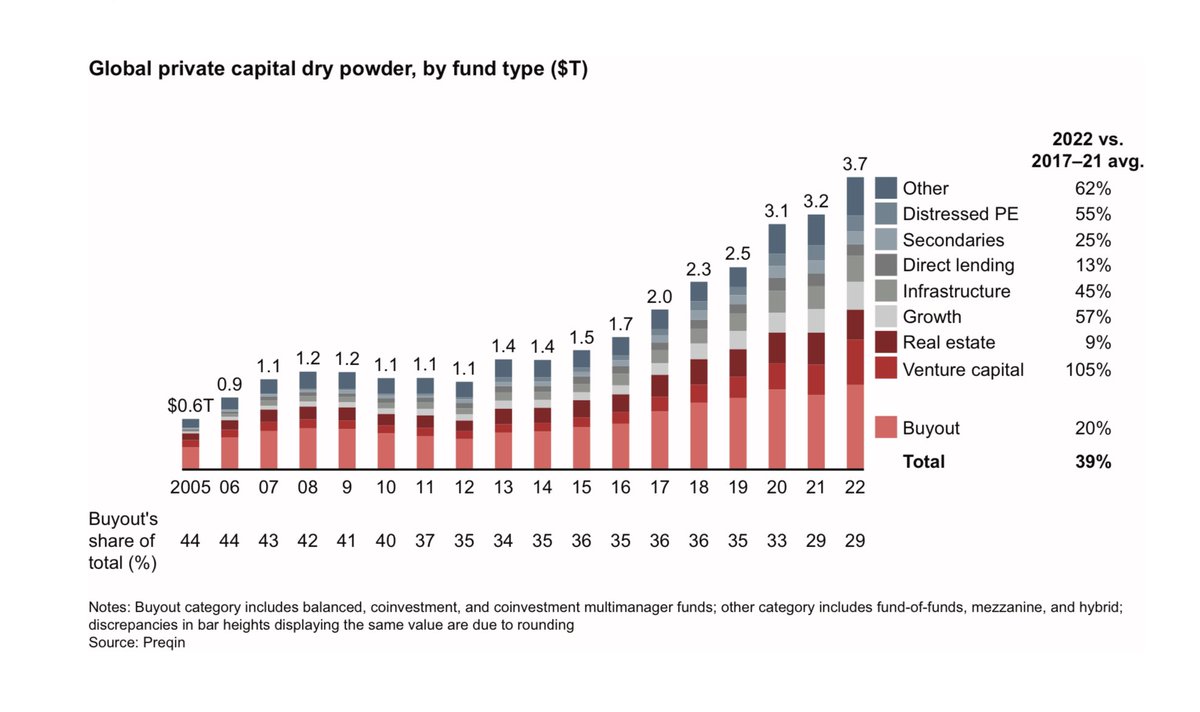

$1.3 trillion of that powder was raised in 2022 alone

$1.3 trillion of that powder was raised in 2022 alone

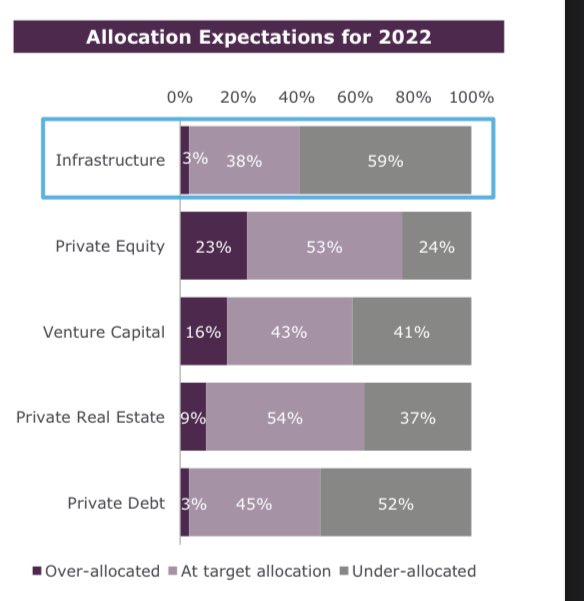

It also established its infrastructure business in 2008. Since then, it has scaled it to $50bn of AUM. Brookfield is well over $100bn of AUM in infra and still growing that biz quite rapidly. Most institutional investors feel under allocated to infra. Nice growth market for them.

It also established its infrastructure business in 2008. Since then, it has scaled it to $50bn of AUM. Brookfield is well over $100bn of AUM in infra and still growing that biz quite rapidly. Most institutional investors feel under allocated to infra. Nice growth market for them.