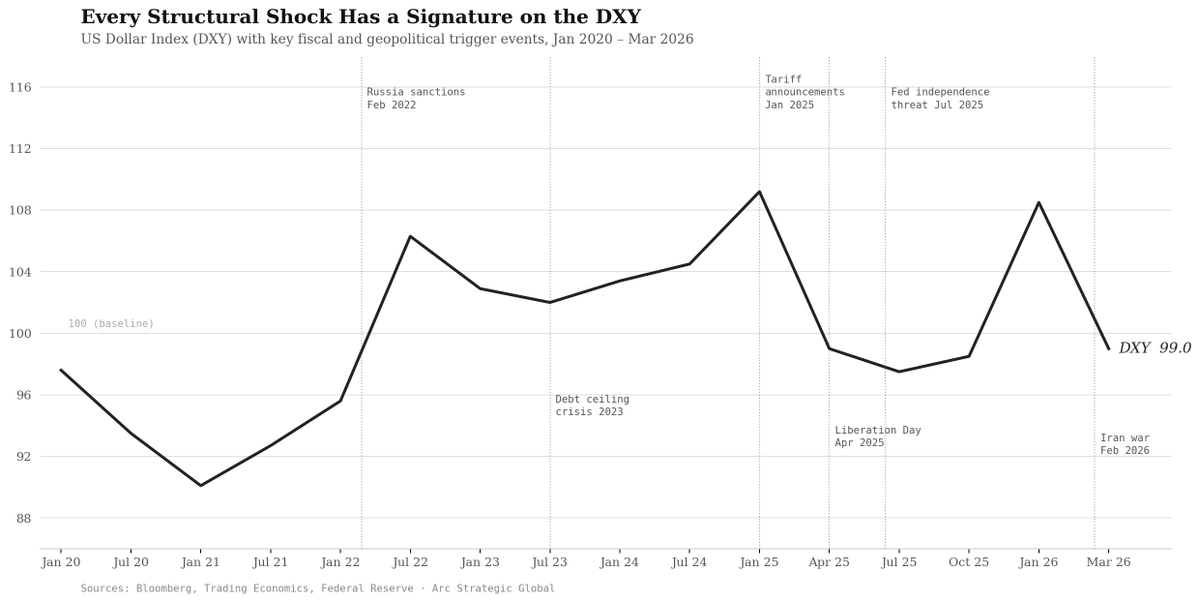

Tollbooth regimes & selective access in energy chokepoints | Hormuz

Probability frameworks over panic

Mar 24 • 6 tweets • 6 min read

1/6 THE PRICE OF AMERICAN MONEY IS CHANGING. EVERYTHING DOWNSTREAM ADJUSTS.

How rising yields are repricing the world, from US mortgages to African debt

On March 20, a 30-year US Treasury bond sold at a yield of 4.96%. On the same day, the average American trying to buy a home was looking at a 30-year mortgage rate of 6.44%. Those two numbers are connected by a chain of logic that runs all the way to Nairobi, Islamabad, and Ankara, and most of the people at the end of that chain have no idea they are in it.

This is what rising bond yields actually do to the world.

The mechanism nobody explains

When bond prices fall, yields rise. When yields rise, the government has to pay more to borrow. When the government pays more to borrow, every other borrower in the economy, bank, company, homebuyer, also pays more, because US Treasuries set the floor under the entire global cost of money.

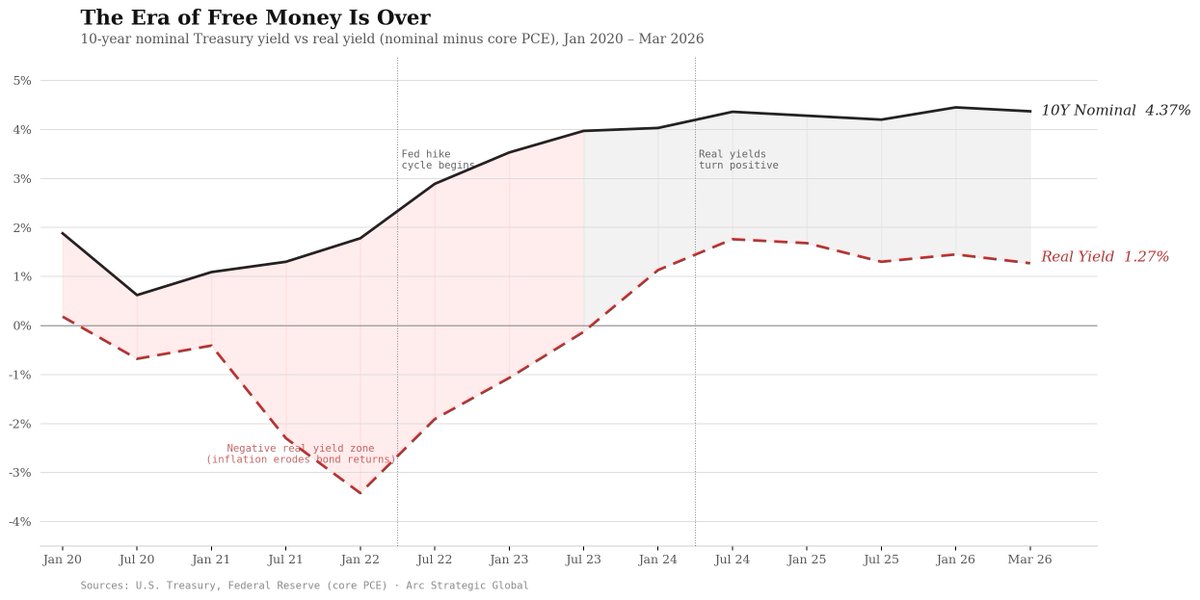

The 10-year Treasury yield is now above 4.2%, holding near its highest level since August. The 30-year bond touched 4.96%. Core PCE inflation accelerated to 3.1% in January, and that data predates the Iran war's energy spike entirely. The numbers that come next will be worse.

Government bonds, normally a refuge during geopolitical shocks, have joined the equity sell-off this time. When inflation is the problem, bonds do not provide shelter. The shock is transmitting through energy prices, not demand collapse.2/6 America: the floor is moving

The 30-year fixed-rate mortgage averaged 6.33% as of March 19, with a dual surge in benchmark yields and risk premiums having eliminated nearly all room for downward movement. On a $400,000 loan, the difference between today's rate and the 3% era of 2021 costs a family roughly $850 more every single month. That is not a statistic. It is a car payment that disappears from the economy, every month, for 30 years.

Bright MLS chief economist Lisa Sturtevant put the stakes plainly: if the Iran conflict prolongs, the result may be not just a delay in the spring homebuying season, but a broader shift in the trajectory of a housing market that had been expected to rebound in 2026.

The federal government faces the same arithmetic. FY2025 ran a $1.8 trillion deficit. Every rollover of existing debt now locks in higher rates. The interest burden does not disappear when oil prices ease. It compounds. The OECD projects debt-to-GDP rising from 83% to 85% in 2026 as global sovereign borrowing hits a projected $29 trillion.