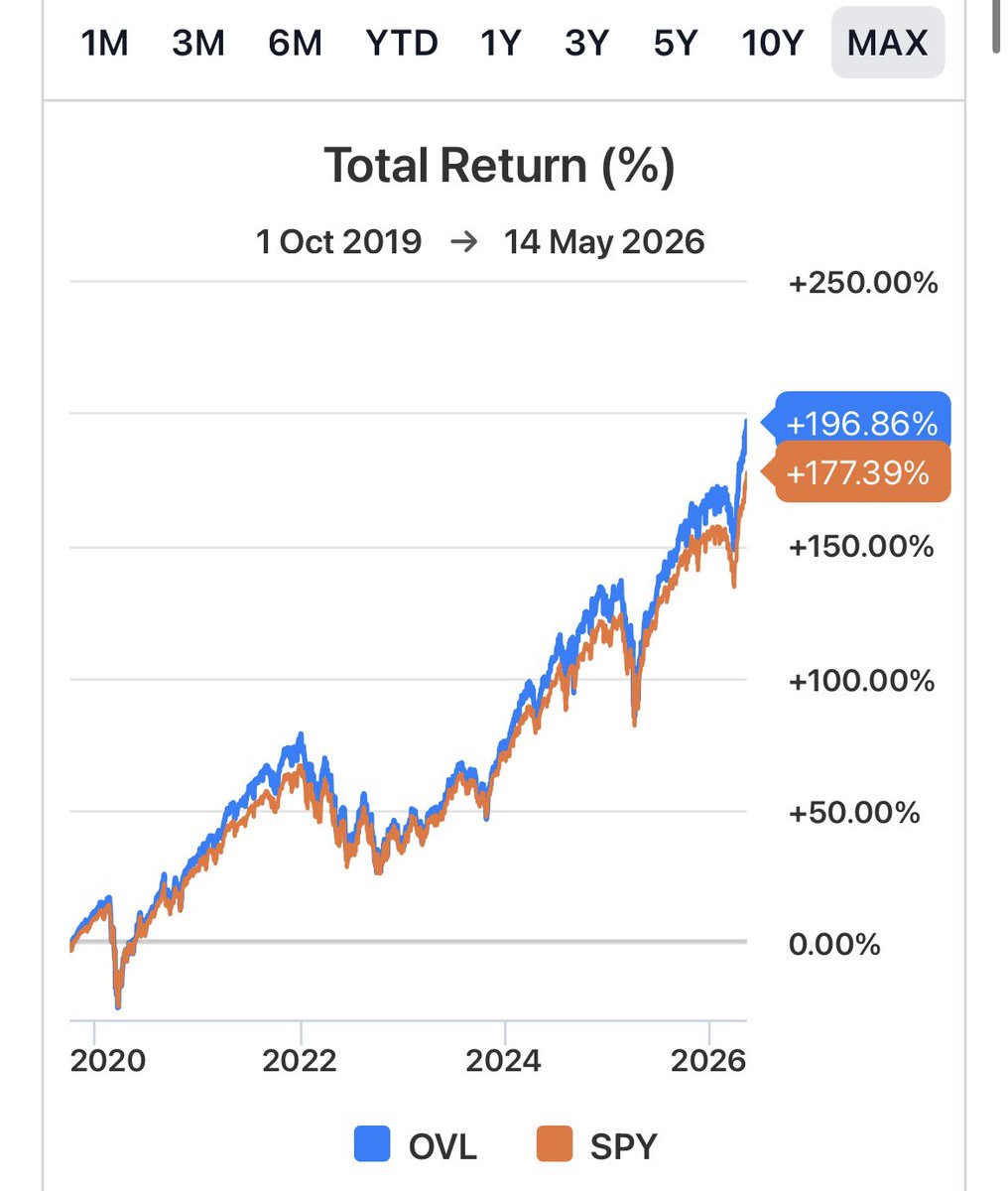

$OVL holds 99% $VOO and uses the rest as collateral to cover a ladder of put credit spreads.

Those spreads allow for 10.5% yield and uncapped upside. The fund has even beat the S&P 500 for nearly 7 years. It’s the true best of both worlds fund.

Those spreads allow for 10.5% yield and uncapped upside. The fund has even beat the S&P 500 for nearly 7 years. It’s the true best of both worlds fund.

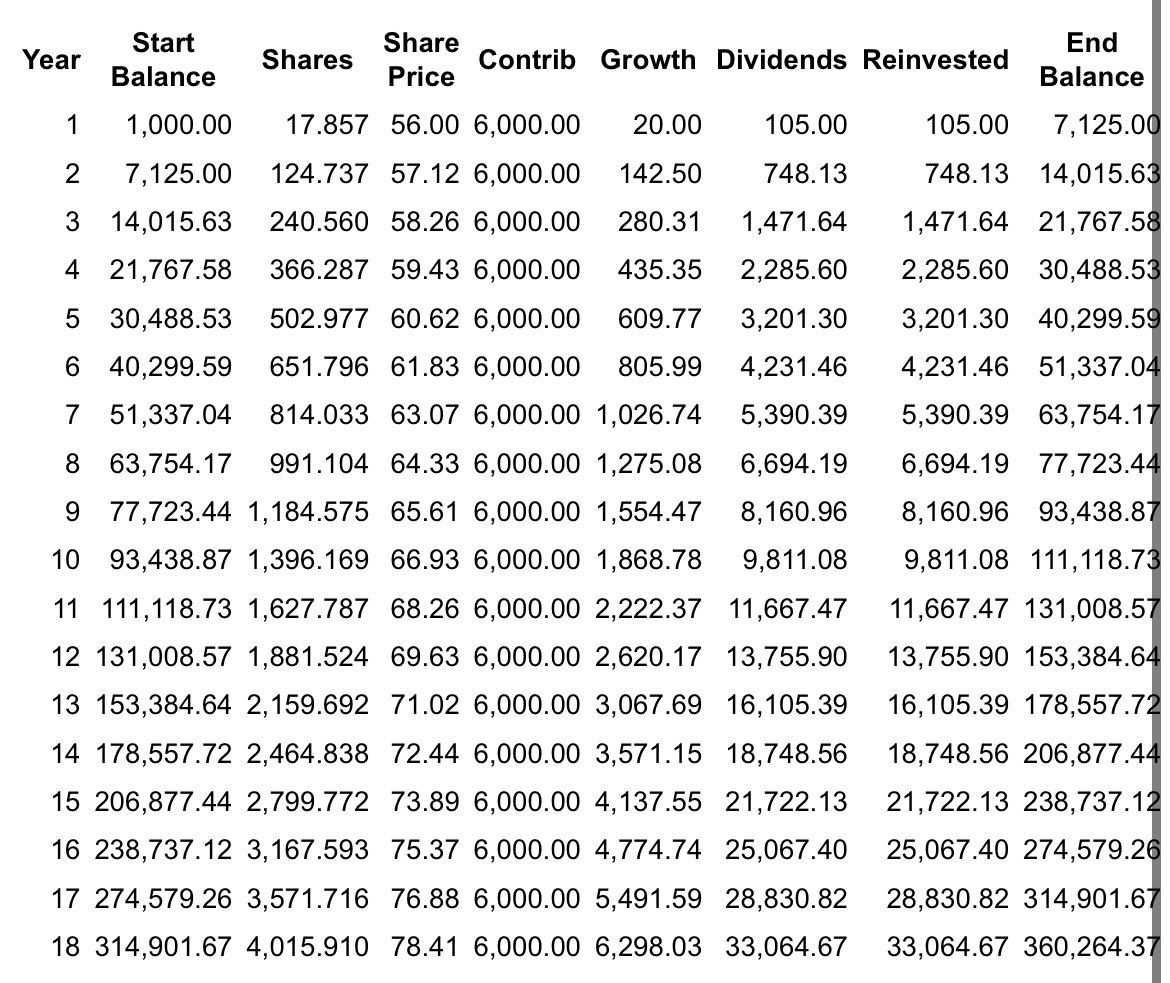

Let’s use some conservative metrics.

1️⃣ $1,000 per month contributed

2️⃣ Drip turned on

3️⃣ 2% annual nav growth

4️⃣ 10.5% yield

Here’s the results 👇

1️⃣ $1,000 per month contributed

2️⃣ Drip turned on

3️⃣ 2% annual nav growth

4️⃣ 10.5% yield

Here’s the results 👇

By year 18 the balance grows from $1,000 ➡️ $622,000

The income stream grows to $65,000.

The income stream grows to $65,000.

There’s no thinking behind this instead only patience, consistency, and a high quality fund.

Is $1,000 per month too much? Even $500 grows into $315,000 & $33,000 per year in cashflow.

Most kids start their adult life with no assets and student loan debt. Don’t let yours be most.

Come play high yield the right way in 2026!

I break down every high yield fund I buy.

Every entry. Every exit. Every target. Every move.

If you want:

📊 Fund breakdowns

🎯 Real time buys & sells

📝 Entry/exit levels

🏆 Only the best high yield plays

⏰ Set & Forget Funds

👋 Hands on strategy

Tap the link below to play high yield the right way 👇+ 0DTE • Option Selling • Leaps • Swing Trading = All Included. t.co/r1dHINwADl

I break down every high yield fund I buy.

Every entry. Every exit. Every target. Every move.

If you want:

📊 Fund breakdowns

🎯 Real time buys & sells

📝 Entry/exit levels

🏆 Only the best high yield plays

⏰ Set & Forget Funds

👋 Hands on strategy

Tap the link below to play high yield the right way 👇+ 0DTE • Option Selling • Leaps • Swing Trading = All Included. t.co/r1dHINwADl

• • •

Missing some Tweet in this thread? You can try to

force a refresh