The argument that China has a comparative advantage at industrial policy is a bit like the argument that the US has a comparative advantage at exporting debt. It is a good line, but even quips need a limiting principle ...

1/

1/

I am not sure this week's Free Lunch column came up with that limiting principle; the notion that "the west might be better off simply leveraging the benefits of Chinese scale" suggests getting out of China's way across the board

2/

ft.com/content/42fc2e…

2/

ft.com/content/42fc2e…

But China has -- in Greg Ip's phrase (based on Rhodium's analysis) -- an "industrial policy for everything," which would imply that China is on track (with its comparative advantage at industrial policy) to dominate most industrial sectors

3/

wsj.com/world/china/be…

3/

wsj.com/world/china/be…

China's industrial policy targets now include quantum, advanced semiconductors, advanced chip making equipment (EUV), legacy analogue chips (many military applications), civil aircraft, and top of the line jet engines --

4/

4/

I think most people would consider those sectors to be important for either national or economic security -- so letting China exercise its comparative advantage in "industrial policy" unchallenged would mean accepting real security trade offs

5/

5/

Does exploiting China's scale extend to its clear existing scale in rare earth processing and refining (including the rare earths that have very clear and important military applications) + its edge in manufacturing magnets that use those rare earths?

6/

6/

That means accepting dependence on China for components used in high end interceptors, nuclear subs and stealth fighters/ their radars -- which seems unwise ... yet those are the sectors were China has scale and a clear cost edge ...

7/

7/

If drone technology is really critical to the future of war (as many think) and massing large numbers of drones so as to overwhelm defensive systems is a big part of that is it tenable to rely on China's battery chemicals and batteries (no one questions China's scale there) indefinitely?

8/

8/

Innovation equally doesn't just come from universities. China's edge in rare earths reflects mastering a set of process technologies - countries with no rare earth refining today won't have any chance of developing those innovations ...

As @SanderTordoir likes to note, ASLM emerged out of Philips and thus out of the engineers trained in Dutch semiconductor production -- so I at least would question the assumption that innovation is entirely separate from participating in cutting edge industries ...

10/

10/

The history of civil aviation also suggests that the West isn't always bad at industrial policy. Airbus was an industrial policy success for France, Germany, the UK and Spain (it also on net made money for the governments involved, their profits on the 320 and 350 will cover losses on the 340 and 380)

11/

11/

@SanderTordoir Boeing equally emerged out of the massive investment the US made in aircraft production in the 40s and jet aircraft production in the 50s ...

11/

11/

@SanderTordoir I at least would argue that a big barrier to investment (and the innovations that come from producing the world's most advanced goods) right now is the prospect of competing against Chinese state subsidies & Chinese firms that can export at an undervalued exchange rate

12/

12/

@SanderTordoir The seductive arguments of Free Lunch (no need to actually get your hands dirty and compete in sectors where China has erased returns ... move to the easy profit in service sectors ... ) also leave out the role of macroeconomics in China's industrial success ...

13/

13/

@SanderTordoir The theory of comparative advantage argues having a successful industrial policy for everything -- the whole point of exporting in Ricardo is to be able to import more, which is what China conspicuously doesn't do right now ...

14/

14/

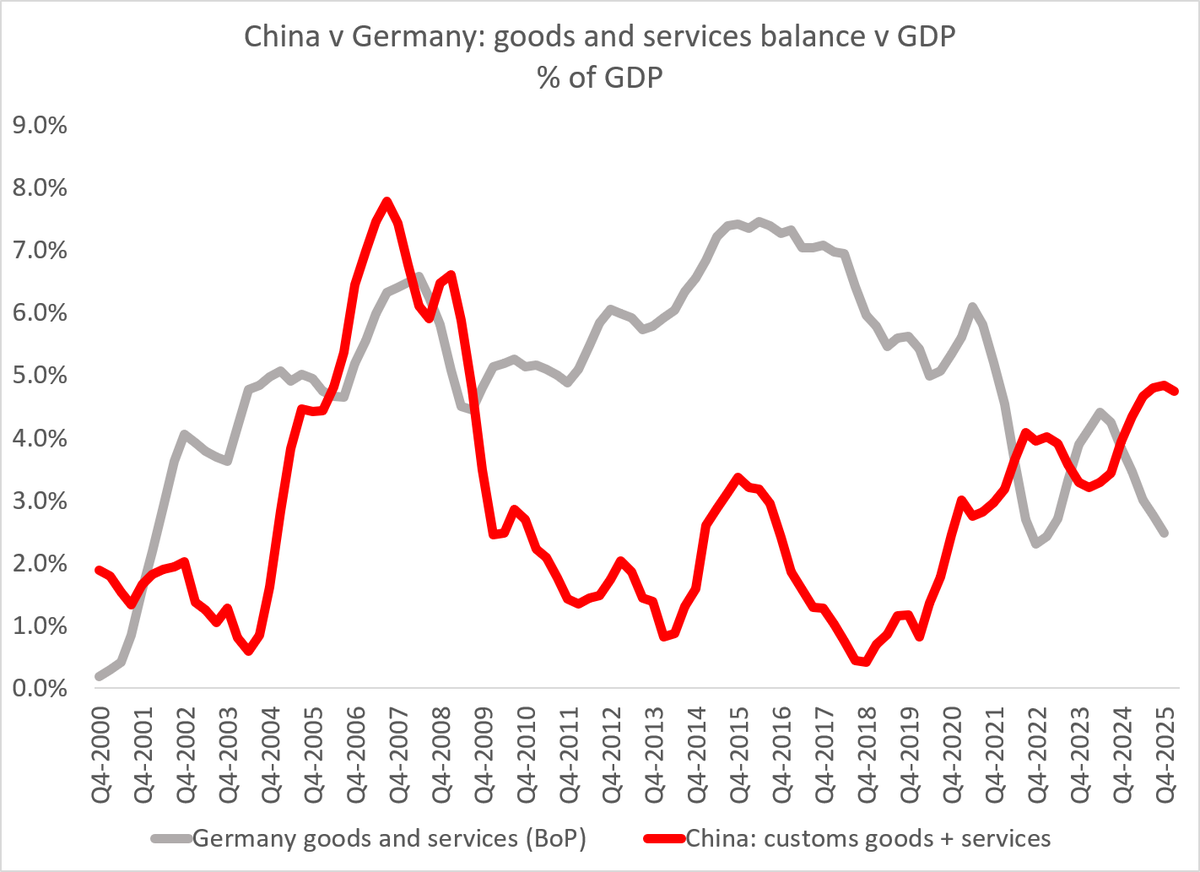

China isn't just an outlier in its ability to do industrial policy/ state capitalism well (and absorb large losses along the way), it is an outlier on a number of macroeconomic variables which have created an economy that has to export to offset its internal weaknesses

15/

15/

• • •

Missing some Tweet in this thread? You can try to

force a refresh