My broad thoughts on BTCTC's, preferred stock potential (bullish and bearish take), equilibrium mNAV etc. 👇🧵

1/12 The severe mNAV compression across the board has occurred much sooner than I expected. I've viewed this as inevitable long term, but the 5,10,20 mNAV stocks which have compressed to 1.x in a few months has been a shock. If I had a perfect understanding of these stocks, I would have seen it coming, but that didn't happen. The best I know how to do is learn from it and bake that into my understanding.

Jul 4, 2025 • 8 tweets • 8 min read

Sorry, but remember my cube concept?

X- Bitcoin price change changes the stocks price by the same amount assuming mNAV and btc/share stay the same.

Y- mNAV change affects price the same way, assuming Bitcoin price and btc/share stay the same.

Z- BTC/share change affects price as a simple ratio as well assuming Bitcoin price and mNAV stay the same.

All of this being said, graphs below are cute, but please rationalize them with not just the potential change in Bitcoin price. In order to perform differently relative to Bitcoin, it’s now the area of a 2D surface stretching or compressing with one axis being mNAV change from today (or your baseline) and the other axis being BTC/share change. So, if you expect mNAV to stay flat and BTC/share to 10x its current amount (impossible for Strategy who holds 3% of all Bitcoin and would require holding 30% with zero share dilution in order to 10x btc/share), but if that’s still the naive expectation, that would allow a max outperformance from here of 10x in Bitcoin terms.

“But what about stock buy backs or earning yield in fiat instead of Bitcoin?” As Bitcoin price appreciates (not talking 50% but 1,000%… 10k% and so on) and a companies stack gets larger, yield and the power of buybacks will shrink. Expected double digit % outperformance of Bitcoin will be a thing of the past in coming decades once geo markets are saturated. That’s why now is such a critical time for investors to research and see if anything is worthy of their conviction.

“But mNAV is uncapped if they just stop selling shares on common. Plus, it’s kinda like PE ratio”. Sorry, not uncapped. I disagree with lots of people in this space here, but I’ll try to explain why. Most companies don’t go around selling common shares to the market very often. So why is their price capped? Because they’re unfortunate enough to hold fiat instead of Bitcoin on their balance sheet? Give me a break 😅. Look, we all know Bitcoin will outperform fiat long term, but it is the Bitcoin per share yield which provides tangible outperformance of the underlying. You think MSTR can reach 5% of all Bitcoin (holding 1.05 million of those puppies?). Great, I do too. So, once they do, if their mNAV hit 20 they would have a market cap equivalent to the value of all 21 million bitcoin. If you still think that’s a rational and even likely outcome, consider why investors would bid it up so high. The goal and potential of MSTR and others to outperform Bitcoin has to be quantified in BTC/Share. Otherwise it’s similar to a Bitcoin ETF. Is IBIT trading at a premium because it holds 600k (or whatever amount) Bitcoin? Nope. Why? Sure, by design, but don’t fall back on it not being an operating company etc. the differentiator is yield. If Saylor stopped providing yield.. decided they have enough Bitcoin and they’ll just squat on it, you think mNAV of 1 isn’t the general result? We’ve seen mNAV below 1 (where they certainly weren’t selling new shares to the market).

“But Climb, that was during a bear market”. Ok, so every bull market MSTRs mNAV can go unchecked to 100 and we will just drop 90-99% or so during bear markets?

“But Climb, there won’t be any more bear markets”. Sirs and ladies, can humans still leverage and overextend themselves? Is margin trading still possible? Is individual collateralized debt still possible? Yes. Human greed makes pops and flops of volatile sectors a “when not if” phenomenon.

Want a short thread of things which will keep mNAV from hitting 100 for anything that has more than a handful of Bitcoin and is trading on hope with extremely low marketcap anyway? 🧵 👇

1/7. Competition. We see it now with smaller holding, faster growing companies earning a higher mNAV vs MSTR. New/small companies will trade based on market trust/bet of future yield with the amount and speed of that yield being most important. People stopped trusting Semler’s execution and are confused by the medical business, and as there’s much better executing companies out there, Semler turned geriatric. Willingness to sell common shares to the market at low 1.xx mNAV doesn’t help.

Jun 27, 2025 • 11 tweets • 4 min read

Metaplanet may become the 2nd largest company in the world, second only to Strategy. Issuing perpetual preferred stock is the huge unlock for Metaplanet, and I speculate this will be announced to be voted on during the Sept 1st shareholder meeting. 🧵👇

1/10 Simon, Dylan, Shinpei and even Saylor on stage at Prague have all been talking about preferred stock for Metaplanet a LOT lately. They recently announced an extraordinary meeting of shareholders Sept 1, and as preferreds would require shareholder approval, I see this as very likely an agenda item.

Jun 7, 2025 • 24 tweets • 8 min read

Here are the final 21 out of 42 reasons I am a Metaplanet investor and absolutely love this company. I'll no longer be on the MPM podcast, but will continue sharing as much as possible. 🧵👇

1-21. Here are the first 21 reasons broken down if you missed them:

The first 21 of 42 reasons I love Metaplanet $MTPLF from Metaplanet Madness Ep 4 (link in comments if you missed it). @BTCBullRider also explored his concept of Cultural Torque which I recommend watching. 🧵👇

1. Simon & Dylan. These gentlemen have been transparent, consistent, and each have a few fantastic interviews on YouTube such as this one.

May 17, 2025 • 6 tweets • 2 min read

Below are charts from my model as well as the link to Metaplanet Madness Ep 2 for anyone who missed it live earlier. 🧵👇

1/8 All of these charts are interconnected, and I tried to look at the past and be as conservative (even on the bull case) as possible. So, this isn't my personal view, this is what I believe to be very handicapped bull/base/bear cases. Less % dilution every month for the next 24 months is part of that. Historically, 10% or more has been the norm.

May 13, 2025 • 9 tweets • 2 min read

What is life/vitality for Bitcoin Treasury Companies? Why will some manage to generate higher yield and accumulate Bitcoin much faster than others of the same size? Who decides the winners? Why will it be Metaplanet? A short 🧵👇

1/8 Strong mNAV: I don't mean it's just strong today. For me to trust that the accretive dilution machine can keep churning, I want to see a healthy range historically. Makes accretive dilution MUCH more efficient. MetaPlanet has that.

May 10, 2025 • 11 tweets • 4 min read

Expected about 500 live viewers for Metaplanet Madness Episode 1 and I hear it went over 5,000?! Wowzer! Here's a thread to consolidate some of my charts from the episode. 🧵👇

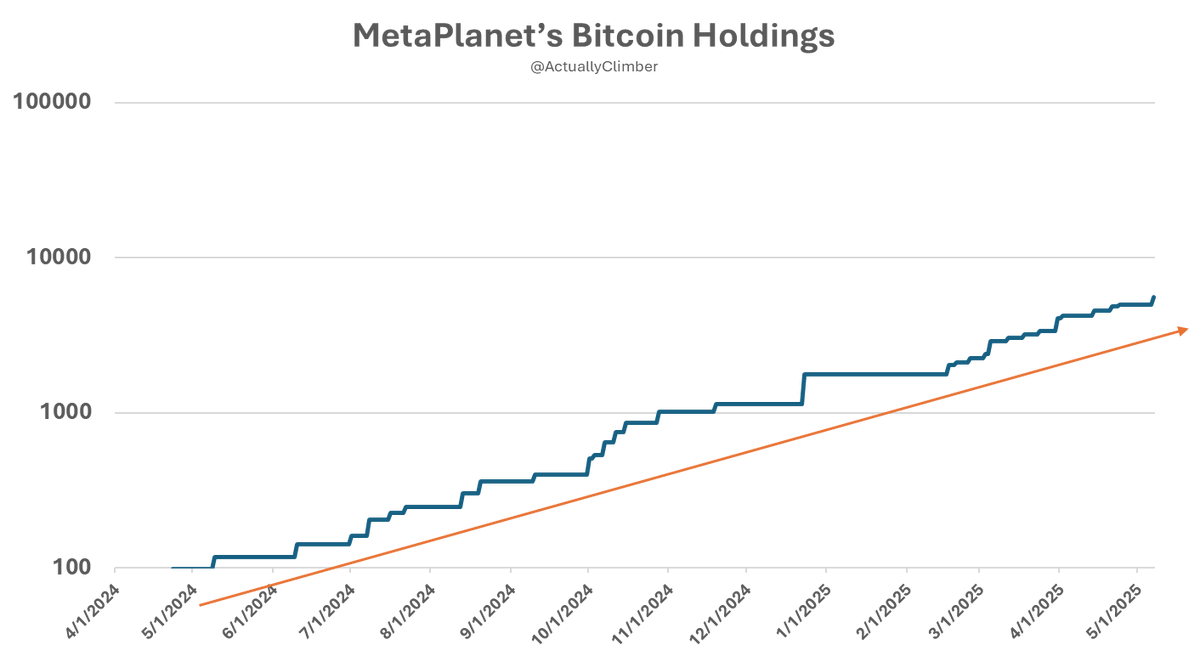

1/10 Metaplanet's bitcoin accumulation has seen exponential growth. This will certainly slow, but I believe gradually. They spent 188 days between around 100 and 1000 bitcoin. I believe they'll spend 261 days between 1000 and 10000. So, my estimation is 10k bitcoin July 16th 2025.

May 1, 2025 • 14 tweets • 5 min read

People wonder why I've shifted from $MSTR to MetaPlanet $MTPLF. MSTR is fantastic and will continue to outperform BTC. I'll continue sharing my viewpoints and encourage readers to have a questioning attitude and make your own decisions. I've made mine. Bookmark this🧵👇:

1/13. Fair or not, what are the two gripes you've heard the most over the past 6 months with $MSTR? "Is Saylor hitting the ATM/How much?" and "Proof of reserves?" MetaPlanet $MTPLF gives Proof as well as showing complete transparency in recent ATM's down to specific days.

Apr 29, 2025 • 9 tweets • 3 min read

Interested in a crash course/resources on MetaPlanet ($3350.T in Japan, $MTPLF in the US)? I'll share some excellent resources in this bookmark worthy 🧵👇. Please do your own research:

Some of my takeaways: 1. Faster Bitcoin and BTC/Share growth than their competition. 2. Huge tax advantages in Japan vs holding Bitcoin with a strong retail holder base. 3. Their mNAV got carried away at 9x but is currently around 2.4x (about the same as $MSTR). 4. They use ~5% of cash to sell puts on Bitcoin, earning interest on short term options or getting a discount on buying Bitcoin, winning either way which makes them stronger in sideways or down markets. 5. With @gerovich and @DylanLeClair_ at the helm, focus and execution are unquestioned. 6. They're a Bitcoin pureplay, only holding 1 hotel from their legacy business which is becoming a Bitcoin focused landmark. 7. They still are tiny (~$1 Billion Marketcap) with huge growth potential, currently holding 1% as much Bitcoin as MSTR. I think they'll hit 2% as much as MSTR within 12 months. 8. They have a fairly new OTC ticker in the US ($MTPLF) with growing volume as the company becomes more well-known. 9. They were the best performing stock in Japan in 2024. 10. Disclaimer, I am a shareholder and view this as my next 10x.

Now for the 🧵👇:

1/8. MetaPlanet's Director of Bitcoin Strategy @DylanLeClair_ recently shared this research report which I highly recommend:

I've been asked to share my typical process for selecting when to buy or sell a stock or option. I promise there's nothing revolutionary here. I try to keep things as simple as possible. I'll touch on #MSTR throughout. 🧵👇

1/8. High Personal Conviction. Over the years I've had very high clarity & conviction about a short list of investments. Bitcoin starting in 2016. Tesla starting in 2017 and becoming very strong in early 2019. MSTR in December of 2022. Similar to Saylor talking about deciding to buy Bitcoin and then worrying that others with deep pockets would figure it out before he achieved a sizable position. This is internal, legitimate FOMO, not external, from other people's excitement (such as the GameStop craze). This applies to stock and longer-term options.

Oct 30, 2024 • 10 tweets • 2 min read

My favorite bullish takeaways from this #MSTR earnings call. It was fantastic!! 🧵👇

1. $42 Billion (over 3 years) total capital raised to buy Bitcoin. $21 Billion will be from share issuance (accretive dilution as BTC/share increases). 21 Billion of bonds. So much more transparency, even breaking down a yearly plan for 2025,26,27.

Oct 23, 2024 • 14 tweets • 2 min read

$MSTR has an impressive list of benefits over owning #Bitcoin ETFs. Have I listed any you haven’t considered? What should I add to the list?

Let’s explore 🧵👇:

1. ETFs charge a management fee. MSTR does not. While ETF fees can be small ~0.2%/year, this is an important drawback for long term investors.

Oct 21, 2024 • 20 tweets • 4 min read

I strongly believe that #MSTR will end up with much more than 2% of all Bitcoin. Here’s why: 🧵👇:

MSTR currently owns 252,220 #Bitcoin or 1.2% of the 21,000,000 that will ever exist. 2 years ago, people doubted they’d ever exceed the 1% mark. Now the doubters have moved the goalpost to 2%.

1. As we’ve seen this year, with the increase of mNAV premium (now around 2.3), MSTR overshot their goal of achieving 4-8% Bitcoin yield (increase in BTC/Share). So far they are around 18% and the year isn’t over.

Oct 18, 2024 • 12 tweets • 3 min read

$MSTR mNAV may go a lot higher than people expect. Here's how, and why I'm so much more bullish on MSTR both short and long term. These are just my thoughts. Please do your own research and make your own decisions.

A few weeks ago, with the bull market likely about to kick off, I figured I'd load up on more MSTR in order to ride the wave for the next year or so as gamma squeezes, short squeezes and FOMO enter the market. I figured that mNAV would go up during the bull market, but probably not in a sustainable way. I think I was wrong. I now can't stop buying more shares and currently own over 20,000 as well as some late 2025 leaps. Here are my reasons:🧵👇

1. Microstrategy's yield potential IMPROVES with higher mNAV, incentivizing shareholders to buy and enjoy holding even at higher mNAV. Imagine an mNAV of 10 which only requires a 1% share dilution to increase Bitcoin holdings by 10%! Microstrategy will eventually hold much more than 2% of all Bitcoin (higher mNAV incentives will help make this possible).