I invest in biotechs. I often tweet about companies I have positions in. Nothing I say should be considered investment advice.

Feb 24 • 17 tweets • 13 min read

Lot's of requests to discuss the Wedbush report on $ABVX today. It's a doozy. Obviously I'm a biased bull so sure, take my thoughts with a grain of salt, but this is truly, awful work from my perspective. Let's dig in on a few of the key issues.

"We are skeptical that efficacy signals will hold at a one-year readout."

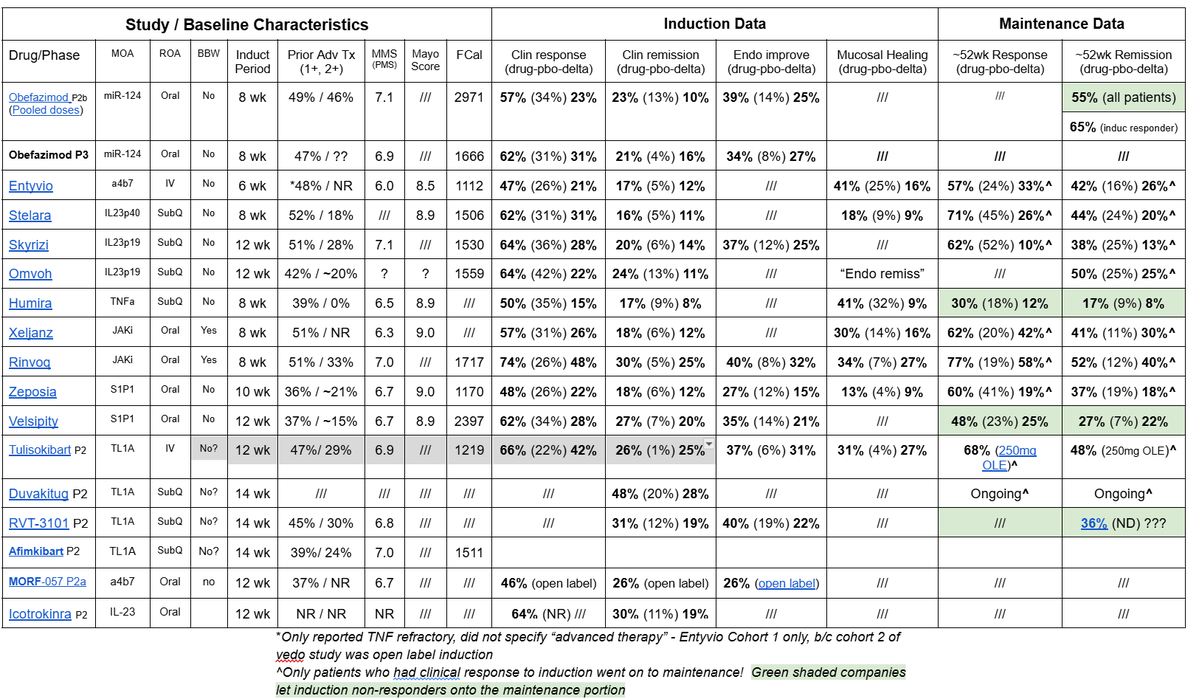

Ok, well, the bear thesis for $ABVX *used* to be that the induction was weak, whereas the maintenance data were super strong. *By far* the strong point of the P2 dataset was the maintenance data.

As I have previously discussed, $ABVX's P2 maintenance dataset showed a higher remission rate than literally any phase 3 trial has ever shown...And it actually wasn't even *close*.

When only looking at induction responders (which is how P3s are run), Obe produced a 65% remission rate...the 2nd highest of any drug was Rinvoq (top of the market efficacy) with 52%. 13% difference.

The caveat here is that ABVX's trial was open label, whereas the Rinvoq study was blinded. That makes a difference, but 13% is a hell of a lot of breathing room...In fact, that's higher than the placebo remission rate in Rinvoq's study!

And Rinvoq is above the rest of the pack. If you compare Obe's 65% to Entyvio (42%), Skyrizi (38%), or even the supposedly "exciting" TL1A inhibitors like Tuli (48%) and RVT-3101 (36%)....ABVX's 65% with Obe is blowing everything on the market out of the water. Yes, even stuff with safety warnings, yes even "novel" stuff like TL1A.

And that was in the P2 where the induction responses weren't even that strong...

So, Wedbush's first bear point is that they aren't sure that maintenance efficacy will hold up...OK...why? No reason? Just pure conjecture that goes directly in the face of the proof of concept data that we have.

Jan 14 • 10 tweets • 12 min read

I’ve gotten a lot of messages asking about my BioPick selection for this year, $TENX. I’ve responded to a few but don’t have the time to respond to everyone.

I actually considered making $TENX an official “pitch”, but I don’t think I can get there on the risk/reward skew to say that this is “one of the best setups I’ve ever seen” like I try to do for “official” pitches.

Still, it’s been an obscure name, and IMO very clearly has a heavily underappreciated 2026 catalyst that many people don't know about, so I think it's worth talking about. I am long currently and there’s a decent chance that I’ll be exposed to the binary - at least I think that I’ll be exposed to the readout if the stock stays at these prices going into the data.

So, I won’t pitch it with a comprehensive thread like $NKTR & $ABVX, and I won’t share my full large diligence document like I did for those. But, I hope the brief (by my standards) discussion here could lead to some solid sharing of thoughts with the “biotwitter” community. Frankly, I'm not even sure the best way to "play" this one, so some feedback and collective diligence here could be useful.

Everyone’s favorite part of the thread → Disclaimers!

First one is important - Don’t be fooled by your brokerage account telling you this has some tiny microcap valuation. There are lots of warrants outstanding from the company’s history, making the fully diluted share count more like ~65M (by my calculations).

Second, much like $ABVX, the downside on a total fail by $TENX is huge. Like 90%. I’d also say that, for $ABVX, I eventually arrived at such high confidence that they were going to hit that I’d almost have called that a "guarantee" (although nothing in biotech ever actually is). For TENX, the *massive* +500-1000% upside scenarios are certainly on the table like they were for $ABVX, but the odds of that happening versus the ~90% downside crash are certainly nowhere near as positively skewed for $TENX. THE BINARY HERE IS GOING TO BE RISKY.

Oct 6, 2025 • 7 tweets • 7 min read

THIS IS 🚨NOT🚨 A PITCH, but the $PALI story is a fascinating one, and I am currently long (and bought more this morning).

This is a wild story of a nanocap biotech that was valued at ~$8M only a few days ago, but has now burst onto the scene with a potentially unique approach to an increasingly validated target in IBD and >40x'd its "value" (a number which I think will likely continue to balloon today ).🎈

People will compare it to $ABVX given that both have QD oral treatments for IBD, but let's break down the specifics of the nascent $PALI story...

First...❓How did a seemingly left-for-dead ~$8M company raise $138M seemingly out of nowhere❓

Well, some keen observers noticed that on 10/6/15 (today) there was going to be a presentation of new data from a Chinese company testing their drug (Mufemilast) in UC. That presentation was a "prestigious" late-breaking presentation, placed immediately after highly anticipated data from...none other than $ABVX!

The tea leaves suggested that this meant the Mufemilast trial data were positive. This was important because $PALI's lead candidate has the same MoA as this Chinese drug (Mufemilast)

➡️PDE4i

Furthermore, one could look back at old data from 2018 where another PDE4i, apremilast (AKA Otzela) had shown signs of efficacy in UC. This further strengthened the idea that Mufemilast could positively validate $PALI's target. (More on the apremilast PoC later).

So, investors piled into this nanocap biotech in order to invest ahead of potentially validating data from a Chinese drug with the same MoA, raising $PALI's market cap from ~$8M to ~$330M in less than a week! 🤯

Jul 28, 2025 • 7 tweets • 9 min read

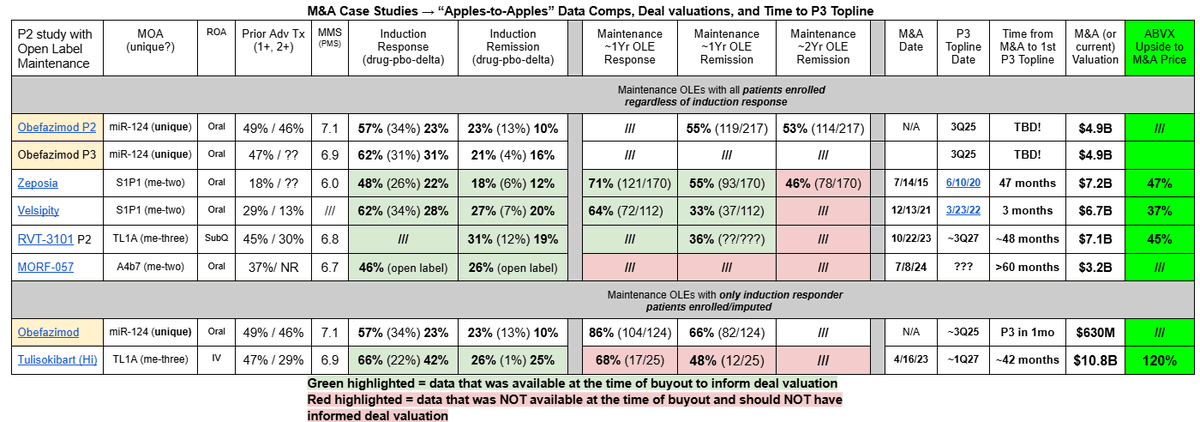

$ABVX may be up a lot since last week, but the upside from $66 remains significant. IMO, $ABVX is probably the single most obvious M&A candidate I have ever seen, and the price it's trading at remains quite attractive relative to M&A comps.

You could argue that UC has been the single biggest indication for biotech M&A over the last ~5 years. So far, essentially everything else that has made it past P2 successfully has been bought out (with lofty valuations to boot). $ABVX is in rare territory now, since nothing else like this has even made it this far (past P3) without getting bought out!

Let's go over $ABVX's data and compare it to M&A cases. I'll explain why $ABVX's final destination is, in my biased opinion, well north of $150/share.

1) What $ABVX Just Showed

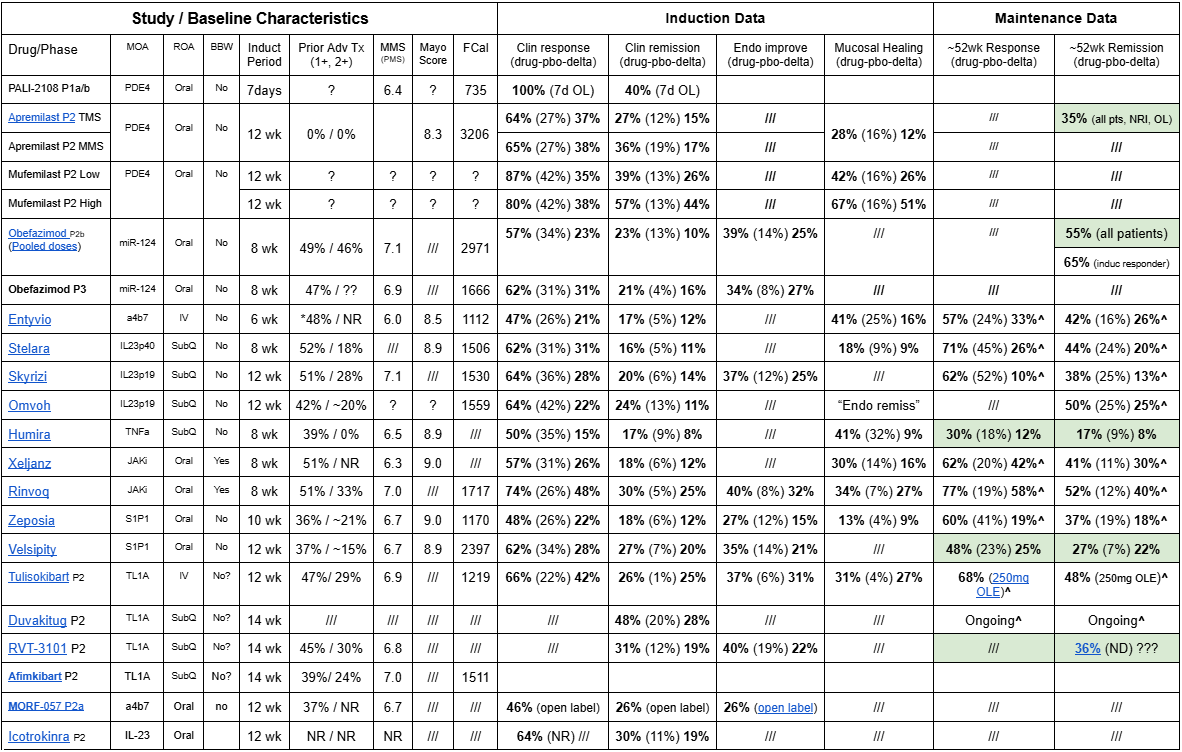

The results of their P3 studies were incredible. $ABVX has shown:

➡️The 3rd highest clinical remission delta ever seen in a P3 program (16.4%). The only two drugs to have higher deltas are Rinvoq and Veslipity, both with dangerous safety warnings on label.

➡️Squeaky clean safety. Adverse event rates were essentially the same on drug as with placebo...transient headaches were the only tolerability signal (already known from P2 data), and they only lasted an average of 2 days before going away on their own...

➡️Excellent Secondary Endpoint Efficacy. Specifically, a 27% endoscopic improvement delta (the most objective endpoint in UC) is the 2nd highest ever recorded in P3, exceeded only by Rinvoq (which has multiple potentially fatal side effects with black box warning).

$ABVX posted these incredible results despite the facts that:

➡️Their trial enrolled the highest percentage of JAKi refractory patients in any UC trial EVER. Much like their P2b, their P3 showed incredible results despite treating more severe patients than any comparator drug.

➡️Their induction timepoint was only 8 weeks. Most other new studies are using 12-14 week induction timepoints, because the remission delta increases with longer treatment. $ABVX cut no corners, and is still beating the comps that sandbag their data by running longer induction periods.

Top tier efficacy and water-like safety despite treating the most severe patient population ever, all in a convenient once-daily pill that requires no pre-initiation bloodwork/lab testing...this P3 readout for $ABVX was a GRAND SLAM.

Jul 21, 2025 • 12 tweets • 24 min read

I won't share in depth pitches like $NKTR often (2/year?). Only with really compelling setups. I've got another one now. The market says PoS is VERY low and that upside could be 10x+. Like with $NKTR, I think the data say success is far more likely than the market thinks.

The name is $ABVX (Abivax).

Like with $NKTR, I will share my long-form research on $ABVX, for free, via google doc (linked below). This $ABVX research is extensive, and the document is substantially longer than $NKTR’s was at ~25,000 words. It will take a lot to get through it, but I think the case for ABVX here is compelling. IMO the market hasn’t even remotely priced the stock correctly for what I think are relatively high odds of success yielding multibagger potential in August.

With that said, we need to cover some REALLY important notes on bias and risk:

1⃣ I am long $ABVX, meaning my opinions here are heavily biased. Keep this in mind throughout any of my research that you read.

2⃣THIS IS AN EXCEPTIONALLY RISKY READOUT WITH 90%+ DOWNSIDE POTENTIAL ⚠️📉⚠️

➡️NKTR’s downside potential was “only” ~50%. $ABVX is FAR riskier, and nearly your entire position could be wiped out when the data come if it fails. PLEASE consider the extreme risk involved in this setup!!!

Now, I actually believe that $ABVX’s odds of success are higher than $NKTR’s were going into data, and I spend a ton of time attacking the existing $ABVX data from every possible angle in order to support this opinion. I’ll post the link to my research below. The next slide provides a rough outline of this thread. If you’re not going to follow/understand anything else from this entire pitch, make sure you check out “Slide 6” 😉

I’ve been open about being short $HIMS (so understand I am biased). At first this was mostly a counter-momentum short during the short squeeze over $70. However, since then, it has become clear to me that the company is being led into serious legal trouble with apparent reckless abandon.

I’m not a lawyer, but as a biotech investor I do have a better understanding of pharma IP than the “average” person, as well as a better understanding of physician liability as a doctor myself. However, frankly, you really don’t need legal experience to understand why parts of the $HIMS strategy *cannot* not be allowed. If bulls can take of their rose-tinted glasses at least momentarily and actually consider the points I’ll make here, I think basic common sense would suffice to arrive at many of the same conclusions I have.

tl;dr summary of points:

➡️The personalized semaglutide scam being committed at scale would kill pharmaceutical IP, leading to the end of new drug development (yes, I'm serious). HIMS is on a one-way train to getting their assess sued off for this.

➡️Physicians who take part in the personalized dosing scam should be aware that they are opening *themselves* up to huge legal liability in so doing.

➡️HIMS CEO is making bold statements about the efficacy of the oral weight loss “solution” that go against medical evidence. The company is at *high* risk of the FDA taking legal action on this false advertising.

➡️The $HIMS super bowl ad also skirted drug advertising laws, and litigation for this appears likely to me as well. Oh, and the blurred out images of Ozempic that they included in the commercial will bring $NVO lawyers knocking at their door as well.

➡️The company employs unscrupulous and dangerous prescribing behaviors by pushing medications without appropriate medical review (as reviewed in a recent WSJ article)

All of this translates to an untrustworthy company. Do you really want to take their word for how bullish their setup is *while their leadership is constantly dumping shares on the open market*?

The "personalized" semaglutide dosing scam.

$HIMS *cannot* be allowed to sell “personalized” semaglutide at scale. The company has doubled & tripled down on this idea both on the recent earnings call and on the Hims House podcast last week. The thought is that the company can make “personalized” (i.e. non-commercially available) doses of semaglutide through a 503A compounding pharmacy loophole that allows special doses to be made for patients in rare situations where, for some abnormal reason, the standard dosing will not work for them.

People must understand that exploiting this loophole “at scale” like $HIMS is trying to do WOULD MEAN THE END OF PHARMACEUTICAL INTELLECTUAL PROPERTY.

If a generic drug company like $HIMS can simply slightly modify dosing or formulation of an on-patent drug and suddenly be allowed to reap substantial profit from something that a pharma company discovered, developed, and owns, *what would stop generic drug companies from doing this with EVERY patented drug in the world?* There would be nothing to stop generic/compounding companies from stealing the intellectual property of every drug on the market by simply dose-modifying or adding inert compounds to the formula.

$HIMS manipulating the 503A specialized dosing rule may seem innocuous at first - “So what, some people will get some cheap Ozempic and $NVO will lose some money.” But if you actually consider the implications of this precedent even for a moment, it is clear that this scheme could be applied to *any* patented drug. Suddenly pharmaceutical IP is meaningless, and now there is no longer *any* financial protection/incentive for discovering new drugs. New drug development stops.

IMO, it is not at all a stretch to see how the first domino of $HIMS mass-selling “personalized” doses of semaglutide leads to others doing the same thing with other patented drugs, which leads to the end of the pharmaceutical industry and new drug development as we know it.

“Oh come on Adam, that will never happen”. Correct. It will not happen because $HIMS will NOT be allowed to get away with this. The 503A specialized dose “loophole” exists for RARE exceptions in order to help patients who would be at risk of serious harm (example - a small child with a cancer that is treated by a drug that has so far only been approved in adults. They need a much smaller dose than what is available, so 503A allows a compounding pharmacy to legally help this child with a non-commercially available dose).

The 503A specialized dose “loophole” does NOT exist so that $HIMS and other generic drug leeches can steal Novo Nordisk’s intellectual property and make their own c-suite rich by selling stock. If the company actually goes through exploiting this well-intentioned rule in that way, they will be stopped. They will be stopped because they *MUST* be stopped if we are going to preserve the system for developing new drugs.

The idea that $HIMS will actually be able to get away with this is ludicrous, and the CEO repeatedly telling his retail investors that it's not going to be a problem MASSIVELY undermines his credibility and trustworthiness in my book. When he reassures us about something that is so obviously wrong/not going to work, why would we believe him about anything else?

Nov 7, 2024 • 14 tweets • 13 min read

I have never pinned anything on X, but I am going to keep this thread calling out $CGEM as being undervalued pinned for a while, because I am feeling pretty confident about it. I want to call my shot on this one. The thread isn't short, but I hope it does a good job of documenting the general basis for what I think is a significant mispricing of Cullinan.

In the $15s right now, the market cap is under a billion, and the EV is <$200M with their surprisingly strong balance sheet.

Maybe there is some value in their oncology assets (they did get some good $ for half of zipalertinib ownership), but personally I am writing those off completely and focusing on CLN-978, their CD3xCD19 T-Cell Engager for I&I.

Part 1: The Foundational Data.

The CD19 I&I hype really started with a small cohort of patients from Georg Schett. This showed impressive efficacy of CD-19 CAR-T in 15 patients with Lupus, Inflammatory Myositis, and Systemic Sclerosis.

The most impressive data was from the Lupus patients, who universally went from severe disease that was refractory to essentially all available treatments to having no disease activity and no need for continuing medications after the CAR-T infusion.

This got a lot of people excited, as it looks like some patients have been *cured* of their lupus. Given how severe their disease was and how poor the standard of care is even for less severe cases of Lupus, these results were truly remarkable.

Since then, several other small studies of CD19 CAR-T in multiple different I&I conditions have been published showing similar, sometimes curative-appearing results (won't discuss all of these for the sake of brevity, but there's a lot going on in this space).

Lymphoconditioning is in absolutely no way a rate-limiter to the widespread and early-line adoption of cell therapies.

I get that chemotherapy lymphodepletion isn't sunshine and roses, but treating it like this is some huge hurdle for cell therapy to overcome is ignoring the backbone of how we have treated hematologic malignancies for the last half century.

CHEMOTHERAPY.

Dec 9, 2021 • 7 tweets • 2 min read

Cell Tx Soap Box 1:

What leg is the "Targeted NK cells can't generate durable responses" argument left standing on?

At this point, that argument looks like an assumption based entirely on preclinical assays or historical clinical data of non-targeted allo-NKs.

What is the point of preclinical assumptions when we have a growing body of CLINICAL data to guide our thinking?

We now have 3 strong examples of durable responses using targeted NK cells, with 3 different targets, in 3 different indications.