1/9

Eric asks a reasonable question: what should be done about a future stock market slump? Specifically, should the Fed buy stocks?

🧵

tl:dr

* The legal process for the Fed buying stocks means the Treasury actually owns them, the Fed finances it by extending loans to buy the stocks.

* Trump will love this idea, as he wants a Sovereign Wealth Fund, and now has the Government holding several US companies. We suspect he will probably want these stocks as permanent government holdings, up to 20% of the stock market ($16n trillion of stocks).

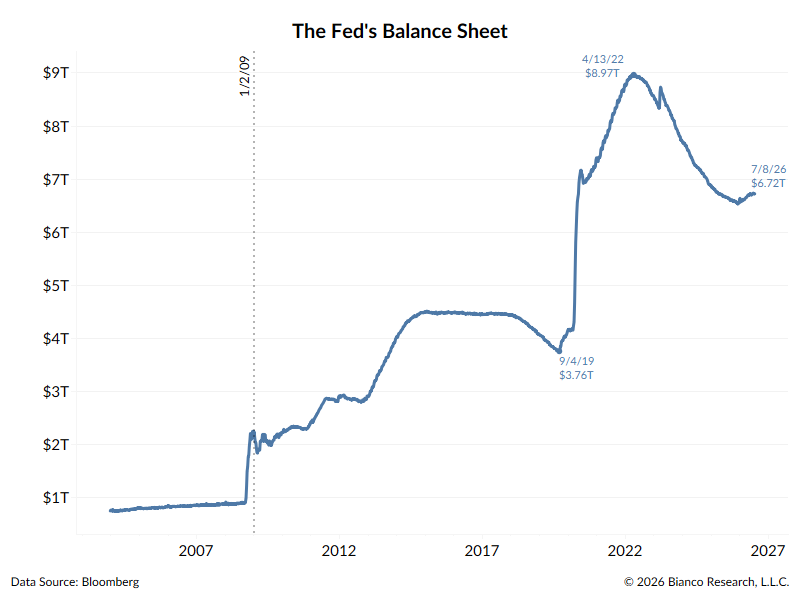

* This would balloon the Fed's balance sheet to $25 trillion (from $6.7 trillion now).

* What would be the reaction to the balance sheet ballooning to $25 trillion? Bullish as that means massive buying of stocks? Bearish as the market fears another inflation spurt, and accompanied interest rate rise? Remember, 2022 inflation hit 9%, interest rates soared and the S&P 500 fell 25%.

* We think the Fed buying of 2008 and 2020 worked to "save" markets as deflation was the bigger concern than inflation. But now with elevated inflation (as in the last 6 years), anything that looks inflationary would be received badly by financial markets.

All these bullet points are detailed below.

Eric asks a reasonable question: what should be done about a future stock market slump? Specifically, should the Fed buy stocks?

🧵

tl:dr

* The legal process for the Fed buying stocks means the Treasury actually owns them, the Fed finances it by extending loans to buy the stocks.

* Trump will love this idea, as he wants a Sovereign Wealth Fund, and now has the Government holding several US companies. We suspect he will probably want these stocks as permanent government holdings, up to 20% of the stock market ($16n trillion of stocks).

* This would balloon the Fed's balance sheet to $25 trillion (from $6.7 trillion now).

* What would be the reaction to the balance sheet ballooning to $25 trillion? Bullish as that means massive buying of stocks? Bearish as the market fears another inflation spurt, and accompanied interest rate rise? Remember, 2022 inflation hit 9%, interest rates soared and the S&P 500 fell 25%.

* We think the Fed buying of 2008 and 2020 worked to "save" markets as deflation was the bigger concern than inflation. But now with elevated inflation (as in the last 6 years), anything that looks inflationary would be received badly by financial markets.

All these bullet points are detailed below.

https://x.com/biancoresearch/status/2074510947289358577

2/9

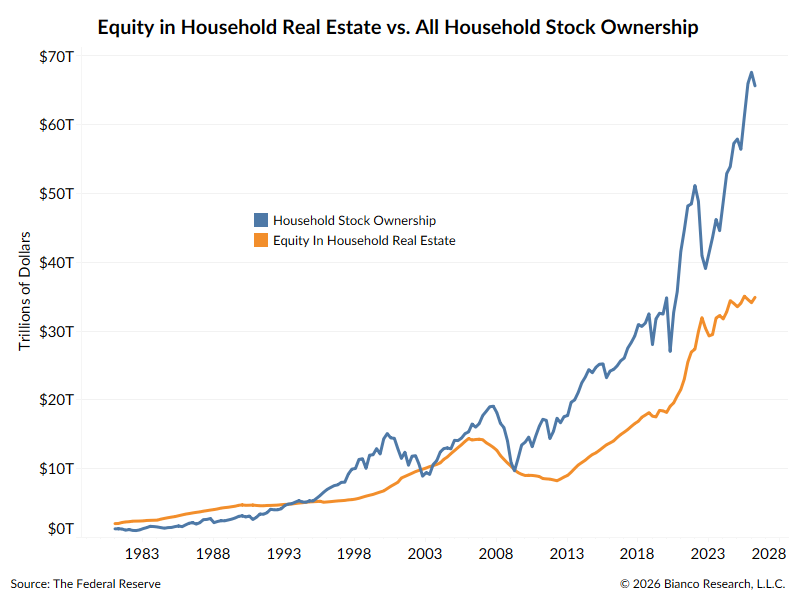

First, Eric is correct in his comment about the stock market:

--

The stock market increasingly functions as America’s de facto retirement system, with roughly 58% of Americans now owning stocks — a figure that could approach 70% as Trump Accounts add millions of investors. As equities become more central to household wealth, voter behavior, and financial stability, the political and economic cost of a prolonged bear market has rarely been higher.

---

He also goes on to say:

---

One could even argue it has become more important than Social Security, which is on track to exhaust its trust fund reserves within the next decade.

First, Eric is correct in his comment about the stock market:

--

The stock market increasingly functions as America’s de facto retirement system, with roughly 58% of Americans now owning stocks — a figure that could approach 70% as Trump Accounts add millions of investors. As equities become more central to household wealth, voter behavior, and financial stability, the political and economic cost of a prolonged bear market has rarely been higher.

---

He also goes on to say:

---

One could even argue it has become more important than Social Security, which is on track to exhaust its trust fund reserves within the next decade.

3/9

Global housing prices are similarly considered vital retirement assets. Government policies and programs are openly designed to manipulate prices higher, and then offer additional programs for first-time homebuyers to buy homes they otherwise could not afford.

Stocks mean more to households than housing.

Global housing prices are similarly considered vital retirement assets. Government policies and programs are openly designed to manipulate prices higher, and then offer additional programs for first-time homebuyers to buy homes they otherwise could not afford.

Stocks mean more to households than housing.

4/9

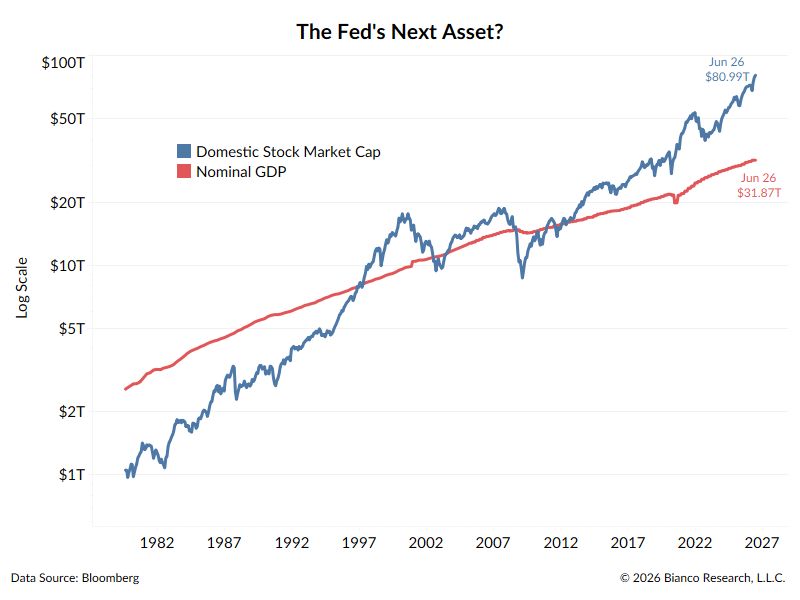

So, why not treat the stock market the same way? If the Fed can buy mortgage-backed securities to help homeowners, why not U.S. stocks? After all, the stock market is larger than the economy.

So, why not treat the stock market the same way? If the Fed can buy mortgage-backed securities to help homeowners, why not U.S. stocks? After all, the stock market is larger than the economy.

5/9

How Would the Fed Buy Stocks?

The Fed’s ordinary purchase authority is limited to Treasuries and government-backed mortgage securities — it cannot buy corporate bonds or equities outright.

In both 2008 and 2020, it worked around that limit the same way: the Fed set up a Special Purpose Vehicle (SPV), the Treasury supplied equity as a loss-absorbing cushion, and the Fed made a secured loan to the SPV, which used the combined funds to buy the actual securities.

That financing structure — not a change in what the Fed can legally own — is what let it reach mortgage assets, corporate bonds and ETFs during past crises:

2008: The Fed used three Maiden Lane SPVs (named for the street the New York Fed sits on) to buy troubled Bear Stearns and AIG assets, plus TALF, which made loans against AAA-rated asset-backed securities.

2020: a similar alphabet soup did the same for other markets — PMCCF/SMCCF for corporate bonds and bond ETFs, plus separate facilities for money-market funds, commercial paper, PPP loans, mid-sized business loans and municipal debt.

These procedures are noted to point out the fact that it’s the Treasury, not the Fed, that would end up owning the stocks. The Fed’s role is to finance the purchase, not make it directly.

How Would the Fed Buy Stocks?

The Fed’s ordinary purchase authority is limited to Treasuries and government-backed mortgage securities — it cannot buy corporate bonds or equities outright.

In both 2008 and 2020, it worked around that limit the same way: the Fed set up a Special Purpose Vehicle (SPV), the Treasury supplied equity as a loss-absorbing cushion, and the Fed made a secured loan to the SPV, which used the combined funds to buy the actual securities.

That financing structure — not a change in what the Fed can legally own — is what let it reach mortgage assets, corporate bonds and ETFs during past crises:

2008: The Fed used three Maiden Lane SPVs (named for the street the New York Fed sits on) to buy troubled Bear Stearns and AIG assets, plus TALF, which made loans against AAA-rated asset-backed securities.

2020: a similar alphabet soup did the same for other markets — PMCCF/SMCCF for corporate bonds and bond ETFs, plus separate facilities for money-market funds, commercial paper, PPP loans, mid-sized business loans and municipal debt.

These procedures are noted to point out the fact that it’s the Treasury, not the Fed, that would end up owning the stocks. The Fed’s role is to finance the purchase, not make it directly.

6/9

Trump’s Reaction

The Trump Administration is actively trying to create a sovereign wealth fund, so a structure like the one above, which would give the Treasury a way to buy vast swaths of the stock market, would likely be approved.

The current administration has already taken equity stakes in several other companies, and has reportedly discussed a similar stake in OpenAI:

* Intel — 10% stake, $8.9 billion (Aug. 2025)

MP Materials — up to 15% stake, $400 million (Jul. 2025)

* Lithium Americas — 5% direct stake plus 5% in its GM joint venture (Oct. 2025)

* Trilogy Metals — 10% stake plus warrants for another 7.5% (Oct. 2025)

* Vulcan Elements — $50 million equity stake (Nov. 2025)

* USA Rare Earth — 10% stake, part of a $1.6 billion package (Jan. 2026)

* IBM — up to $1 billion minority stake in its new Anderon quantum-chip subsidiary (May 2026)

Trump’s Reaction

The Trump Administration is actively trying to create a sovereign wealth fund, so a structure like the one above, which would give the Treasury a way to buy vast swaths of the stock market, would likely be approved.

The current administration has already taken equity stakes in several other companies, and has reportedly discussed a similar stake in OpenAI:

* Intel — 10% stake, $8.9 billion (Aug. 2025)

MP Materials — up to 15% stake, $400 million (Jul. 2025)

* Lithium Americas — 5% direct stake plus 5% in its GM joint venture (Oct. 2025)

* Trilogy Metals — 10% stake plus warrants for another 7.5% (Oct. 2025)

* Vulcan Elements — $50 million equity stake (Nov. 2025)

* USA Rare Earth — 10% stake, part of a $1.6 billion package (Jan. 2026)

* IBM — up to $1 billion minority stake in its new Anderon quantum-chip subsidiary (May 2026)

7/9

Would Stock Buying Be Permanent?

Additionally, Trump would most likely argue that any such purchases of stocks should be permanent rather than temporary. And don’t be surprised if he wants to include crypto in the mix.

Given some of Trump’s previous comments, he might be in favor of the Treasury holding 10% to 20% of the U.S. stock market ($8 to $16 trillion, based on the market’s roughly $80 trillion size). Given that the Fed’s balance sheet currently stands at $6.7 trillion, this would roughly double to triple its size.

What would be the market reaction to the Fed’s balance sheet rocketing to $25 trillion?

Would Stock Buying Be Permanent?

Additionally, Trump would most likely argue that any such purchases of stocks should be permanent rather than temporary. And don’t be surprised if he wants to include crypto in the mix.

Given some of Trump’s previous comments, he might be in favor of the Treasury holding 10% to 20% of the U.S. stock market ($8 to $16 trillion, based on the market’s roughly $80 trillion size). Given that the Fed’s balance sheet currently stands at $6.7 trillion, this would roughly double to triple its size.

What would be the market reaction to the Fed’s balance sheet rocketing to $25 trillion?

8/9

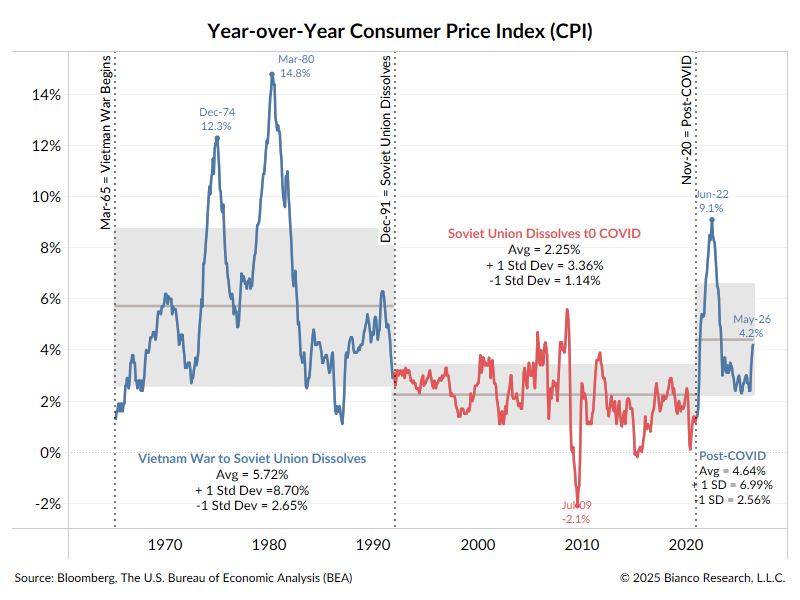

What Impact Would This Have?

We have argued that one reason the 2008 and 2020 programs worked was that markets were more worried about deflation than inflation.

But since 2020, inflation has been front and center. CPI is running at a 4.2% annual rate as of May 2026, the highest since 2023.

The following chart is a color-coded version of CPI. The Fed buying stocks during the quiet inflation period of the red section worked. But will it work in the elevated section of the leftmost blue area?

What Impact Would This Have?

We have argued that one reason the 2008 and 2020 programs worked was that markets were more worried about deflation than inflation.

But since 2020, inflation has been front and center. CPI is running at a 4.2% annual rate as of May 2026, the highest since 2023.

The following chart is a color-coded version of CPI. The Fed buying stocks during the quiet inflation period of the red section worked. But will it work in the elevated section of the leftmost blue area?

9/9

Ballooning the balance sheet by the amount noted above could scare the market into thinking a re-run of 2022 is happening, which produced 9% inflation and a 25% correction in the S&P 500. Anything less than $7 trillion might not be enough to make a difference, and Trump might demand the Fed buy at least this much, even if stocks recover.

Simply put, it is possible government stock purchases could exacerbate a selloff because of inflation fears.

Ballooning the balance sheet by the amount noted above could scare the market into thinking a re-run of 2022 is happening, which produced 9% inflation and a 25% correction in the S&P 500. Anything less than $7 trillion might not be enough to make a difference, and Trump might demand the Fed buy at least this much, even if stocks recover.

Simply put, it is possible government stock purchases could exacerbate a selloff because of inflation fears.

• • •

Missing some Tweet in this thread? You can try to

force a refresh