Excited to FINALLY release toughest+most rewarding paper I've worked on...

….we attack a 150 year old Walras question that's gone unanswered, not for lack of trying (Hicks, Samuelson, Arrow; our chances?😱)...

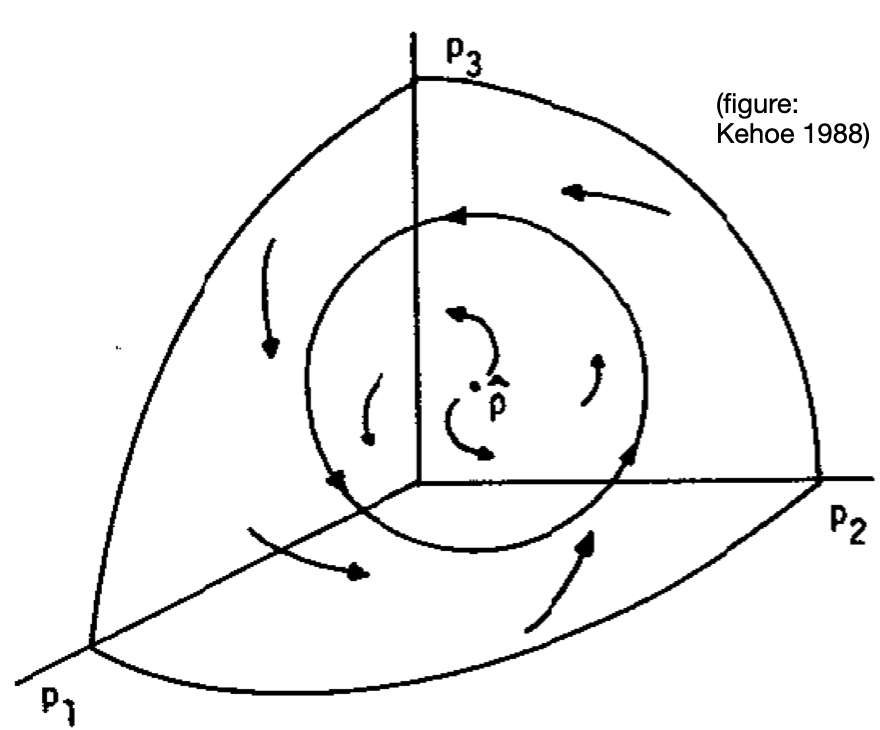

Q: Is the market equilibrium stable or unstable?¯\_(ツ)_/¯

🧵

….we attack a 150 year old Walras question that's gone unanswered, not for lack of trying (Hicks, Samuelson, Arrow; our chances?😱)...

Q: Is the market equilibrium stable or unstable?¯\_(ツ)_/¯

🧵

Not an abstract question… General Equilibrium (GE) is applied in trade, growth, public finance, macro, IO, development...

Question is not if equilibrium exist: that was settled triumphantly by Arrow, Debreu, McKenzie, but...

What good is it if we don't get there?

Question is not if equilibrium exist: that was settled triumphantly by Arrow, Debreu, McKenzie, but...

What good is it if we don't get there?

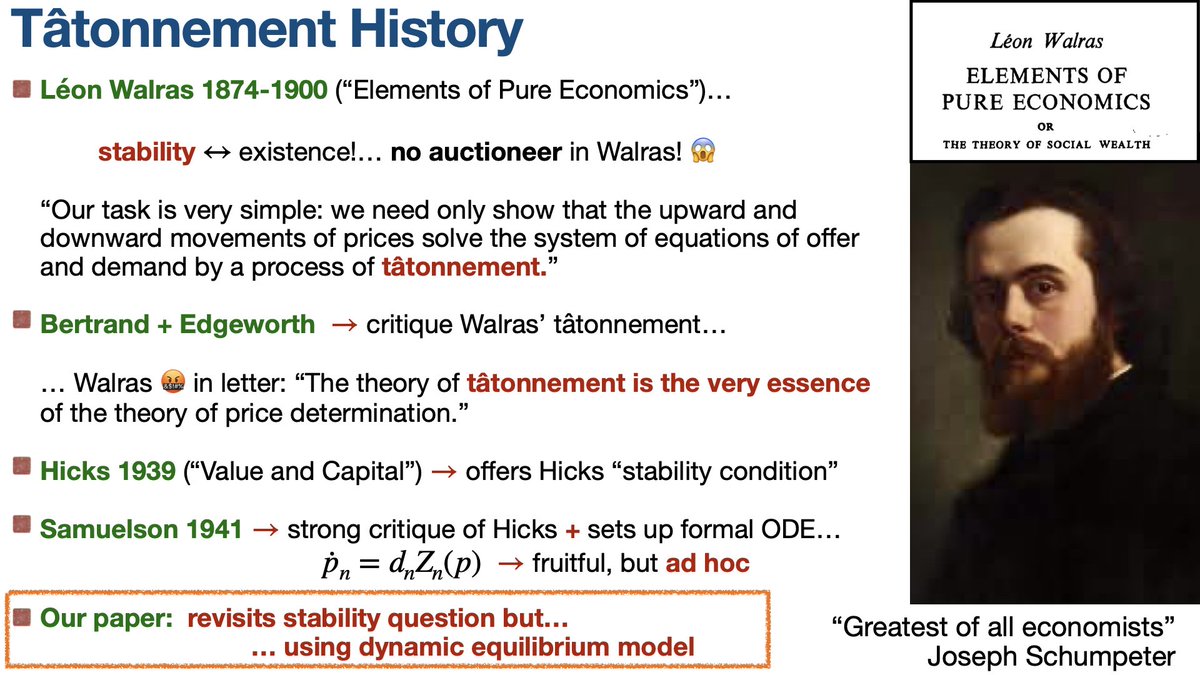

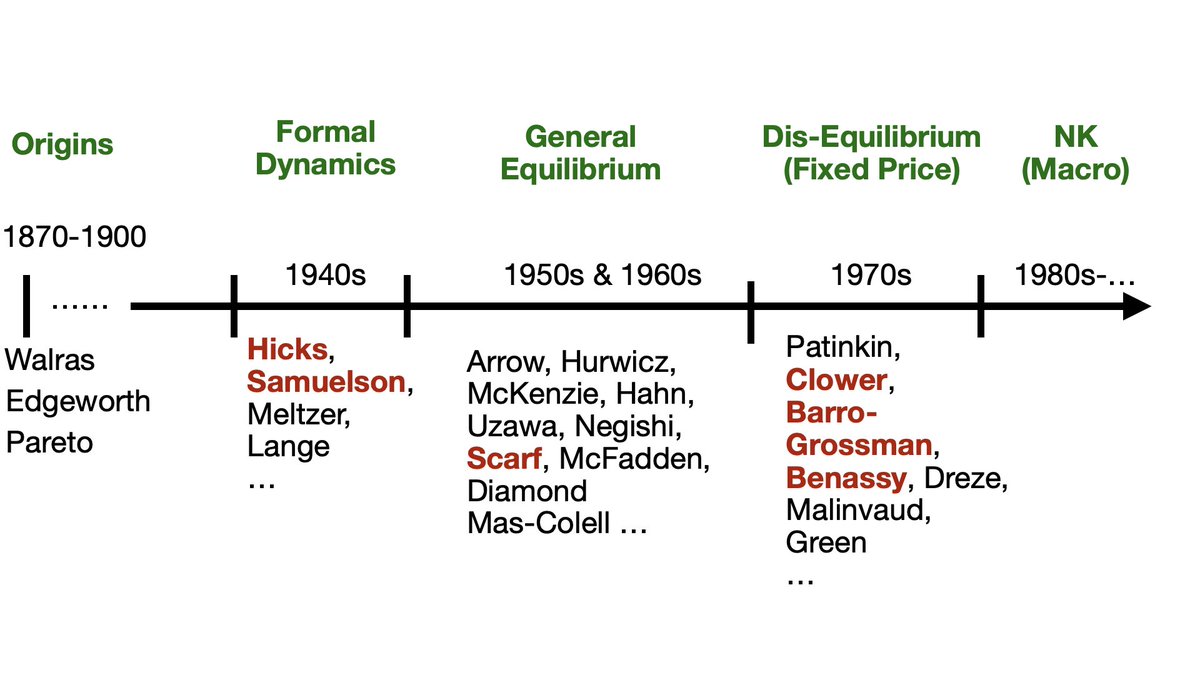

A bit of fun history...

Leon Walras was so ahead: he pushed economics to GE with many markets 16 years before Marshall wrote his great partial equilibrium book...

Myth busting: Walras did not push a centralized auctioneer, he had in mind actual decentralized markets...

Leon Walras was so ahead: he pushed economics to GE with many markets 16 years before Marshall wrote his great partial equilibrium book...

Myth busting: Walras did not push a centralized auctioneer, he had in mind actual decentralized markets...

He spent decades revising his magnum opus, defending what he called tâtonnement where

… prices "feel their way" toward equilibrium

... nudged by excess demand

(Tâtonnement from French/Latin root tactare, to touch or feel)

… prices "feel their way" toward equilibrium

... nudged by excess demand

(Tâtonnement from French/Latin root tactare, to touch or feel)

Walras thought equilibria existed and were stable. Always. By modern standards he had no proof...

Next up: Hicks vs Samuelson…🥊

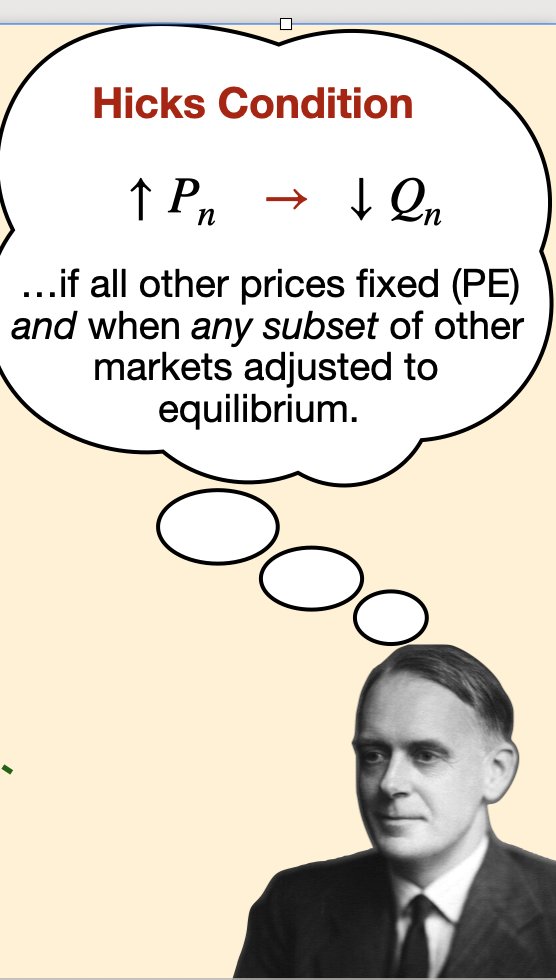

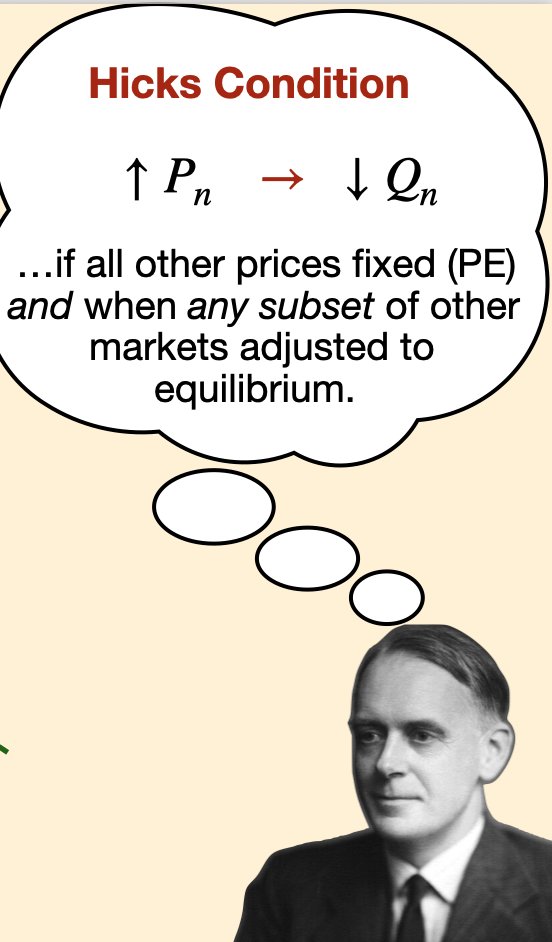

Hicks took up stability in his magnum opus. A big step to recognize stability is NOT so easy, not a foregone conclusion.

He proposed a condition.

Next up: Hicks vs Samuelson…🥊

Hicks took up stability in his magnum opus. A big step to recognize stability is NOT so easy, not a foregone conclusion.

He proposed a condition.

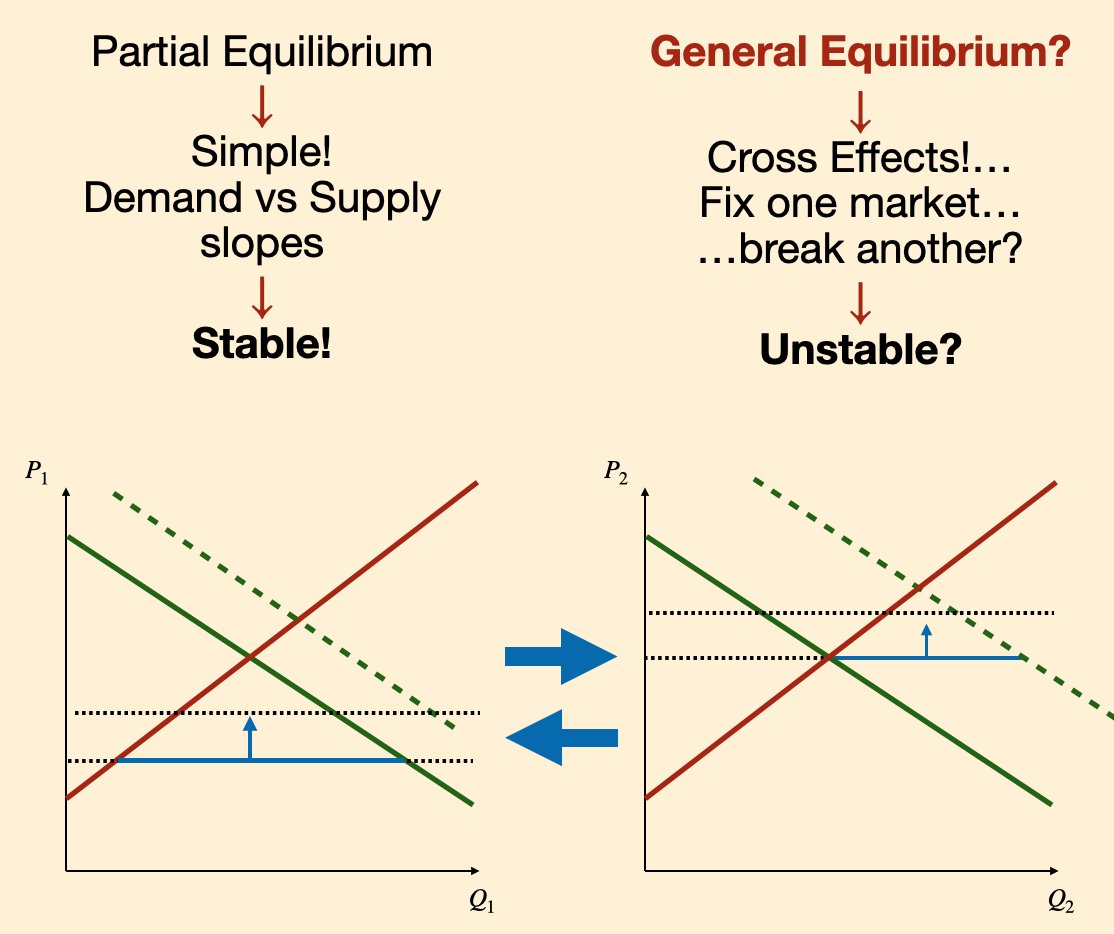

But wait, first: why is stability so hard. Just make demands slope down and supply up!… In a single market sure. But with more markets...

… as you fix one market… you may screw up the other… "whack a mole"!

So Hicks thought of this and came up with...

… as you fix one market… you may screw up the other… "whack a mole"!

So Hicks thought of this and came up with...

Hicks condition (1939): impose that excess demand slopes down after any subset of other markets clear.

Smart.

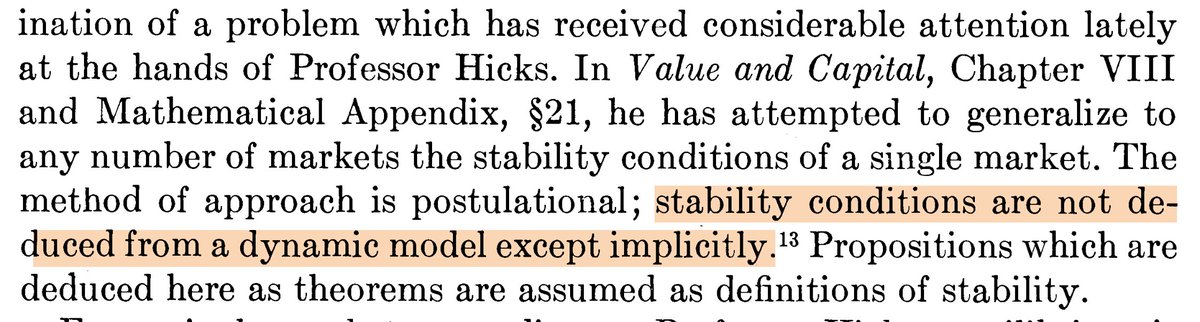

… but Samuelson came immediately (1941) to critique Hicks: "He has no explicit dynamics. He made that condition up. Here are some actual dynamics! Let's see…"

Smart.

… but Samuelson came immediately (1941) to critique Hicks: "He has no explicit dynamics. He made that condition up. Here are some actual dynamics! Let's see…"

…a formal but ad hoc version of Tâtonnement was born…

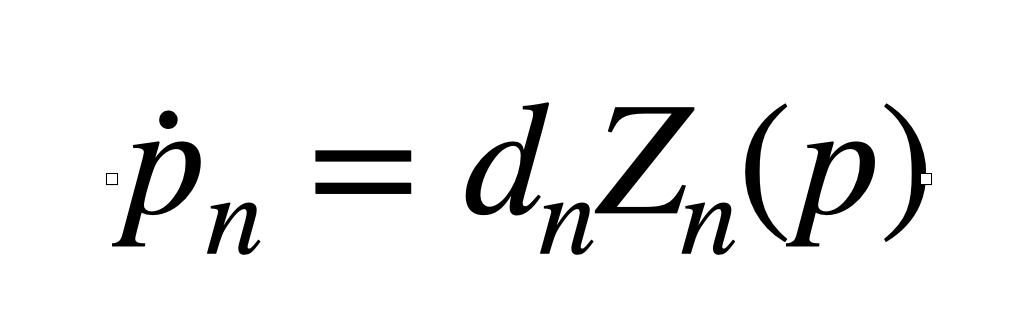

Samuelson put down a differential equation that says:

"prices in market n go up (dot p>0) if there is excess demand Zn(p)>0 in that market at some speed dn"

Samuelson put down a differential equation that says:

"prices in market n go up (dot p>0) if there is excess demand Zn(p)>0 in that market at some speed dn"

Then he studied that equation and said that Hicks is just plain wrong. Quoting below from his paper. Later repeated in his magnum opus Foundations.

Devastating. (Hicks in his 2nd edition partially conceded.)

Devastating. (Hicks in his 2nd edition partially conceded.)

Fun side note: Samuelson is known for the "Correspondence Principle" linking comparative statics with Dynamics. You may think he pushed a tight link.

No! He was warning "only in 1-dimension, very tricky otherwise!"

My view: it was mostly a critique of Hicks after reading V&C.

No! He was warning "only in 1-dimension, very tricky otherwise!"

My view: it was mostly a critique of Hicks after reading V&C.

Samuelson's equation was picked up by the top GE people. Metzler, McFadden defended Hicks...

… but later work in 50s and 60s by Arrow-Hurwicz, Hahn, McKenzie, Negishi, Uzawa and many other top GE theorists mostly did not use Hicks.

They found… STABILITY! But how?...

… but later work in 50s and 60s by Arrow-Hurwicz, Hahn, McKenzie, Negishi, Uzawa and many other top GE theorists mostly did not use Hicks.

They found… STABILITY! But how?...

Idea 💡

They imposed (as Arrow-Debreu had) that demands Z(p) aren't "anything", they are derived from optimal choices of firms and households: this had some bite.

But it didn't last...

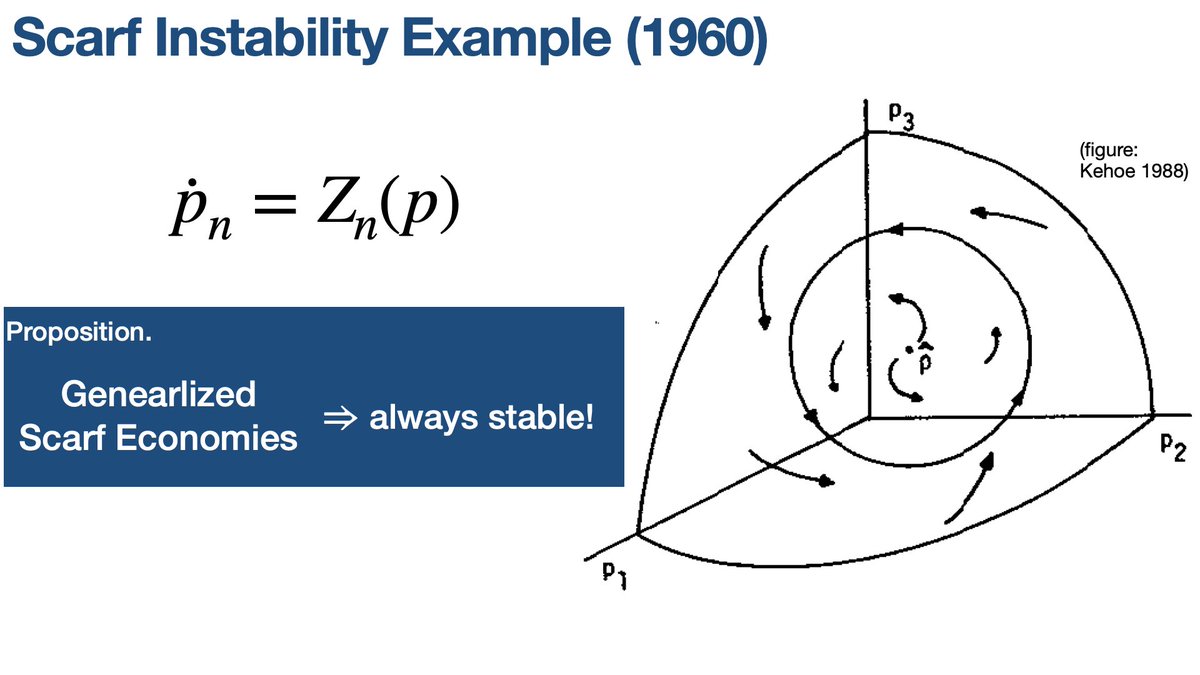

A bright 29yo Scarf announced a counterexample taking down the hopes of these greats.

They imposed (as Arrow-Debreu had) that demands Z(p) aren't "anything", they are derived from optimal choices of firms and households: this had some bite.

But it didn't last...

A bright 29yo Scarf announced a counterexample taking down the hopes of these greats.

Scarf was a decade ahead of his time, putting his toes in the "Anything Goes" "Sonnenschein-Mantel-Debreu" results obtained in the 70s.

Bummer: Due to income effects aggregate demands are not restricted.

(We dedicated our paper to genius Rolf Mantel. My undergraduate teacher.)

Bummer: Due to income effects aggregate demands are not restricted.

(We dedicated our paper to genius Rolf Mantel. My undergraduate teacher.)

So Samuelson's tâtonnement can be unstable.

Did that lead to tâtonnement's demise?

No. Economists also wished uniqueness, but lived with multiplicity.

What really killed tâtonnement was its ad hoc origin and concrete concerns it was just wrong...

Did that lead to tâtonnement's demise?

No. Economists also wished uniqueness, but lived with multiplicity.

What really killed tâtonnement was its ad hoc origin and concrete concerns it was just wrong...

Frank Fisher at MIT laid it out in a nice book much later.

Basically tâtonnement is a "static model with dynamics pasted on".

Concern 1: who sets prices? Arrow "in GE, nobody!😱"

Would price setters set prices use excess demand? ¯\_(ツ)_/¯

Concern 2: even if they did...

Basically tâtonnement is a "static model with dynamics pasted on".

Concern 1: who sets prices? Arrow "in GE, nobody!😱"

Would price setters set prices use excess demand? ¯\_(ツ)_/¯

Concern 2: even if they did...

Concern 2: if prices are not at equilibrium

—> not everyone can get what they want...

—> if you can't satisfy demand for one good

—>affects your demands for other goods…

Oh no: Walrasian demands don't capture this, they assume you satisfy all demand.

—> not everyone can get what they want...

—> if you can't satisfy demand for one good

—>affects your demands for other goods…

Oh no: Walrasian demands don't capture this, they assume you satisfy all demand.

Concern 3: Dynamics matter for behavior.

Consumers —>may wait if price temporarily high or buy more on bargain; don't always spend all income, can smooth.

Price setters: price will be set for a bit, expectations of future matter. Not myopic!

Consumers —>may wait if price temporarily high or buy more on bargain; don't always spend all income, can smooth.

Price setters: price will be set for a bit, expectations of future matter. Not myopic!

Two literatures emerged to deal with different subsets of these issues...

1. Disequilibrium 70s:

Takes on concern 2 in GE: effective demand with spillovers (very insightful)

But not 1+3 (i.e. static "fixed price" equilibria!)

Also: intractable problems. Bad reputation (not fair)

1. Disequilibrium 70s:

Takes on concern 2 in GE: effective demand with spillovers (very insightful)

But not 1+3 (i.e. static "fixed price" equilibria!)

Also: intractable problems. Bad reputation (not fair)

New Keynesian 80s-today: (Secret weapon: monopolistic competition!) Huge success: solves price setting many ways + lots more

… but abandons general GE for macro settings

… sure, multiple markets yes, but not Generality of GE

Neither address Walras' Stability Question.

… but abandons general GE for macro settings

… sure, multiple markets yes, but not Generality of GE

Neither address Walras' Stability Question.

What do we do...

Take best of both literatures+tâtonnement spirit...

—> new excess-demand approach

—> pricing with excess demands

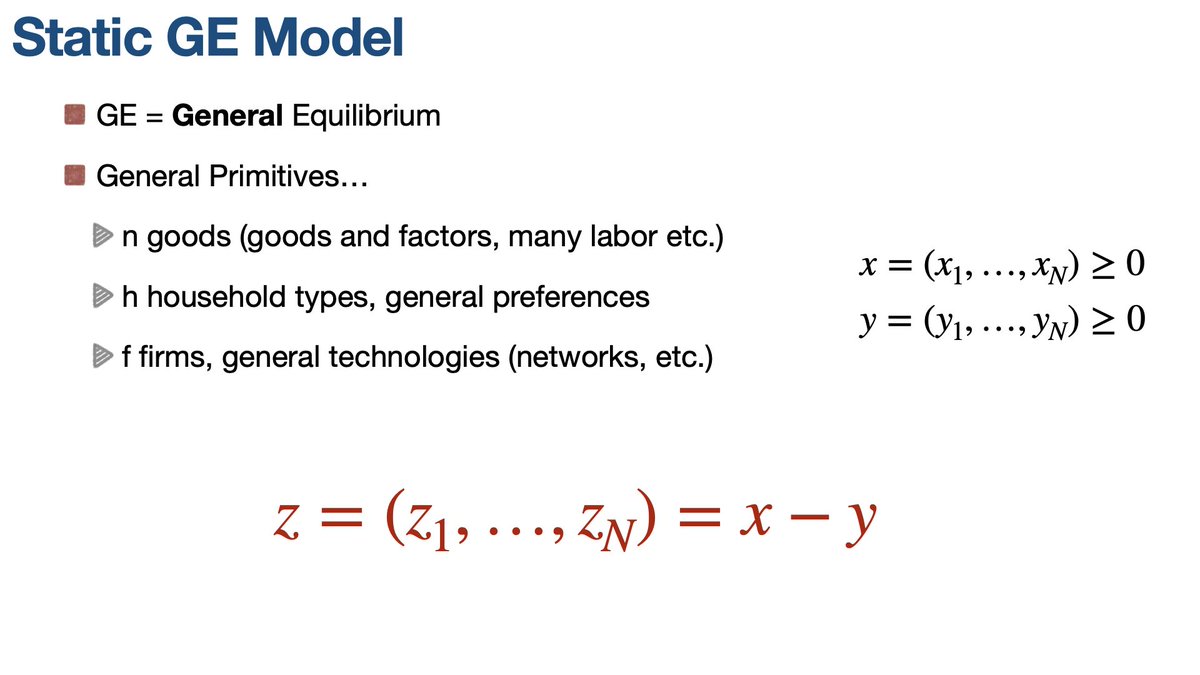

Framework: fully general GE...

any # of goods (labor)

any # households + preferences

any # firms _ technologies

pricing: market power+friction

Take best of both literatures+tâtonnement spirit...

—> new excess-demand approach

—> pricing with excess demands

Framework: fully general GE...

any # of goods (labor)

any # households + preferences

any # firms _ technologies

pricing: market power+friction

(after all, GE has word General in it!)

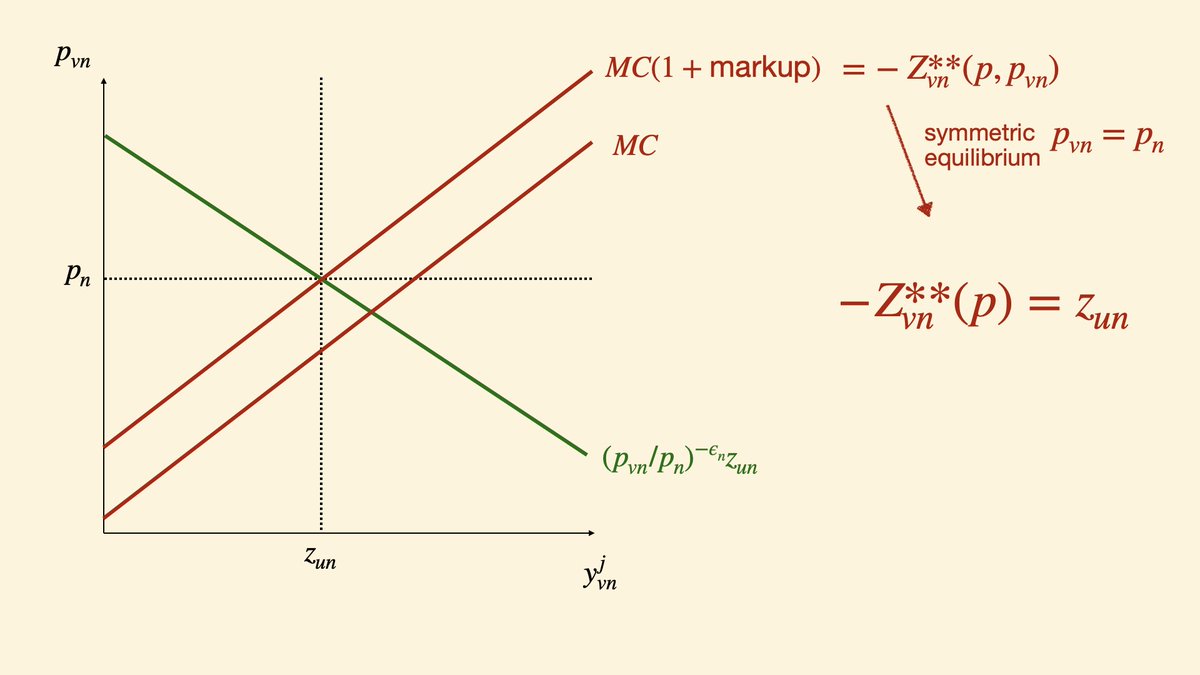

First stop: static model + flex prices + market power

Each market n has 2 sides

Differentiated: sets prices, has variety (e.g. baker)

Undifferentiated: chooses quantities, is fungible (e.g. shoppers)

Allow: Monopolistic or Monopsonistic.

First stop: static model + flex prices + market power

Each market n has 2 sides

Differentiated: sets prices, has variety (e.g. baker)

Undifferentiated: chooses quantities, is fungible (e.g. shoppers)

Allow: Monopolistic or Monopsonistic.

Elements standard in trade, growth, macro... but more general backbone.

Result: one can define excess demands Z(p) that encapsulate both price and quantity choices!

Intuition: choose a price freely —> choose your quantity!

Thus: "pricing as if quantity choice"

Implication: ...

Result: one can define excess demands Z(p) that encapsulate both price and quantity choices!

Intuition: choose a price freely —> choose your quantity!

Thus: "pricing as if quantity choice"

Implication: ...

Implication: equilibrium condition as if walrasian (despite market power) for price vector p:

Zn(p)=0

for all markets n.

Simple! Nice connection. But so what? This was warm up!

Second Stop: adding price frictions in static...

redo disequilibrium and demand "spillovers"

Zn(p)=0

for all markets n.

Simple! Nice connection. But so what? This was warm up!

Second Stop: adding price frictions in static...

redo disequilibrium and demand "spillovers"

Result 1: We now need to adjust Z(p) for spillovers. We show how to do that in closed form. See below, where A=spillover matrix. Reminiscent of network input-output theory.

Result 2: Allow single baker to reset price = "price pressure"...

price pressure= proportional to Z(p)

Result 2: Allow single baker to reset price = "price pressure"...

price pressure= proportional to Z(p)

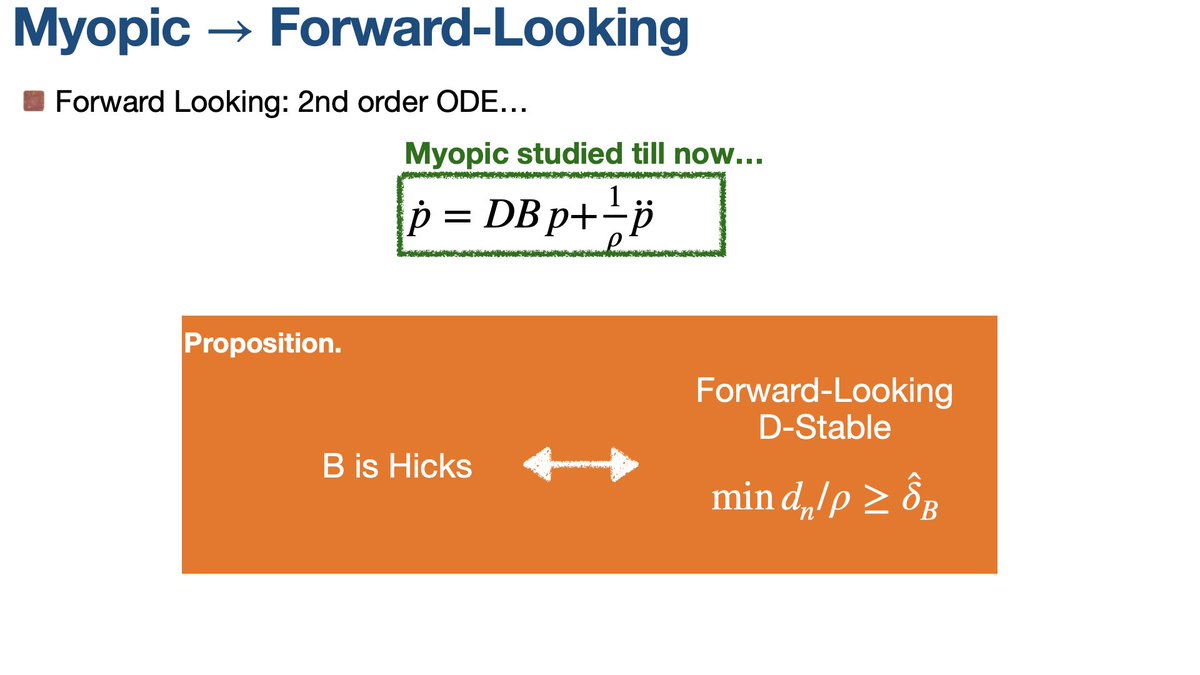

Next Stop: Dynamic Model with Pricing Frictions

Wait, why pricing frictions?

1. realistic prices not fully infinitely flexible!

2. we want non-trivial dynamics for prices, like Samuelson's "p dot" ODE...

Wait, why pricing frictions?

1. realistic prices not fully infinitely flexible!

2. we want non-trivial dynamics for prices, like Samuelson's "p dot" ODE...

Main result: excess demands and price pressure idea works here too!… in each market n

…price change today is proportional to weighted average of excess demand in that market only of today and future.

Intuitive? Yes! We love that! What micro 101 teaches!

A big deal since...

…price change today is proportional to weighted average of excess demand in that market only of today and future.

Intuitive? Yes! We love that! What micro 101 teaches!

A big deal since...

Big deal for us...

1. intuitive+simple+general: yet not obtained before

(requires our excess demand approach)

2. connects to tâtonnement!

—> dynamic forward-looking tâtonnement!

3. (next paper): useful way to do macro!

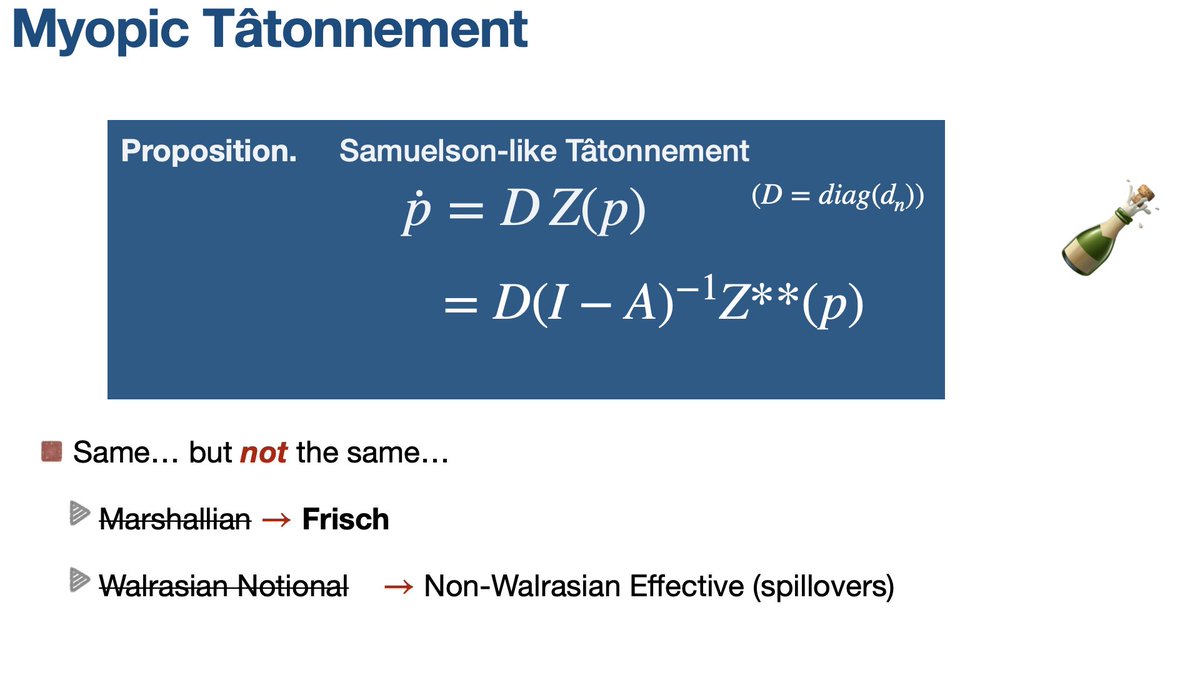

Myopic limit —> get a Samuelson-like tatonnement...

1. intuitive+simple+general: yet not obtained before

(requires our excess demand approach)

2. connects to tâtonnement!

—> dynamic forward-looking tâtonnement!

3. (next paper): useful way to do macro!

Myopic limit —> get a Samuelson-like tatonnement...

So Samuelson was right?

Yes and no!...

Yes, in form, but NO: the demand Z(p)...

1. not Marshallian uncompensated Z

intertemporal household...

—> Z is "Frisch" with no income effects!

… NOT ANYTHING GOES!

2. Spillover adjusted Z a earlier closed form!

Implications...

Yes and no!...

Yes, in form, but NO: the demand Z(p)...

1. not Marshallian uncompensated Z

intertemporal household...

—> Z is "Frisch" with no income effects!

… NOT ANYTHING GOES!

2. Spillover adjusted Z a earlier closed form!

Implications...

Implication...

Frisch nature of demand

—> strong force for stability

Sharpest Result: absent spillovers —> global stability!

Corollary: Scarf examples always stable in our dynamic setting!

Paper: many other results covering spillovers.

Frisch nature of demand

—> strong force for stability

Sharpest Result: absent spillovers —> global stability!

Corollary: Scarf examples always stable in our dynamic setting!

Paper: many other results covering spillovers.

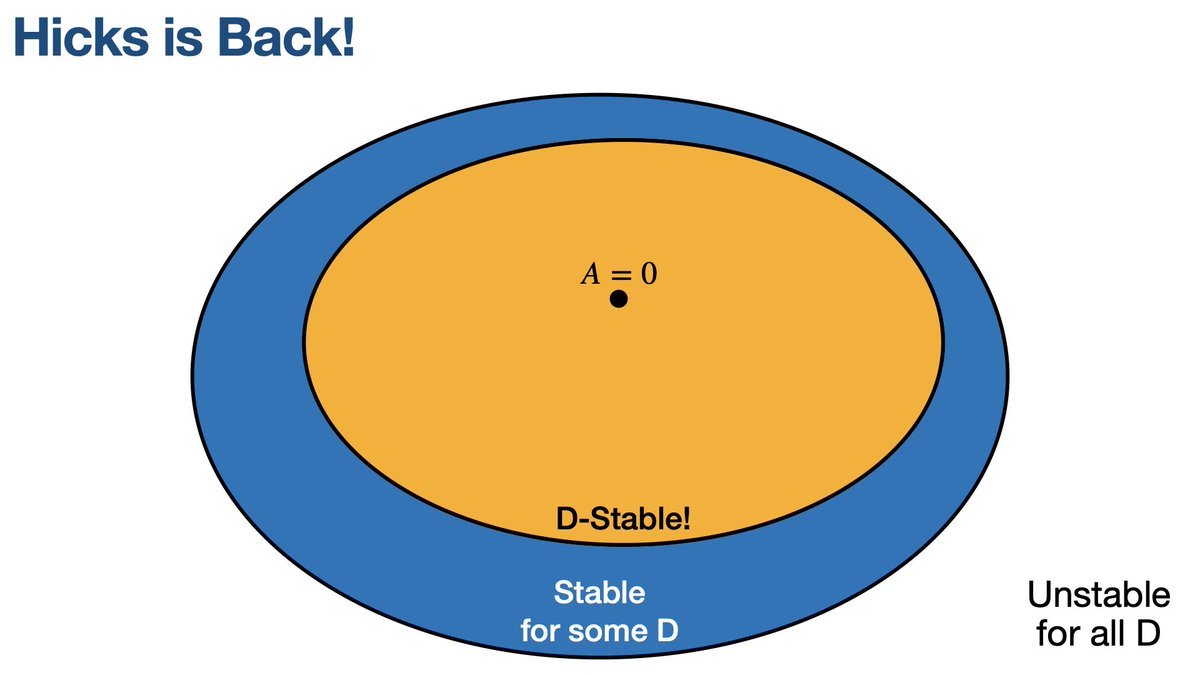

Result: A form of Law of Demand implies stability for all speeds, a robust form of stability called D-stability in literature.

Hicks Condition = even weaker form of Law of Demand

… is necessary for D-stability, but not sufficient.

...until now…. (surprising result coming)

Hicks Condition = even weaker form of Law of Demand

… is necessary for D-stability, but not sufficient.

...until now…. (surprising result coming)

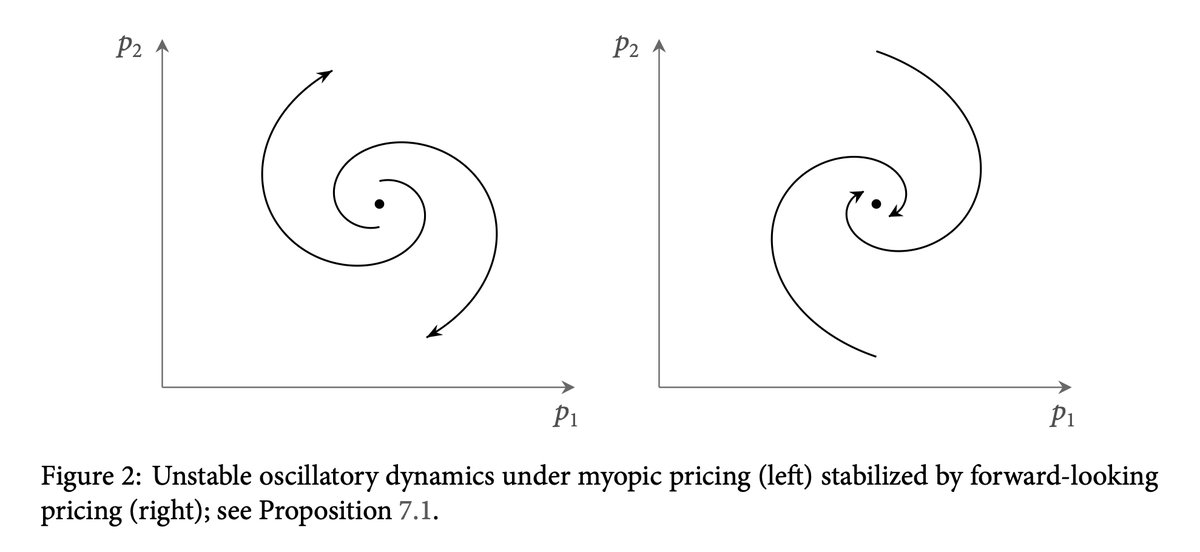

2nd strong force for stability from...

… forward looking price setting!

Result 1: more forward looking

—> grows set stable economies!

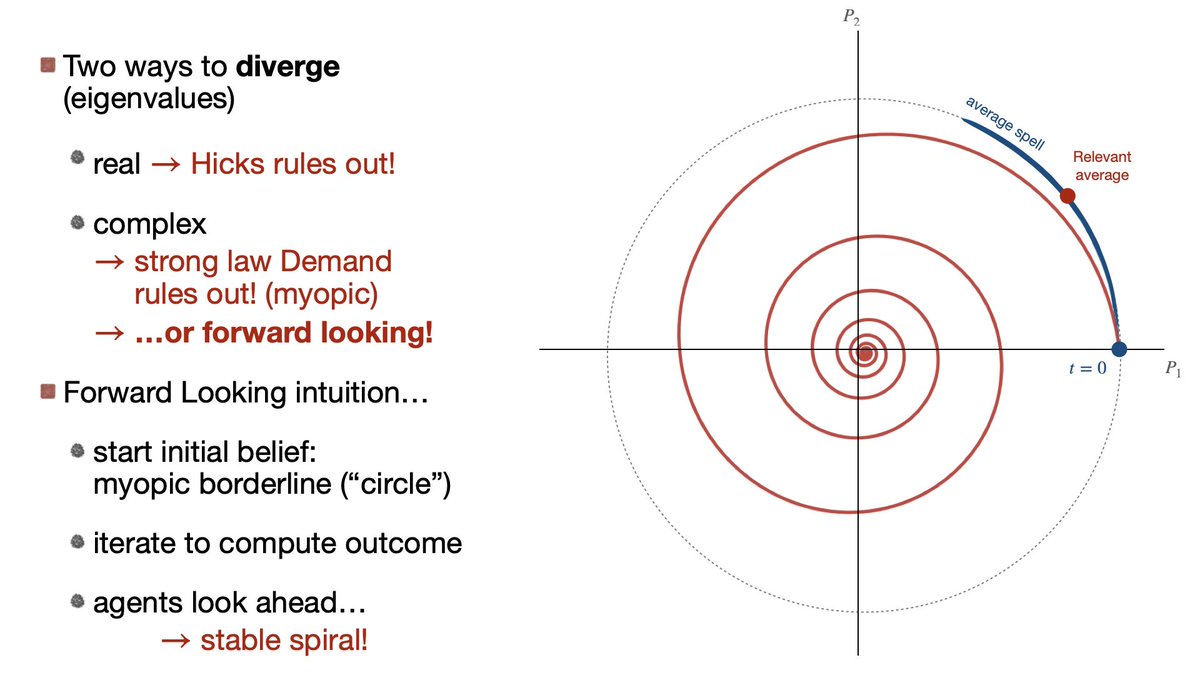

Result 2: in fully forward looking pricing

—> all oscillatory instability

—> becomes stabilized!

… this shocked us 😱… unexpected

… forward looking price setting!

Result 1: more forward looking

—> grows set stable economies!

Result 2: in fully forward looking pricing

—> all oscillatory instability

—> becomes stabilized!

… this shocked us 😱… unexpected

Finally, poor Hicks, so toughly criticized…

… we felt we had to do something for him…

His condition does not imply robust stability with myopic pricing...

… but what about with forward-looking pricing?

What are the chances…? 🎲 🃏 🎰...

… we felt we had to do something for him…

His condition does not imply robust stability with myopic pricing...

… but what about with forward-looking pricing?

What are the chances…? 🎲 🃏 🎰...

Result: Hicks is Back!

With fully forward-looking pricing the Hicks condition is necessary and sufficient for robust D-stability.

… did Hicks know this all along?! ;)

With fully forward-looking pricing the Hicks condition is necessary and sufficient for robust D-stability.

… did Hicks know this all along?! ;)

Intuitions?

We offer intuition for this unexpected result... it actually makes a lot of sense! 🥳

Q: How do oscillatory unstable spirals get stabilized??

A: When price setters anticipate getting ahead of the curve, they bend the curve! ... ⚽️

We offer intuition for this unexpected result... it actually makes a lot of sense! 🥳

Q: How do oscillatory unstable spirals get stabilized??

A: When price setters anticipate getting ahead of the curve, they bend the curve! ... ⚽️

Intuition 2.0

Price setters average the future, with sprials this pushes them to act as if prices lean into the steady state

---> that then takes us to steady state!

— stabilizing force from dynamic forward looking!

Let's finish this!...

Price setters average the future, with sprials this pushes them to act as if prices lean into the steady state

---> that then takes us to steady state!

— stabilizing force from dynamic forward looking!

Let's finish this!...

One more thing...

Pricing becomes fully forward looking if impatience goes to zero, but ALSO….

… as prices become very flexible. So if we think of walraisan economics as a flexible limit, we get these stability forces at full.

Pricing becomes fully forward looking if impatience goes to zero, but ALSO….

… as prices become very flexible. So if we think of walraisan economics as a flexible limit, we get these stability forces at full.

Skipped a lot, lots more in paper. Link at the end.

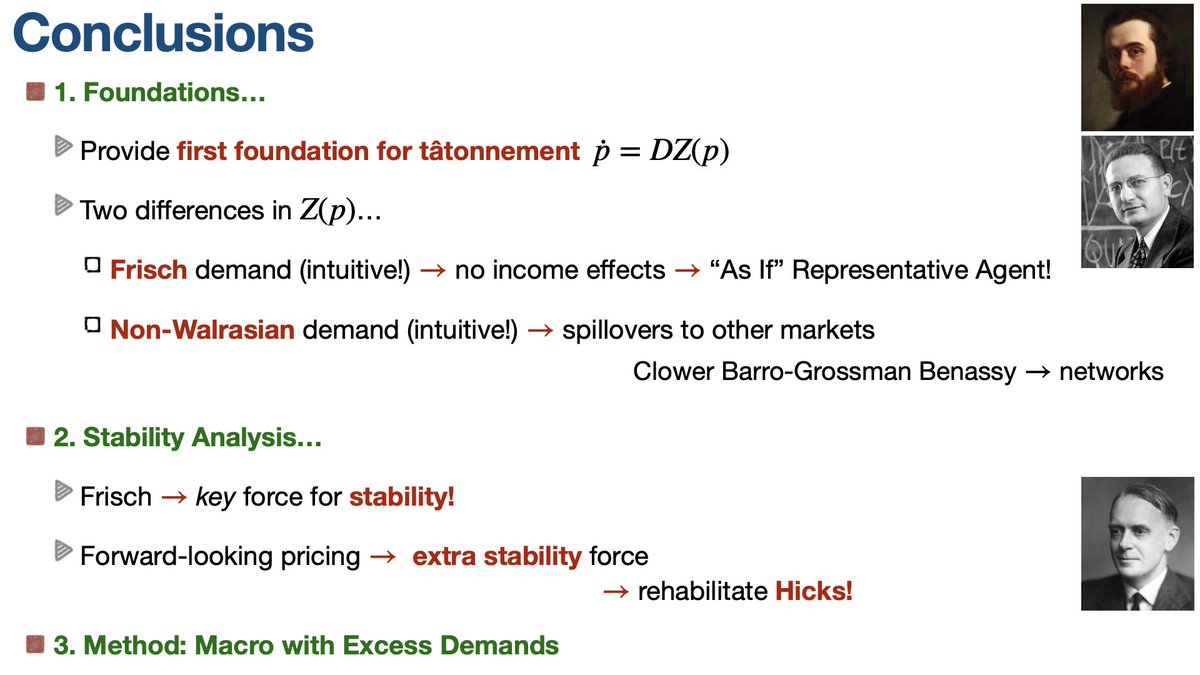

1. we provide foundations for Walras

2. justify Samuelson's ad hoc equation, but

3. … not the same because of demands

4. reinstate Sir John Hicks

2 forces for stability

A. Frisch demands!

B. Forwards looking pricing!

1. we provide foundations for Walras

2. justify Samuelson's ad hoc equation, but

3. … not the same because of demands

4. reinstate Sir John Hicks

2 forces for stability

A. Frisch demands!

B. Forwards looking pricing!

Link to paper… (or DM or email me)

cc'ing the great Guido, follow him: @guido_lorenzoni

That's all FOLKS! It was a lot, sorry!dropbox.com/scl/fi/jtra55d…

cc'ing the great Guido, follow him: @guido_lorenzoni

That's all FOLKS! It was a lot, sorry!dropbox.com/scl/fi/jtra55d…

• • •

Missing some Tweet in this thread? You can try to

force a refresh