Bold and unfiltered takes on trade, shipping, and commodities. Not investment advice.

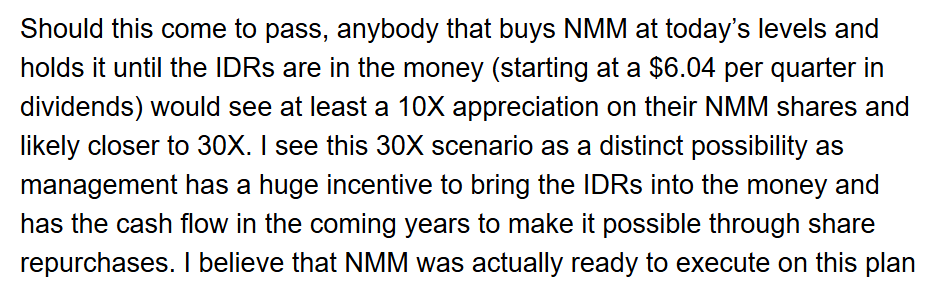

Where to start…

Where to start… 2/ I have been an unwavering $NMM, Tanker and Capesize drybulk bull ever since through some incredible volatility and so many doubters and so much disdain for this company and industry. I still have every last share of my huge tranche of <$4 cost basis shares I bought late 2020.

2/ I have been an unwavering $NMM, Tanker and Capesize drybulk bull ever since through some incredible volatility and so many doubters and so much disdain for this company and industry. I still have every last share of my huge tranche of <$4 cost basis shares I bought late 2020.

2/ Here are the ratios of non-Chinese fleet to US share of global trade to show how many times over US trade is covered for each segment by the non-Chinese fleet:

2/ Here are the ratios of non-Chinese fleet to US share of global trade to show how many times over US trade is covered for each segment by the non-Chinese fleet:

These sanctions actually DO work.

These sanctions actually DO work.

2/ Even though 71% of borrowers will still have a balance after $10k-$20k forgiveness or will not receive any forgiveness due to income, ALL eligible federal student loans currently remain in forbearance until this is resolved.

2/ Even though 71% of borrowers will still have a balance after $10k-$20k forgiveness or will not receive any forgiveness due to income, ALL eligible federal student loans currently remain in forbearance until this is resolved.

2/ TGA is the next easiest and totally calculable. ~$300B more of drawdowns (liquidity injections) due to debt ceiling then also tapped out.

2/ TGA is the next easiest and totally calculable. ~$300B more of drawdowns (liquidity injections) due to debt ceiling then also tapped out.