Retiring Investment Manager sharing their 10x10x10=1000 methodology

Mar 6 • 4 tweets • 1 min read

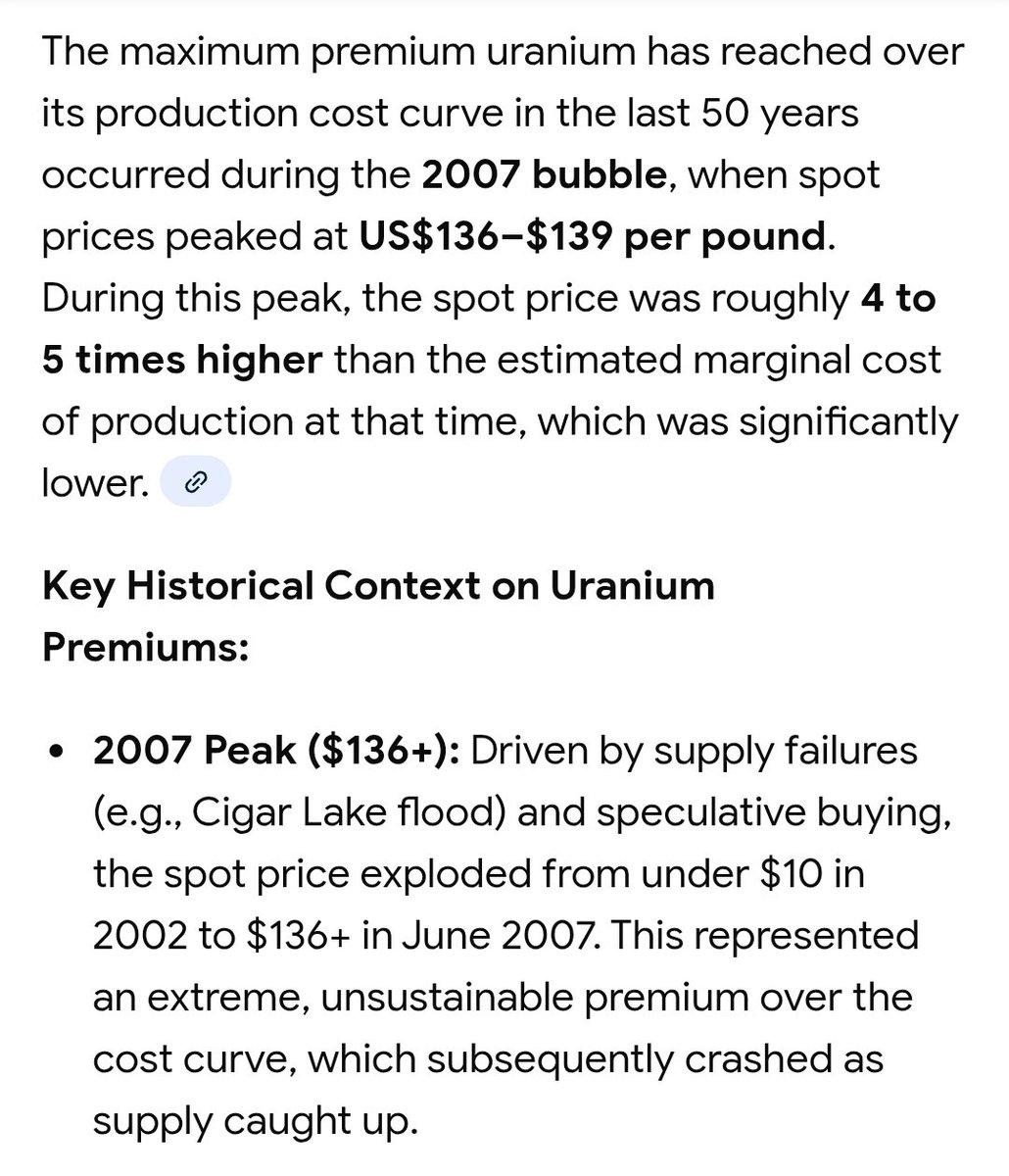

.....using > 5x cost curve assumptions on NPVs or mid term cashflow will generally let you down, don't use above 2x cost curve as an average assumption to ground you for the down cycle. #commodities

Note a <1x PE stock on near peak cycle spot (>5x cost curve) is > 20x PE at cycle lows (or negative if not a lowest quartile producer) and 5-8x PE using mid cycle assumptions #Commodities

Jan 17 • 6 tweets • 2 min read

The link for those who wish to take up my 5 stock tips offer near the next cycle low.

We harvest a 10 bagger on average every 2 years by ensuring our entry is is near a deep cycle low & 3-5yr sitting.

Note from 2024/25 cycle lows in #cyclicals there will be > 100 10 baggers through 2027.

Apr 5, 2025 • 4 tweets • 1 min read

The process...

Mass Contagion = creates generational entry points

Margin calls across the board, ETF redemptions = baby goes out with the bath water

Decoupling of #commodities will occur in the next 30-40% downside

Prepare 10 bagger watchlists for slow scale in post -20%

You must run toward the fire as everyone else is running away in fear, as it will soon be time to be greedy.

Apr 4, 2025 • 5 tweets • 1 min read

#Vietnam day 2, 280 stocks are limit down for the 2nd day, Index -6% at open.

Landing several days out.... Watchlist refreshed, initial entry points 20% lower.

A typical limit down stock in #Vietnam worth looking below 5yr lows on < 5x PE.

Apr 1, 2025 • 5 tweets • 1 min read

Pre-production #uranium cap performance from 1Q 2025 lows

2025 #Uranium is about service bottlenecks (sticker shock to Utes) + Russian supply cuts to the US + unexpected supply cuts (KAP pivot to East + negative events)

2H 2025 several US Utes will likely require action on replacement supply sources = Spot buying (8-12lbs)

Dec 30, 2024 • 4 tweets • 1 min read

What's a US$5m pre-production cap #gold #silver play with 2 mine $200m NPV (@ 2700 gold) worth as the following occurs in 2025?

PFS release on 1st mine in January 2025

1st mine offtake financing of $28m or strategic partner financing?

Dilution over 2025 likely to be $2m

Potential outcomes as #gold spot climbs through $3k:

A) no project funding and $2m dilution at cap lows (25% probability)

B) project funding secured & +200-400% rerate (50% prob)

C) dilutive project funding secured at the cost of 50% project stake reduction (25% prob)

Nov 11, 2024 • 5 tweets • 1 min read

As our followers will recall, we used $GBTC at its 50% disc near cycle lows to achieve our #bitcoin exposure, our scale down for this cycle commences at $84k through $135k over the next 12 months. This will equate to >10x returns from GBTC over a 3 yr holding period from 4Q 2022.

The cycle continues to dictate our 10 bagger position, as it should do for our followers.

Nov 1, 2024 • 4 tweets • 1 min read

Pre-production micro cap #Commodity stocks rules to adhere to:

Dilution: 80%

Elapsed: 12-18m

D) DFS to production (compelling project)

Dilution (cumulative) 90% plus

Elapsed Time: 30-48 months

Total elapsed: 76 to 114 months

For a downcycle one can double the dilution.

Oct 17, 2024 • 9 tweets • 3 min read

Without regards for the cycle, 10 baggers are mythical beasts.... With regards to the cycle they are 30% probabilities 🎯 with the following characteristics..

A) down > 95% from the previous cycle peak

B) trading < 3% NPV near cycle lows

C) implied 3-4yrs out trading on <0.4x CF

Active example there will be over 20 10 baggers from the #lithium space from recent cycle lows through the 2027 cycle peak.

Note the amount of 10 baggers from 2020 lows through 2021/22 highs compared with 2022 highs through 2024 lows.

The #cycle is everything

Sep 29, 2024 • 5 tweets • 2 min read

Top positions for us are ones near exiting as they have performed so well, where new top positions come in at 2% and can move to 15% by outperformance. Old asymmetric themes have performed and are on the chopping block, this is how to play cyclicals.

Cyclicals trading > 8x 2027 peak CF are an exit, those trading <0.3x are an entry.... Knowing the difference is the art work.

Sep 28, 2024 • 4 tweets • 1 min read

Feasibility studies are conducted by profession enterprises with much experience, the AISC is an equalizer on the value of a #uranium pound, as is the project IRR, to say otherwise indicates ones lack of comprehension

We prefer at surface low grade, with high mill feed grade....

ISR annual capex is opex and should be treated as such

Credits can be very important is net costs

1st Tier AISC project < $36 in 2025 will likely move to <$40 by 2028 and <$44 by 2031

#uranium

Sep 26, 2024 • 4 tweets • 1 min read

Some of our recent unexpected #uranium developer moves from lows:

$GXU +100% winding back some extraordinary negativity

$AEE +57% Tiris powering up for FID

$AEC +60% Producer on the horizon

$FSY +72% It's time to revise the DFS

$LAM +63% Which project 1st?

$WUC +32% Processing at WM?

This group should average +200-300% this #uranium upleg based on 1Q 2025 US$100 spot and $86 LT pricing

Sep 3, 2024 • 5 tweets • 1 min read

$TOE #uranium

In 3-4 weeks a passive fund may drop 18m shares into the bid over a few days due to cap size rules (which may reverse again prior to the cycle peak).

This passive flow may result in an extreme low entry point for contrarian investors, >95% disc from peak.

Post the Western Australian ban removal (1-5yrs) it crystalizes a $700m plus NPV.

2% of NPV = 2% portfolio weighting = diluted upside of 8x

1% of NPV = 5% wght = diluted upside of 15x

0.5℅ of NPV = 10% wght = 25x returns

Holding period 2-6yrs

Aug 28, 2024 • 4 tweets • 1 min read

What's does a 8x cyclical returner look like over the 3-5yrs?

Down > 95% from highs

Cap < 3% of NPV

IRR > 40%

Implied trading < 40% of cashflow

Related commodity spots can be deep into cost curves

Reasonable probability of getting into production within this coming upcycle

What does a 16x cyclical return look like?

Down > 97%

Cap < 2% of NPV

Cap < 25% of annual cashflow 3-4yrs out

Good mgmt execution

Alignment of interests

Aug 3, 2024 • 5 tweets • 1 min read

For our followers: Now that the sky has started it's fall and you have stocked up on dry powder as we have guided, the next step is to review watchlist entry points. It's key one moves to a Greed mode over the next 6 months as markets bottom, removal of Fearfulness.

Some massive compelling cycle bottoms will occur in such industrial commodities such as #lithium

Look for...

> 95% declines from peak

Cap < 3% of NPV

Cap < 30% of Cash flow 3-4yrs out

IRRs > 40% on $25k pricing