Germany is the epicentre of the China Shock 2.0 reverberating in global markets

In a new paper, @Brad_Setser and I show the shock is a key driver of Germany’s economic malaise. And it's accelerating

Berlin needs to stop admiring the problem, and join efforts to fight back

1/

In a new paper, @Brad_Setser and I show the shock is a key driver of Germany’s economic malaise. And it's accelerating

Berlin needs to stop admiring the problem, and join efforts to fight back

1/

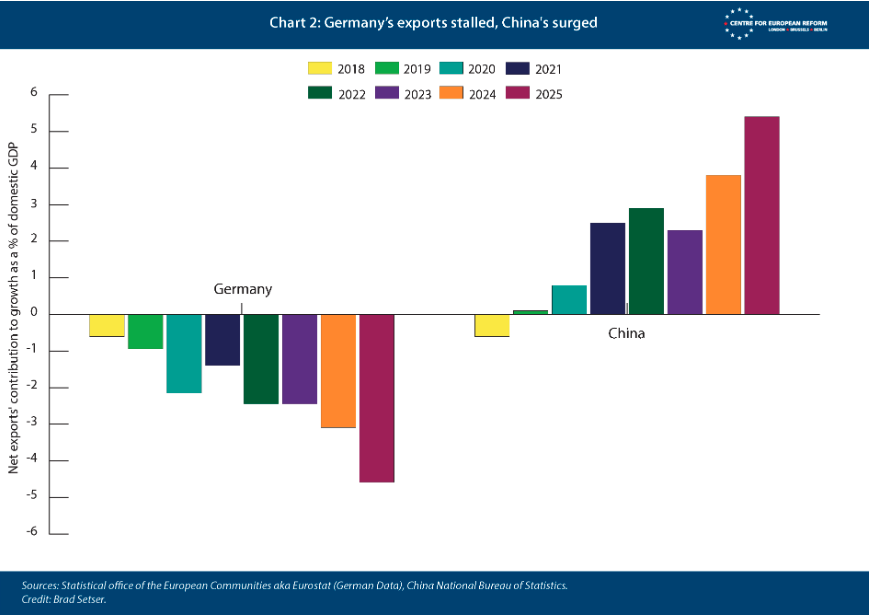

China’s exploding exports are squeezing German firms in cars, machinery, chemicals and aerospace in China, third markets and increasingly Europe itself.

The drag from falling net exports has accelerated sharply since 2023, amounting to roughly 3% of German GDP.

2/

The drag from falling net exports has accelerated sharply since 2023, amounting to roughly 3% of German GDP.

2/

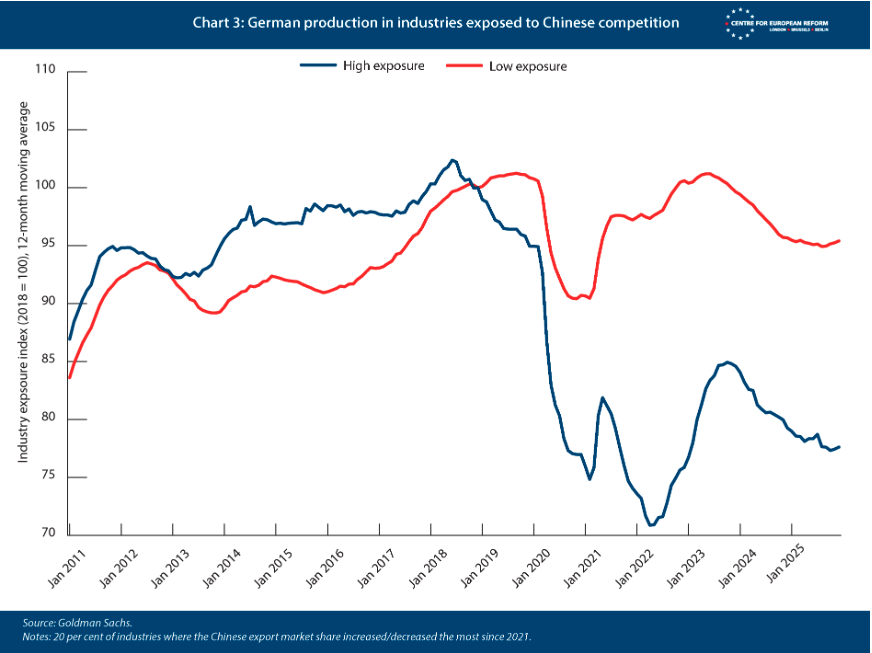

The damage has fed through to industrial production, with sectors most exposed to Chinese competition shrinking fastest.

Germany isn't alone. Every major EU economy except the Netherlands (buoyed by chipmaking giant ASML) has seen exports to China fall

Bureaucracy anyone?

3/

Germany isn't alone. Every major EU economy except the Netherlands (buoyed by chipmaking giant ASML) has seen exports to China fall

Bureaucracy anyone?

3/

The shock is worsening for Europe's most car-centric economy.

Analysts had estimated China would only export 10 million cars a year by the end of the decade. But China’s 2025 Q4 exports, annualised, already hit that mark.

And the automotive sector is not unique.

4/

Analysts had estimated China would only export 10 million cars a year by the end of the decade. But China’s 2025 Q4 exports, annualised, already hit that mark.

And the automotive sector is not unique.

4/

In 2025, China’s export volumes grew at more than twice the pace of global trade — and accelerated further in 2026.

The result is a more than $1 trillion rise in Chinese exports without a balancing rise in imports, yielding a manufacturing surplus on par with Italy’s GDP.

5/

The result is a more than $1 trillion rise in Chinese exports without a balancing rise in imports, yielding a manufacturing surplus on par with Italy’s GDP.

5/

Beyond Das Auto, similar dynamics are unfolding across sectors long seen as the backbone of the German economy — machinery, chemicals, clean tech and aircraft.

Germany now buys more capital goods from China than China buys from Germany — a striking tipping point.

6/

Germany now buys more capital goods from China than China buys from Germany — a striking tipping point.

6/

Berlin can no longer afford to wait for the problem to correct itself.

The drivers of China’s surplus persist, including a weak domestic demand dragged down by the property bust, cheap state-backed credit for manufacturing, and an undervalued currency.

7/

The drivers of China’s surplus persist, including a weak domestic demand dragged down by the property bust, cheap state-backed credit for manufacturing, and an undervalued currency.

7/

Textbook adjustment just isn't materialising.

China is intervening to stymie currency appreciation, while its vast domestic savings mean it could plausibly sustain an external surplus of 10% of GDP, with no hard limit on the foreign financial claims it can accumulate.

8/

China is intervening to stymie currency appreciation, while its vast domestic savings mean it could plausibly sustain an external surplus of 10% of GDP, with no hard limit on the foreign financial claims it can accumulate.

8/

The latest batch of Chinese data shows domestic demand weakening further.

And China’s new five-year plan doubles down on manufacturing expansion, import substitution, and technological self-reliance.

It all augurs even more export-led growth ahead.

9/

And China’s new five-year plan doubles down on manufacturing expansion, import substitution, and technological self-reliance.

It all augurs even more export-led growth ahead.

9/

The risk for Germany, which already struggled to adjust when China’s surplus (correctly measured) jumped from 2 to 5 per cent of GDP, is acute.

Much of the demand generated by Germany’s fiscal expansion could leak into Chinese imports and throttle Germany’s recovery.

10/

Much of the demand generated by Germany’s fiscal expansion could leak into Chinese imports and throttle Germany’s recovery.

10/

Global car, machinery and chemicals production could concentrate further in China, eroding innovation in traditional manufacturing centres.

And increasing Beijing's ability to coerce Berlin by throttling supply the way it did for rare earths and Nexperia chips.

11/

And increasing Beijing's ability to coerce Berlin by throttling supply the way it did for rare earths and Nexperia chips.

11/

The EU has launched a patchwork of product-specific trade defences and a piecemeal buy-EU industrial policy.

But China’s trade surplus with the EU is still growing at around 30%, showing these efforts are too slow and too narrow.

The EU is holding a knife in a gunfight.

12/

But China’s trade surplus with the EU is still growing at around 30%, showing these efforts are too slow and too narrow.

The EU is holding a knife in a gunfight.

12/

In a world where China relies heavily on net exports to sustain growth (1.5–2% of GDP a year), and Europe remains the largest open advanced market, Berlin and Brussels still have strong cards to play.

We lay out several options.

13/

We lay out several options.

13/

This includes deploying trade safeguards more broadly, and developing an EU 301 style instrument to respond to China’s currency undervaluation - tariffs the EU can take off if China adjusts.

The EU should, of course, exempt its roster of 76 FTA partners from these measures

14/

The EU should, of course, exempt its roster of 76 FTA partners from these measures

14/

Many of them are equally worried about China.

But Brussels and Berlin should not let Chinese content enter unchecked through FTA partners, and should push partners to adopt similar rules.

Europe needs to play industrial/trade policy Tinder — insisting on reciprocity.

15/

But Brussels and Berlin should not let Chinese content enter unchecked through FTA partners, and should push partners to adopt similar rules.

Europe needs to play industrial/trade policy Tinder — insisting on reciprocity.

15/

Retaliation from Beijing is likely, including possibly restrictions on minerals and industrial inputs.

Europe therefore needs a credible deterrence strategy, including investment in alternative supply chains and the ability to respond in kind to economic coercion.

16/

Europe therefore needs a credible deterrence strategy, including investment in alternative supply chains and the ability to respond in kind to economic coercion.

16/

Germany now has a unique window to build a coalition of EU and global allies to respond to China.

France has valiantly tried the diplomatic route with China via its G7 presidency.

And the Commission will debate the China shock on May 29, followed by EU leaders in June.

17/

France has valiantly tried the diplomatic route with China via its G7 presidency.

And the Commission will debate the China shock on May 29, followed by EU leaders in June.

17/

Berlin needs to decide whether it wants to allow China to dismantle core parts of its manufacturing ecosystem in an era of rearmament.

Time is running out: Europe's leverage will decline as China captures ever more chokepoints.

The paper is here:

18/18

cer.eu/publications/a…

Time is running out: Europe's leverage will decline as China captures ever more chokepoints.

The paper is here:

18/18

cer.eu/publications/a…

• • •

Missing some Tweet in this thread? You can try to

force a refresh