What's the better business model for an AI lab, subscription or API? (1/4)🧵

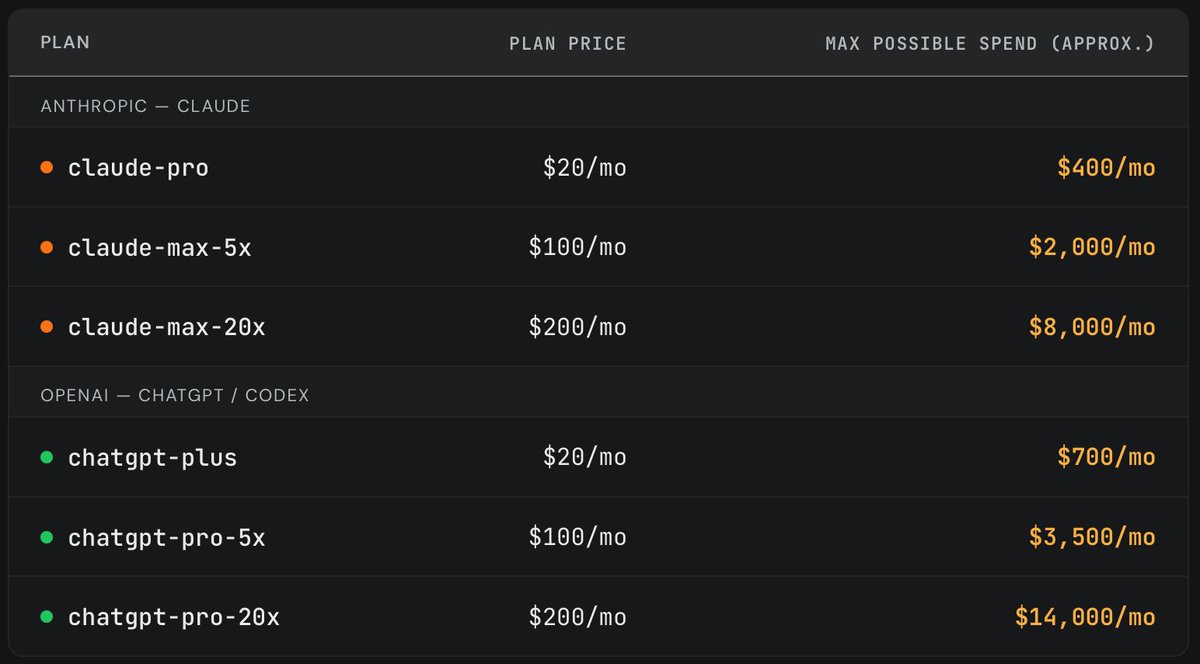

Recently, we purchased one of each Anthropic/OpenAI subscription plan and randomly ran long horizon coding tasks until we exhausted the weekly limit. It's widely believed that a $200/month plan maxes out at ~$2000/month worth of tokens (assuming API pricing). However, we found that the subscriptions are actually far more generous. (2/4)

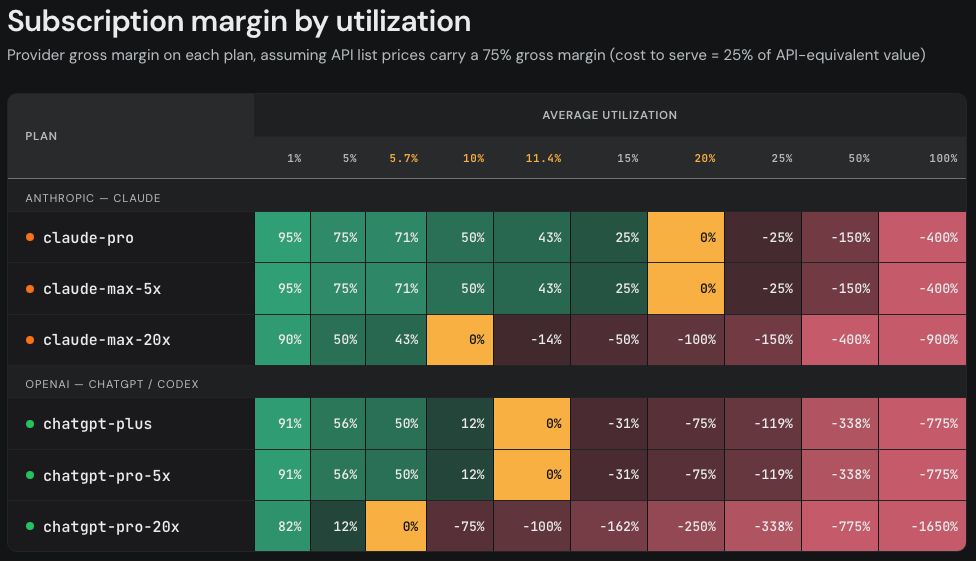

The margin on a subscription plan is a function of the average utilization. If we assume both companies have 75% API gross margins, this results in the following subscription margins. (3/4)

Obviously this is way worse than API overall. However, explicitly nerfing subscriptions leads to huge public backlash, and the rapidly falling cost of intelligence means you'll be able to profitably serve Opus 4.8 level models for $20/month in the near future. We therefore think it's far more likely the labs will withhold new features/models from subscription plans. It will be interesting to see if Mythos ends up being API only. (4/4)

• • •

Missing some Tweet in this thread? You can try to

force a refresh