$IREN Q1 (FYQ3) Full Breakdown & Analysis (Deep Dive)

In this post, I’ll cover everything new revealed in $IREN's recent Q1 earnings presentation (+ the follow-up CEO interview) and provide some much-needed context and insights.

🧵

$IREN Q1: Financial Results 💸 (1/4)

IREN once again proved to be the most profitable entity in the $BTC mining space.

In fact, it was the only “Bitcoin miner” to post a profitable quarter — now for the second quarter in a row, excluding FASB gains/losses (BTC price fluctuations on the balance sheet).

$IREN posted impressive 16.3% net margins for the quarter — a new all-time high.

Net margins below 20% may not seem remarkable at first glance, but achieving consistent profitability this early in the company’s lifecycle is genuinely impressive.

People forget that $IREN is still a relatively young company, founded in November 2018. Reaching profitability this quickly, while in hyper-growth mode, is not a given.

It’s also great to see $IREN's top-line growth firmly in the triple digits — posting a 172.7% YoY revenue increase. As expected, thanks to expanding margins, $IREN's bottom line grew even faster, with net profit after tax (NPAT) up 181.4% YoY.

This increase in profitability is primarily the result of:

→ operating leverage ✅

→ reduced average electricity costs ✅

The company’s “Other Costs”, which mostly consist of SG&A and site-level operating expenses, declined relative to revenue from 23.76% to 17.08% on a YoY basis.

This suggests $IREN is scaling without proportionally increasing its core operating overhead — a textbook case of positive operating leverage.

This effect is enabled by IREN's "giga-site" strategy.

Instead of operating a fragmented portfolio of smaller data center sites, most of IREN's compute capacity is concentrated at one massive 750 MW data center site in Childress.

This consolidation allows $IREN to centralize staffing, infrastructure, and support functions (such as maintenance), driving down operational overhead per MW — which enables operating leverage and supports more efficient growth as capacity ramps.

I expect this trend to accelerate over the coming quarters as the company expands its Bitcoin mining operations by another 66% (from 30 EH in Q1 to 50 EH by June).

This will act as a strong tailwind for net margins going forward. 📈

Likewise, IREN's focus on expanding its Childress site will bring further relative cost savings in electricity rates.

Childress, located in West-Texas, has some of the cheapest electricity in the country — often below $3c per kWh — significantly lower than the industry average of over $4c per kWh.

As of Q1, about 2/3 of $IREN's operations were located at Childress, while the remaining 1/3 were at the company’s Canadian sites in British Columbia.

The Canadian sites consistently report electricity costs in the mid-$4c range — roughly 50% higher than its Texas operations, though still in line with the broader industry average.

Once $IREN scales to 50 EH by June, its Texas operations will make up ~80% of its total capacity — implying even further relative cost savings going forward.

On top of that, Co-CEO @danroberts0101 mentioned in a recent interview with @McnallieM that IREN has made notable progress over the past 6–8 weeks in fine-tuning its power strategy at the Texas site.

He highlighted that $IREN has a team of data analysts dedicated to optimizing its curtailment strategy — which, over the past 2 months, resulted in industry-leading power costs of just $2.5c in March and $2.9c in April.

Looking ahead, he expressed optimism that IREN could potentially match — if not beat — those results, given the ongoing progress of the analytics team.

Considering the summer period typically brings the highest power costs of the year in Texas, anything below $3c / kWh during this time would be incredibly impressive. ✅

Hence, as $IREN scales from 40 EH to 50 EH over the next weeks, it should realize further cost-efficiency gains due to continued operating leverage and lower electricity costs.

Combined, these 2 factors will act as strong tailwinds for net margins going forward.

Addressing Skepticism: 👇

Some skeptics might read all of this and assume I’m vastly exaggerating IREN's cost discipline — arguing that the real reason for its margin expansion is simply the fact that $BTC trades significantly higher than a year ago.

After all, in last year’s Q1, Bitcoin's price averaged in the mid ~$50K range, while this year’s Q1 saw average $BTC prices around ~$90K.

If BTC prices are up ~80% YoY, wouldn’t that explain IREN's increase in profitability?

Well — it actually doesn’t. ❌

Ironically, while the BTC price has increased substantially over the past year, mining conditions have materially worsened over the same period.

For one, April last year marked the most recent $BTC halving, which cut block rewards from 6.25 to 3.125 BTC — effectively halving miner revenues overnight. Despite an ~80% increase in BTC price since then, it still hasn’t fully offset the revenue impact of the halving.

As if that weren’t enough, network difficulty also increased by approximately 40% YoY.

To put that in perspective: a 40% increase in difficulty results in a ~28.6% reduction in revenue per unit of BTC mining compute (EH).

All in all, despite BTC prices rallying significantly over the past year, mining conditions — i.e., revenue potential per EH — have actually declined by roughly 36%. 📉

This is precisely why no other mining company besides $IREN has posted positive operating income over the past year.

In fact, the state of the industry is so poor that IREN's Co-CEO recently stated that he hopes profitability among competitors improves — acknowledging that it’s currently a bad look for the sector.

Dan Roberts also noted that break-even times on ASICs (mining hardware) are nearing all-time highs, approaching 2 years, further underscoring the current economic strain on the mining industry.

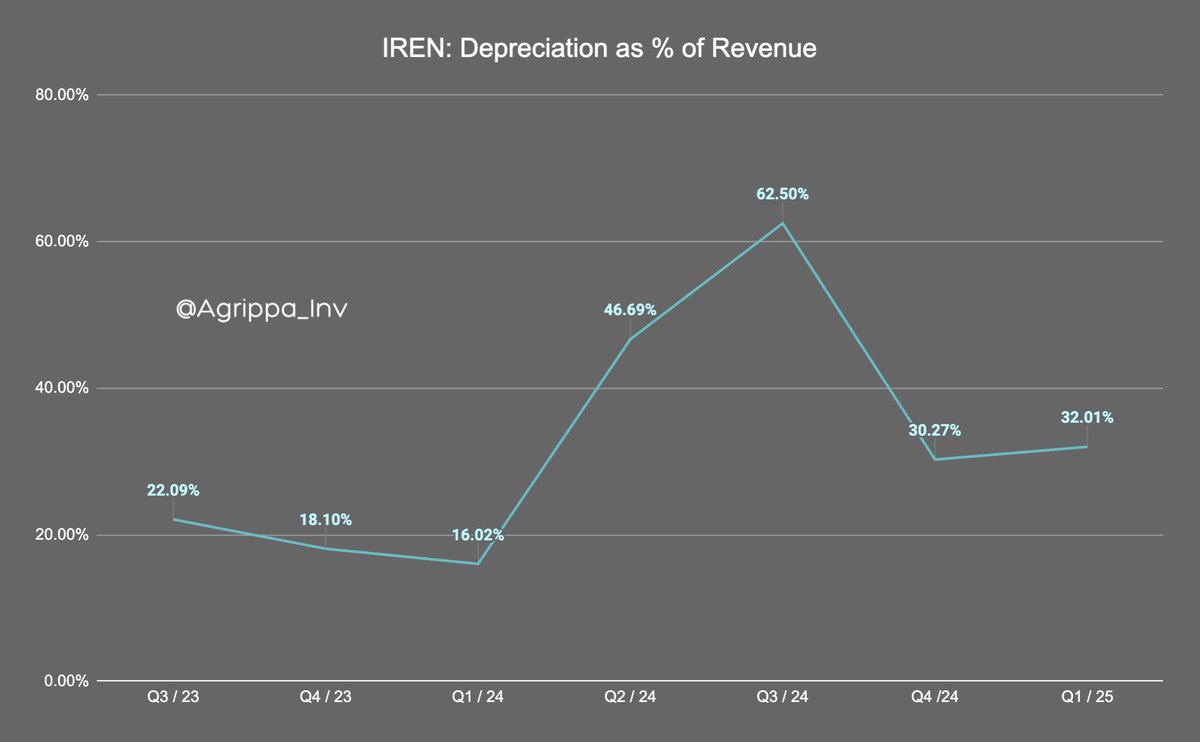

Another straightforward indicator that mining conditions have worsened is this: 👇

Depreciation expense as a percentage of revenue has increased, not decreased.

If mining conditions had actually improved, you’d expect each ASIC to generate more revenue per unit of depreciation — not less.

I encourage you to compare this chart to the previous one. While both electricity costs and “Other Costs” decreased, depreciation clearly rose as a percentage of revenue.

If mining conditions had improved — meaning higher revenue per mining rig or per EH — you’d expect: 👇

Revenue ↑ faster than depreciation → depreciation as a % of revenue ↓

But instead, we see the opposite: depreciation as a % of revenue increased. ❌

This makes $IREN's net margin expansion even more impressive.

The company improved margins despite these industry-wide headwinds, driven primarily by disciplined cost management and the operating leverage enabled by its giga-site strategy.

My expectations going forward: 💬

As explained above, I expect further relative cost savings in electricity and “Other Costs” for the reasons already outlined. All else being equal, this alone should drive continued net margin expansion and, by extension, higher profitability.

However, layered on top of that, I also expect mining conditions — which have previously acted as a headwind to margins — to materially improve over the next couple of years, further boosting profitability.

The industry just experienced a halving event, meaning the next one won’t occur until 2028.

In the meantime, I expect BTC prices to vastly outperform network difficulty, leading to rising revenue per unit of compute ($/EH and $/MW).

Several of the largest operators — including $IREN, $MARA, and $RIOT — are in the process of pausing their fleet expansions, at least temporarily, while shifting focus toward AI/HPC. Even $CLSK, a pure-play miner, hasn’t guided for any additional expansion beyond the 50 EH milestone.

It’s clear that under current market conditions, expanding one’s mining fleet makes little economic sense. With most of the sector operating unprofitably, I expect this will lead to a significant slowdown in new mining compute coming online.

Over time, this will help improve mining conditions, since less new mining compute coming online directly limits network difficulty growth.

This industry-wide profitability tailwind could last for at least a year — and even beyond that, it’s unlikely mining conditions will deteriorate to current levels again until the next halving.

We are currently, quite literally, at all-time lows in terms of sector-wide mining profitability — especially for such an extended stretch. This explains why $BTC miners have underperformed so dramatically in public markets over the past year.

While nearly all miners will benefit from improving mining economics, $IREN's ongoing operating leverage and power cost optimization will cement its position as the most profitable operator in the space, further extending its lead. 🥇

Based on these factors, I believe IREN could potentially reach net margins >30% by year-end.

And since the company is also increasing its mining capacity by ~66% from Q1 to the end of Q2, I’m confident we’ll see quarterly net income (from mining alone) increase 3–4x by Q4 (if not more) implying potential quarterly profits of at least ~$75–100 million.

At a current market cap of just ~$1.9 billion, $IREN looks like an absolute steal on a valuation basis. 💸

Nov 13, 2024 • 13 tweets • 79 min read

$IREN - Complete A-Z investment case

In this post I’ll cover why I expect this hyper-growth stock to crack $150 over the next 18 months—representing a gain of 1150% from its current price of $12 📈

I went ‘All-In’ this stock, and for good reason….

🧵1) $IREN - Intro

I believe that $IREN is THE stock to hold over the coming years, as it is positioned at the center of the two strongest 'narratives' of this business cycle & bull market – AI and Bitcoin.

This small cap, with a market cap of just ~$2.3 billion, builds and operates data centers to support high-performance computing applications (HPC), such as $BTC mining and AI, leveraging cheap renewable energy sources.

@IREN was founded in the fall of 2018 by the Australian brothers Will & Dan Roberts (@danroberts0101) and went public in November 2021. Based in Sydney, the firm was established with a forward-looking vision to address the growing demand for computing power in an increasingly digitizing world. In its early stages, Iren strategically acquired land in Canada and the U.S., particularly in regions like British Columbia and Texas, where the increasing availability of renewable energy sources such as solar, hydro, and wind is steadily reducing industrial energy costs.

As Iren acquired most of its land before the recent AI boom, it's likely they purchased it for a fraction of what it would be worth today, potentially paying pennies on the dollar compared to current market values. This foresight has positioned them exceptionally well for future growth as demand for HPC and AI infrastructure increases and land with access to power becomes ever more scarce and valuable.

The company currently holds a very impressive land & power portfolio, consisting of infrastructure sites with grid-connected power capacity of >2.3 GW across the U.S. and Canada, with over 1 GW of additional capacity in the pipeline.

To put this into context, in 2023 the TOTAL global data center capacity was approximately 33 GW, according to a report from Citi Research.

However, a significant portion of Iren’s infrastructure portfolio remains undeveloped, with the company currently operating approximately 450 MW of data center capacity. Iren is actively scaling its operations, rapidly expanding its capacity by developing its land and constructing new data centers at a rapid pace of 50 MW per month.

By the end of the year, $IREN aims to reach 510 MW of available infrastructure, with the majority of this power dedicated to Bitcoin mining at a hash rate of 31 EH/s— positioning the company as one of the largest $BTC miners in the industry.

In case you are new to the Bitcoin mining sector, hash rate (measured in EH/s) is a measurement of computational power being used to mine Bitcoin. Generally speaking, the higher the hash rate, the more $BTC you mine. Since there is a predetermined number of $BTC being issued per “block” (every ~10 minutes), $BTC miners compete for this reward. The higher the hash rate, the higher the cut of that reward. This makes EH/s growth imperative for every miner.

Achieving the end-of-year target of 31 EH/s would set a new industry record for the fastest hash rate growth in a single year by a public BTC mining company, both in nominal and percentage terms. This would mark a leap from 5.64 EH/s in January 2024 to 31 EH/s by December 2024, representing a ~450% increase within just one year.

$IREN already holds the previous record for the fastest-growing Bitcoin miner in a single year, having increased its hash rate from 1.6 EH/s to 5.6 EH/s last year. This represented an impressive 250% growth rate. However, surpassing this record at such a larger scale would be unprecedented and truly groundbreaking in the industry. This company is quickly establishing itself as the fastest growing $BTC miner of all time with unparalleled growth rates, largely thanks to already owning high quality land on which it can rapidly build its data centers.

Given its fast growth, most of Iren’s mining fleet is equipped with the latest hardware this industry offers. This newer hardware translates into higher energy efficiency and, consequently, lower energy costs. As of today, Iren's fleet operates at an industry leading efficiency of 16 J/TH, which is significantly better than the industry average, which ranges in the low-to-mid 20s. By year-end, the company aims to achieve a fleet efficiency of just 15 J/TH, solidifying itself as the most profitable $BTC miner in the industry.

The company has also recently dipped its toes into the AI market, offering a small yet promising AI cloud service, which includes 816 $NVDA H100 GPUs and a recent acquisition of 1,080 H200 GPUs.

While $IREN continues to rapidly gain market share in the BTC mining space, the company is now leveraging this success to strategically position itself for emerging opportunities in the AI sector, aiming to monetize a significant portion of its expansive land and power portfolio in this growing segment.

May 20, 2024 • 8 tweets • 9 min read

$IREN's Q1 results - Deep Dive ⛏️

In this thread I’ll give my 2 cents on $IREN's recent Q1 earnings (reported as Q3).

I will cover:

👉 Mining Costs 💸

👉 EH/s Expansion Plans 📈

👉 AI Developments 🤖

👉 $500 mill ATM & new financing options 🏷

👉 New Price Target 🎯

Mining Costs 💸

$IREN is now clearly one of the most profitable $BTC miners, rivalling $CLSK in all-in cost per $BTC.

Note: I used net income figures from pure mining activities. For $IREN, I excluded the $4.7 mill of foreign exchange gains from the pre-tax net income figure & applied the same tax rate. For $CLSK, I did the same for the $119.7 mill in FASB gains (unrealized $BTC gains).

As we can see, $IREN's profitability is exceptional - coming very close to the lowest cost miner $CLSK.

However, keep in mind that these are pre-halving figures (Jan-March) & don’t reflect the current post-halving costs of either of the 2 miners. We’ll have to wait until Q2 to get post-halving data.

May 13, 2024 • 5 tweets • 6 min read

$IREN Investment Case - a 30x in the making 📈

I recently started a position in the #BTC miner & AI cloud hosting company $IREN - acquiring 27.5k shares at a price per share of ~$4.8.

In this post I explain why I'm so bullish on this rapidly growing company.

Part 1: Explosive hash rate growth 📈

Part 2: $IREN's DNA 🧬

Part 3: Price Target 🎯