Market indiscriminately selling financials, but impact of potential recession mostly neutral for BFF, if not positive. Economic instability increases demand for BFF’s factoring services, as businesses offload invoices to improve cash flow.

Market indiscriminately selling financials, but impact of potential recession mostly neutral for BFF, if not positive. Economic instability increases demand for BFF’s factoring services, as businesses offload invoices to improve cash flow.

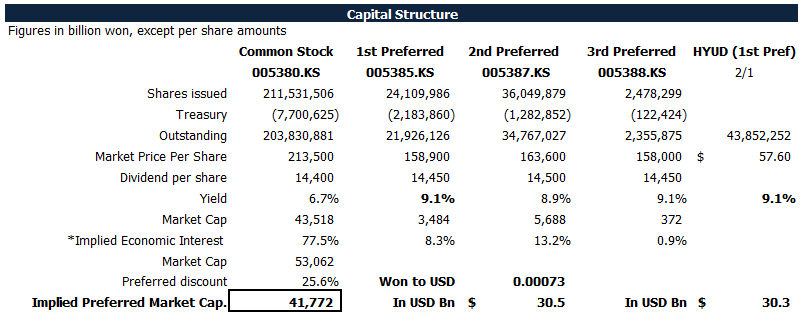

Hyundai prefs have no voting rights, but are legally entitled to divvys equal to common plus a premium. Unlike US preferreds, Korean preference shares have no fixed divvy or maturity--they fully participate in divvy growth of issuer, making them comparable to non-voting common.

Hyundai prefs have no voting rights, but are legally entitled to divvys equal to common plus a premium. Unlike US preferreds, Korean preference shares have no fixed divvy or maturity--they fully participate in divvy growth of issuer, making them comparable to non-voting common.

Diving in (follow closely): PAH3 directly owns 53.3% of the ordinary shares of VW and 1.3% of its prefs, which equates to control position w/a 31.9% economic interest. VW, in turn, owns 75% of the ordinary shares of Porsche AG and 75.8% of its prefs.

Diving in (follow closely): PAH3 directly owns 53.3% of the ordinary shares of VW and 1.3% of its prefs, which equates to control position w/a 31.9% economic interest. VW, in turn, owns 75% of the ordinary shares of Porsche AG and 75.8% of its prefs.

Operates a banking-as-a-service business that generates fee income w/ high levels of noninterest bearing deposits (96% of total). Partners w/ companies that want to instantly disburse funds—think corp disbursements, insurance claim payouts, tax rebates, early wage access, etc.

Operates a banking-as-a-service business that generates fee income w/ high levels of noninterest bearing deposits (96% of total). Partners w/ companies that want to instantly disburse funds—think corp disbursements, insurance claim payouts, tax rebates, early wage access, etc.

36% dom. market share on total assets, 39% loans, and 40% deposits. Given relatively small size of addressable market (pop. of 4mil with unique language), company has won the penetration game and now operates in a disciplined duopoly w/TBC.

36% dom. market share on total assets, 39% loans, and 40% deposits. Given relatively small size of addressable market (pop. of 4mil with unique language), company has won the penetration game and now operates in a disciplined duopoly w/TBC.