Handelsblatt has -- on its front page -- an article summarizing my new paper with Sander Tordoir on Germany's need to find policies to actually fight back against the second China shock

handelsblatt.com/politik/deutsc…

1/ x.com/CER_EU/status/…

handelsblatt.com/politik/deutsc…

1/ x.com/CER_EU/status/…

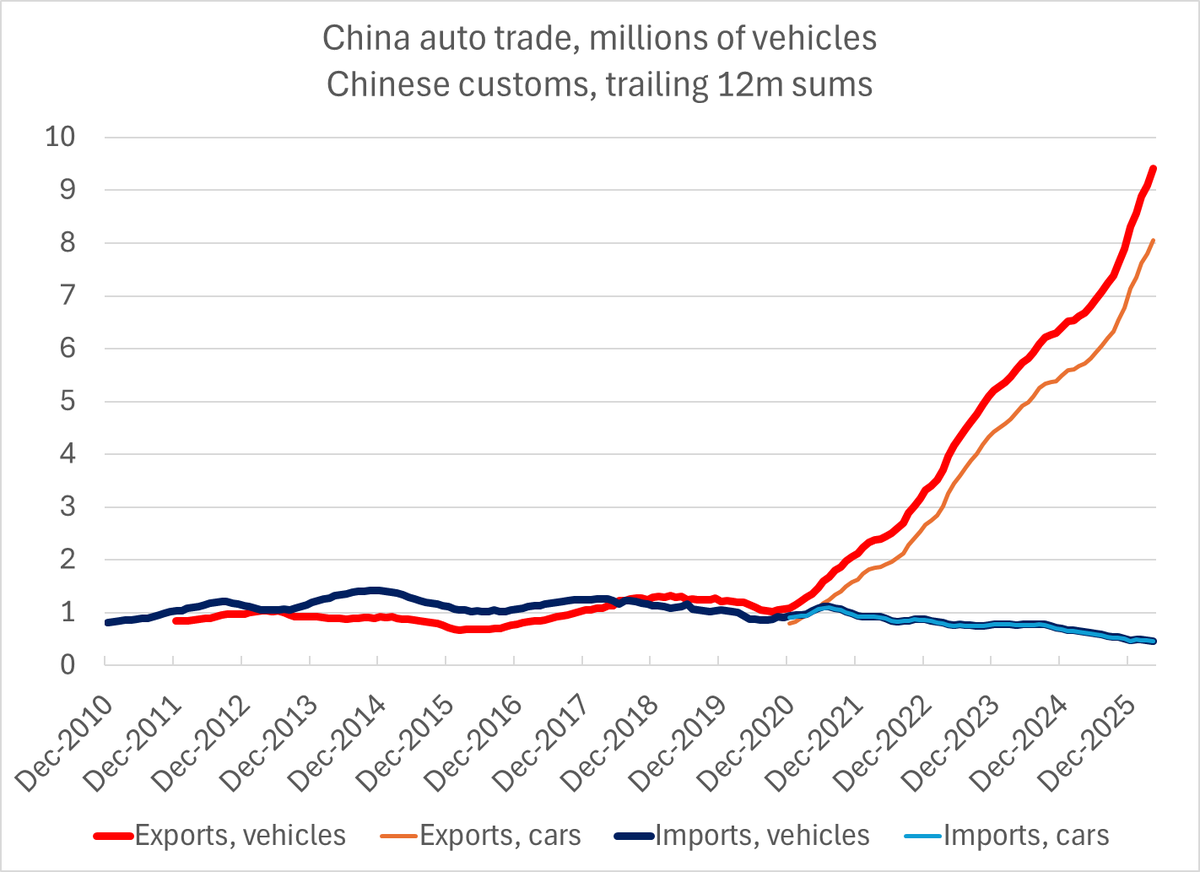

China's industrial structure -- as the ECB and others have noted -- increasingly overlaps with that of Germany ... with autos being the most obvious case.

And the China shock there won't go away on its own; Chinese auto export growth accelerated in the last 12ms

2/

And the China shock there won't go away on its own; Chinese auto export growth accelerated in the last 12ms

2/

The China shock is also visible in the global data -- an undervalued Chinese currency propelled Chinese exports to grow much faster than global trade. China is now big, so that meant someone else's exports had to grow more slowly than global trade ...

3/

3/

There is a new exportweltmeister -- and it as been eating Germany's lunch.

It should be much more widely known that net exports have been a massive drag on German growth in the years after the pandemic

4/

It should be much more widely known that net exports have been a massive drag on German growth in the years after the pandemic

4/

Sander and I don't just admire the problem -- we have a series of recommendations for German and European policy.

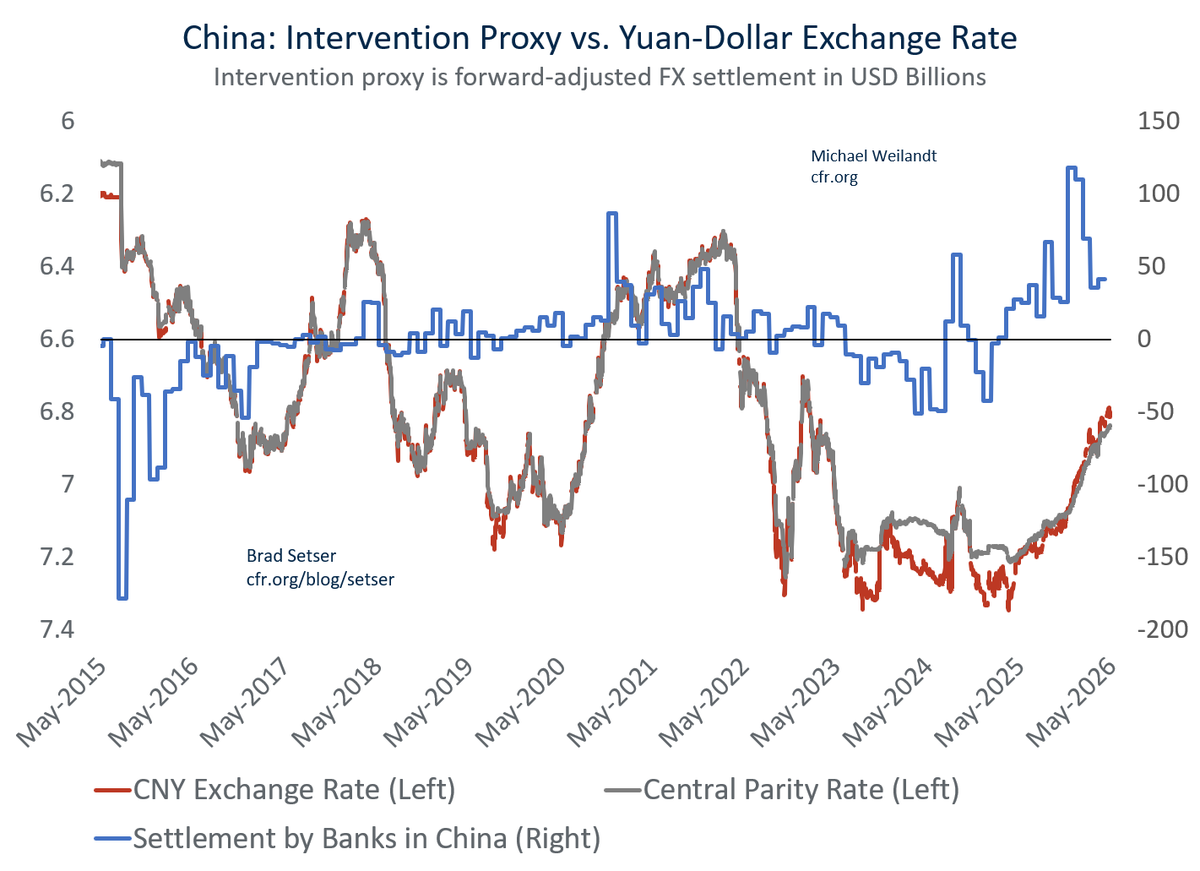

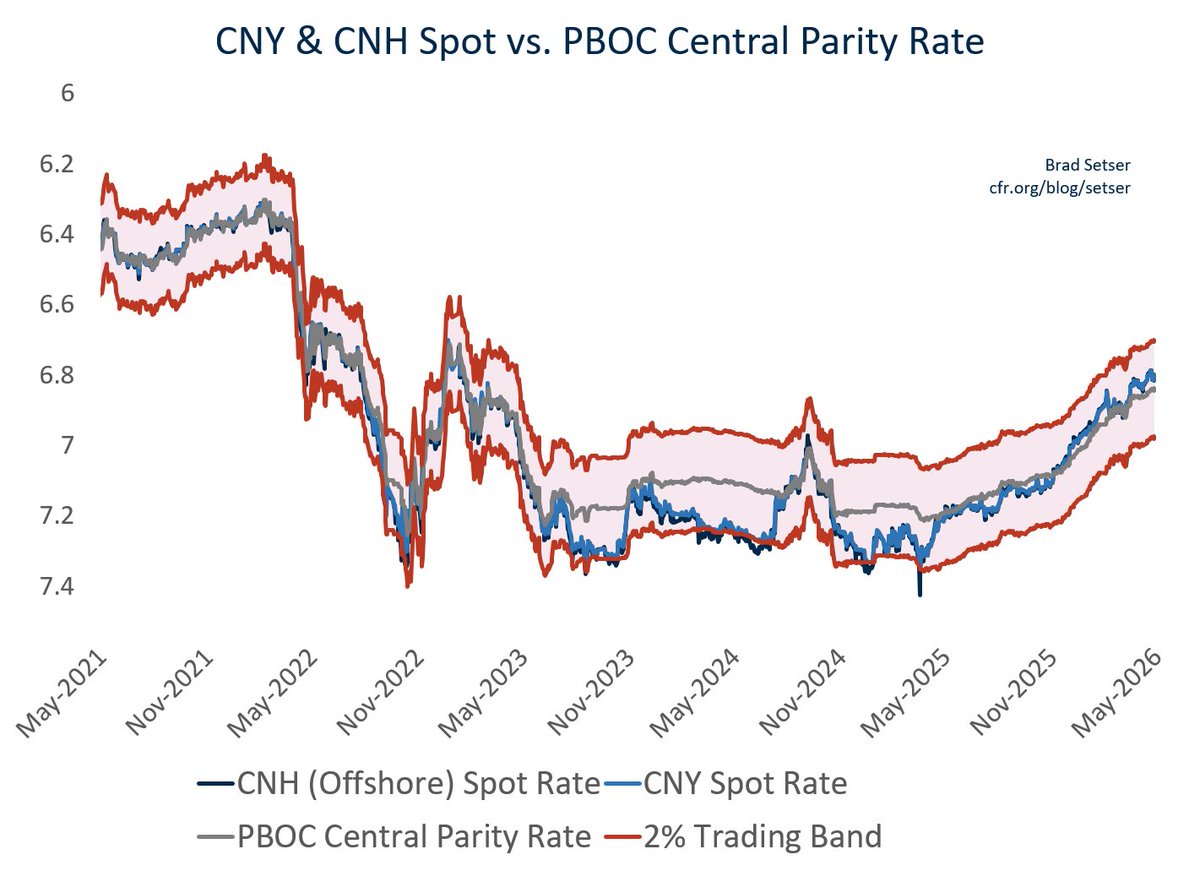

Among other things, we call for a European "301" and suggest using it against Chinese currency policies that suppress the yuan ...

5/

Among other things, we call for a European "301" and suggest using it against Chinese currency policies that suppress the yuan ...

5/

Take a look -- it is a paper meant to shake up the debate in Berlin, and ultimately in Brussels

6/6

cer.eu/publications/a…

6/6

cer.eu/publications/a…

• • •

Missing some Tweet in this thread? You can try to

force a refresh