Emperor of @YetAnotherValue. Part time podcast host / blogger; Full time Cookie Monster.

This isn't a troll or anything. $AAN's is at ~3.5x EBITDA and buying back shares, and I do understand that RTO is a massive value add for consumers living paycheck to paycheck.

This isn't a troll or anything. $AAN's is at ~3.5x EBITDA and buying back shares, and I do understand that RTO is a massive value add for consumers living paycheck to paycheck.

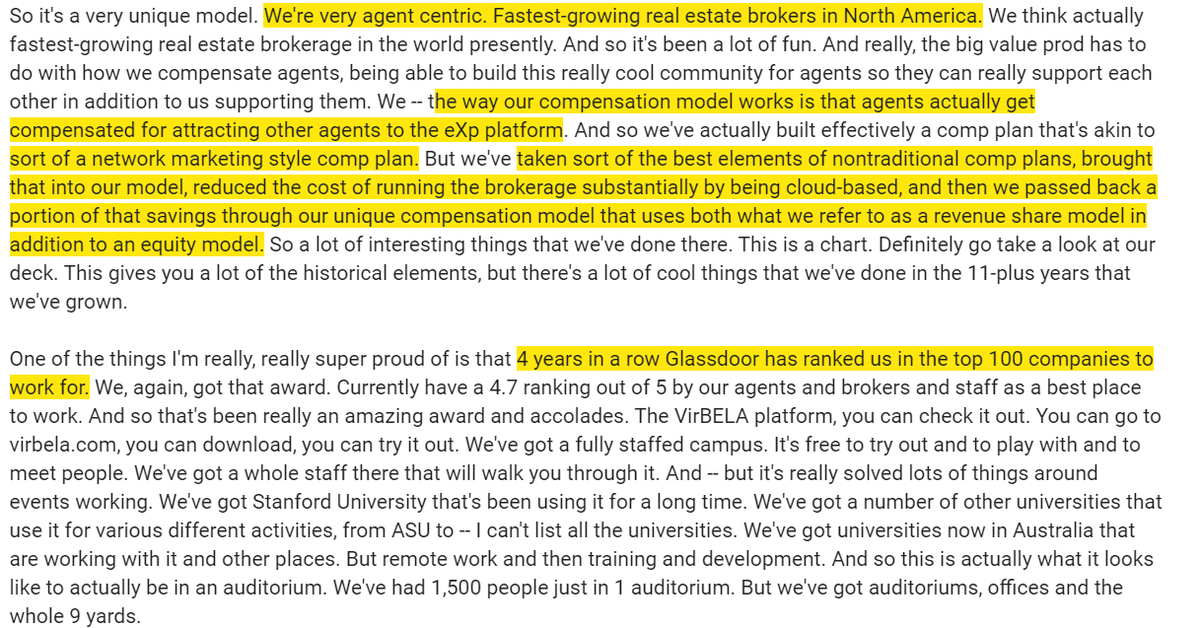

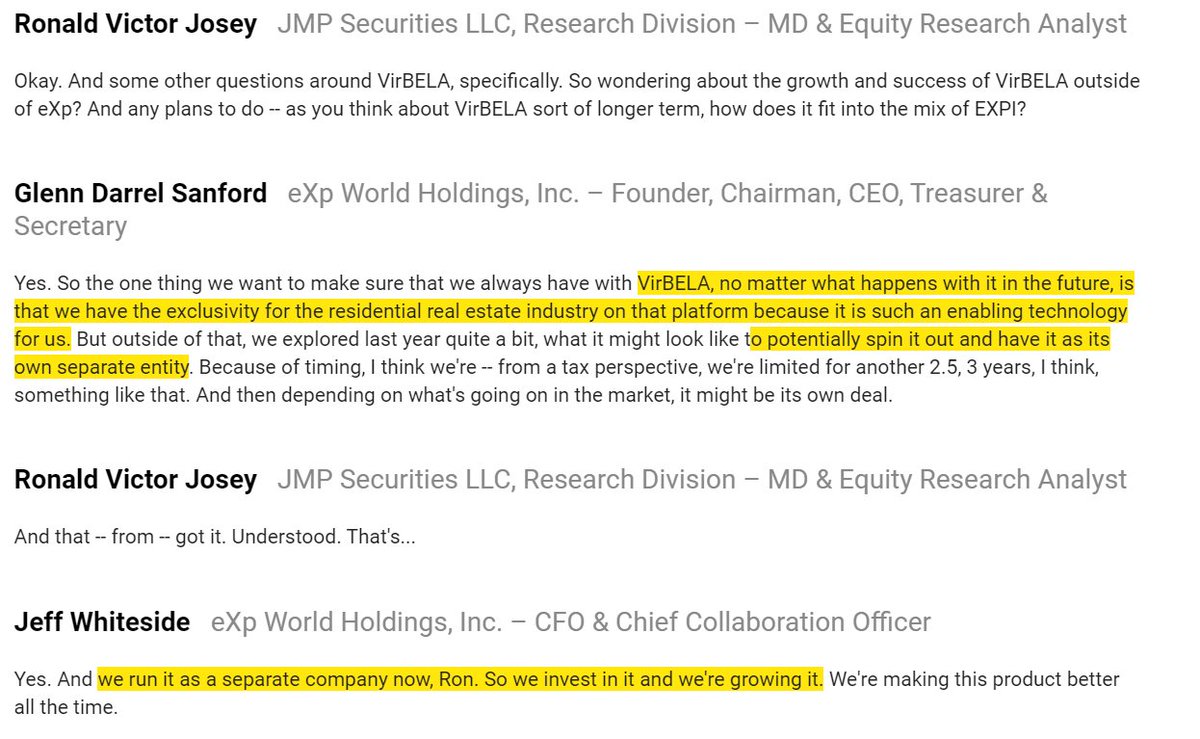

VirBELA also interests me. The stuff I see on their website (virbela.com) reminds me of the Sims from the early 2000s.... but it's a critical piece of their business and they might spin it at some point

VirBELA also interests me. The stuff I see on their website (virbela.com) reminds me of the Sims from the early 2000s.... but it's a critical piece of their business and they might spin it at some point

They may not pull off their flywheel, but this is what you want to here from a potential flywheel market place like : status quo not great + trying to make experience "radically" better + no one else is close to their scale

They may not pull off their flywheel, but this is what you want to here from a potential flywheel market place like : status quo not great + trying to make experience "radically" better + no one else is close to their scale