An argument on the Doctrine of Monetized Speech and the Necessity for Its Reversal

Preface:

I hope many of you enjoy reading these long-form articles and treatises, which explore how I believe we can address many of the failings we see in our government and in the way this country is governed. One of these critical issues is that money equals free speech. This doctrine, introduced in the Buckley v. Valejo decision of 1976, in my opinion, started a chain of catastrophic and expanding events by which domestic and outside powerful forces have shaped our way of life.

Money equals free speech. Think about it for a second. The money of the poor and wealthy is equivalent to free speech, but what distinguishes them? The money of the poor is limited, while the money of the wealthy is not. Imagine a billionaire buying all of the billboards in a city or even a state to put their speech up on whatever topic or issue they want you to see, while all you can do is print out flyers and hang them up on lamp posts. See the difference?

The amplification of a billionaires speech drowns out even the voices of a large number of people. This isn't the speech our founders envisioned, nor should this country allow. Not just as citizens, but as voters. Since 1976, this country has allowed massive amounts of money to shape the way it thinks, talks, and comports itself, through Superpacs, dark money, foreign donations, and lobbying. This has become a monumental problem.

I'm a 1A absolutist. I believe the marketplace of ideas should be front and center to who we are as a people, that society and the market should make determinations of what is allowable speech, even if it's hateful, wrong, or inopportune. The marketplace of ideas will determine which of these things is appropraiate for our society and how it wants to shape its communication. Not all ideas are good ones. We know this, but powerful forces are spending untold billions of dollars worldwide to influence our thoughts while we as mere citizens get drowned out in the process.

But speech shouldn't be bought, sold, and commoditized, and that's what we are enduring right now as a country and as a society. I say it must stop. That is why I'm writing this doctrine to eliminate the notion that money equals free speech and to outline what it will take. Additionally, what the potential benefits of reverting to a system where this no longer occurs will be.

You've read my articles on the pros and cons of abolishing the Fed and what that looks like. You've read my articles on why the Fed should be abolished and what it should be replaced with to further the financial and economic aims of the country and return it to a more constitutional framework. This article now aligns with the evolution that further expands the freedoms and liberties of citizens, aligning with the principles outlined in these other articles. There will be more.

With that, I will leave it to you to decide if this is the right path to go in or not. If you believe your 1A rights would be better served by not being bought and paid for, and never being heard, please spread this far and wide. Many of you who follow and have listened to me on spaces have heard me say this. It's time this country abandoned equating money with speech. It has hurt us deeply, and it needs to stop.

I want to thank the founders for their fight in allowing me to express these ideas and beliefs under the First Amendment. I don't have to worry about being censored, arrested, or suppressed. These are my ideas, and I get to share them with you.

As always, I’m not infallible. I put a lot of effort into researching and developing these articles into meaningful and substantive informational packets so that you can read, process, and digest what is being said.

However, I make mistakes, and I want to learn from them, understanding where those mistakes are, so they aren’t made again. Through your reading of my vision, I become better. So, without further ado, please enjoy my work. If you like it, consider sharing it with a quote repost, follow, or a simple like. Be well, and thank you for your time to read this.

Introduction

This argument contends that the SCOTUS campaign finance jurisprudence, which equates large-scale financial expenditures with protected speech, is a grave constitutional error rooted in an antiquated and simplistic understanding of the First Amendment.

The doctrines from Buckley v. Valeo and Citizens United v. FEC have established a legal framework that prioritizes a narrow, libertarian conception of "negative liberty" or freedom from restraint, while actively undermining the "positive liberty" or the capacity to participate meaningfully of the vast majority of citizens.

This has created a failed marketplace of ideas, fostered systemic corruption now amplified by modern technology, and placed the First Amendment in an irreconcilable conflict with the Constitution's guarantee of a republican form of government. For the SCOTUS to maintain its legitimacy and for the Republic to thrive, this doctrinally flawed and empirically damaging precedent must be overturned.

Aug 24, 2025 • 7 tweets • 25 min read

A Framework for Constitutional Money: A Rules-Based, Competitive, and Fiscally Disciplined Alternative to the Federal Reserve System

Preface:

As some of you have seen and read, my prior pinned tweet about what the pros and cons were of ending the Fed. I provided a thorough analysis of what it would take for that to happen, including the ifs, whens, whys, and whats. I tried to make it as comprehensive as I could. I spent a lot of time (a year) researching and really digging into the entire system from before it started, what precipitated or necessitated the need for a Federal Reserve System, and how it has been used and has affected the course of this country using its dual mandate to drive the economics of this country and frankly the world. It was an opportunity to explore a replacement theory or to understand at least what it would take to replace it, given all of the criticisms since its inception to now.

I initially wanted to include it in that analysis, but given the time and my inclination, I did not feel ready or prepared to fully flesh out a system by which a replacement for the fed could be made. I had to sit for a long time in my head to hammer out a system that would have a principled framework from the very basis of constitutionality. That is and has been one of the chief complaints for the Federal Reserve overall. That its very existence, even though it was passed in Congress with the Federal Reserve Act of 1913 alongside the Revenue Act of 1913, which allowed Congress to tax your labor as well, would be so polarizing in its mission.

What I aim to do here is to outline for you, the reader, a framework for what the Federal Reserve system should be replaced with. If you could see what it took to come up with this, it would look like a conspiracy theorist's wall with pictures and a string leading to a super villain at the top. But seriously, I believe this system has a real chance of being read by the right people and possibly being adopted. Now, is it perfect? Only in my eyes, like a parent who stares at their newborn child. But for the rest of you, you will find flaws and holes in it that will, for the most part, make it a better system overall.

So, as always, if you see something, say something. If you think you have a better way to get something done within this framework, by all means let me know via DM or in a reply to this post itself. I want to hear it. I’m not infallible. I make mistakes, and I want to learn from them, understanding where those mistakes are, so they aren’t made again.

In doing so, I become better through your vision. So, without further ado, please enjoy my work, and if you like it, consider a follow or liking it. Be well, and thank you for your time to read this.

Introduction:

The modern system of discretionary central banking, embodied by the Federal Reserve, represents a century-long experiment in economic management. While intended to provide stability, its history is marked by persistent inflation, the creation of severe moral hazards, and the enablement of unprecedented levels of government debt. Please reference the prior pinned post of the analysis titled: Abolishing the Federal Reserve – Pros and Cons: A Comprehensive Analysis of Feasibility, Consequences, and Alternatives on 07/17/2025.

The core flaw lies not in the desire for a stable currency, but in the delegation of immense, discretionary power to a quasi-independent body of technocrats. This structure is both constitutionally suspect and practically problematic. The result is a system where monetary policy is often unpredictable, subject to political pressure, and serves to socialize the losses of the financial sector while systematically eroding the purchasing power of the public.

A return to first principles is required. A monetary system fit for a constitutional republic should not be based on the shifting judgments of a few, but on a foundation of clear rules, robust competition, and inviolable fiscal discipline. It must be a system where the monetary authority is a servant to the law, not its master, and where the government is a participant in the economy, not its ultimate guarantor.

This solution to ending and replacing the Federal Reserve outlines such a framework. It is not a proposal to merely tweak the existing Federal Reserve, but to replace it entirely with a new monetary constitution built upon four integrated pillars. This framework is designed to be constitutionally sound by restoring Congress’s role in setting monetary rules – one of the chief and loudest complaints of its critics since its inception, economically efficient by providing a stable and predictable environment for growth, and structurally resilient by severing the link between money creation and government spending. It is a blueprint for a system where the value of the currency is anchored not to a volatile commodity, but to the credibility of a transparent rule, reinforced by the discipline of the free market.

Jul 17, 2025 • 6 tweets • 53 min read

Abolishing the Federal Reserve – Pros and Cons: A Comprehensive Analysis of Feasibility, Consequences, and Alternatives

The Federal Reserve System, which is the central bank of the United States, is what is considered a cornerstone of the modern American/Global economic framework and architecture. Since its inception in 1913 and consequently alongside the 16A passed and ratified in the same year, it has been given immense power/responsibility. Not just from a currency and monetary policy point of view, but it wields power over financial markets, interest rates, rates of inflation, and so on.

It was intended to serve as a shield against the financial chaos that periodically shook the nation in the preceding century. However, from the moment of its creation, the Federal Reserve or The Fed, as many call it, has been a subject of intense and unceasing debate. To its proponents, it’s an indispensable institution providing monetary stability, a flexible currency, and a crucial defense against economic downturns and financial panics. To its naysayers, it’s an unconstitutional and corrupt entity, an engine of inflation, a facilitator of government profligacy, and the primary cause of potential and possible economic instability it was meant to prevent.

This century-long controversy has recently gained renewed vigor, fueled by the long shadow of the 2008 financial crisis, unprecedented monetary interventions during the COVID-19 pandemic, and a subsequent surge in inflation that has eroded the purchasing power of households worldwide. These events have put the Federal Reserve's operations into the public spotlight and amplified the calls of a vocal and politically organized movement to "End the Fed". This movement, once confined to the circles of Austrian economists and libertarian thinkers, has entered the political mainstream, prompting legislative proposals for the Federal Reserve's abolition.

The question of whether "Is it possible to end the Federal Reserve?" isn’t merely a theoretical exercise but a question of profound practical importance. Answering it requires moving beyond partisan arguments, but to engage in a rigorous and multi-faceted investigation. This report endeavors such an investigation. It will look at the feasibility, consequences, and alternatives associated with dismantling the central bank.

The analysis begins by establishing a foundational understanding of why the Federal Reserve was created, examining the historical context of financial instability that made its establishment necessary. It will then look at the core functions the modern Fed performs, from its dual mandate of promoting maximum employment and stable prices to its critical roles as the lender of last resort and the operator of the nation's payment system.

Once this baseline is established, the report will turn to a systematic and thorough examination of the case for abolition, presenting the multi-pronged economic, moral, and constitutional criticisms that form the intellectual bedrock of the End the Fed movement.

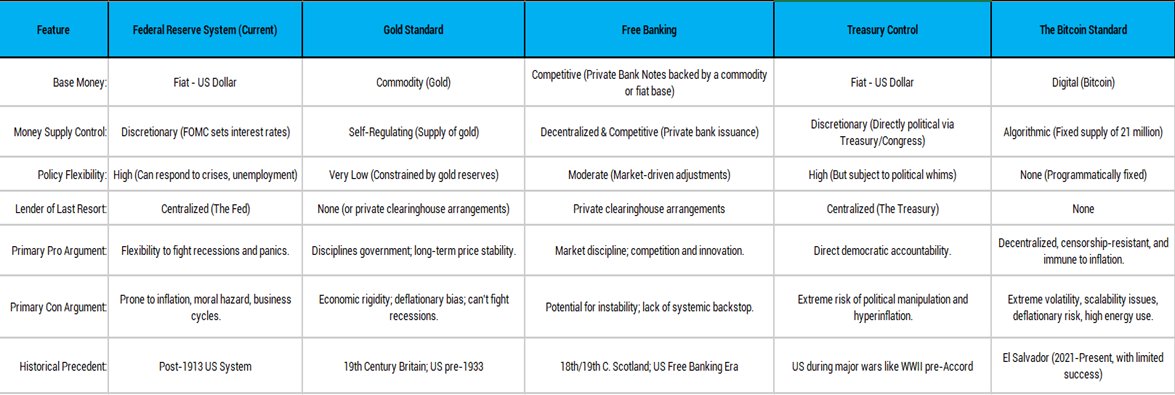

Also, it will confront the monumental cons of abolition, analyzing the logistical gauntlet of undoing such a deeply embedded institution and the potentially catastrophic economic/geopolitical consequences of its absence. And finally, the report will critically evaluate the primary alternatives proposed to replace the current system: a return to the gold standard, the implementation of a free banking regime, the transfer of monetary authority to the US Treasury, or the adoption of a decentralized digital currency like Bitcoin.

Attempting to explore this full spectrum of issues presented above, this report aims to provide a comprehensive, nuanced, and definitive analysis. It will attempt to inform policymakers, financial professionals, and engaged citizens with the deep, evidence-based understanding necessary to navigate one of the most complex and consequential economic questions of our time. It will be broken up into sections to address the various breadth of topics that this report will delve into.

Before I go on, I hope you enjoy this work. It’s something I’m undertaking on a wide array of important topics to look at, but also issues surrounding the Federal Reserve in a more in-depth and needed way. Too often, we discuss these matters at the surface from likes and dislikes, but we rarely get underneath that surface and dive deep.

I’m trying to change that and give comprehensive, researched, fact-based knowledge on topics like this. This is my research and it’s not AI-based. I’ve deliberately steered away from AI to ‘fill in the gaps’ because AI often gets it wrong, and its bias also factors into the research. I will try to keep my bias as minimal as possible and give you as much objectivity as I can as humanly possible. If I’ve failed in that in this report, please accept my apologies. It isn’t intentional.

However, if you believe this report gave you value and insight, consider a follow. But most of all, as I’m a small account, repost it anywhere/everywhere you can to get this information out there. Thank you. Let’s get started.

Section 1: The Federal Reserve System: Architecture, Mandate, and Rationale

To understand the arguments for abolishing the Federal Reserve, an understanding of what it’s, what it does, and why it was created. The Federal Reserve didn’t emerge from a vacuum. It was a deliberate and deeply controversial solution to a century of documented financial instability. Its architecture, mandate, and the very rationale for its existence are rooted in the economic injuries that defined American finance before 1913. This section provides the essential context for establishing a baseline against the critiques, and proposed alternatives can be properly evaluated.

1.1 Genesis: A Response to a Century of Financial Instability

The narrative of the Federal Reserve's creation is fundamentally a story of a nation grappling with the violent economic cycles of the 19th and early 20th centuries. The period before 1913 wasn’t a tranquil era of laissez-faire stability but was marked by frequent, severe financial panics that inflicted widespread economic hardship. The establishment of the Fed was the culmination of a long and contentious search for a mechanism to tame this volatility.

The United States has a long history of ambivalence toward central banking. The nation's first two experiments, the First Bank of the United States from 1791–1811 and the Second Bank of the United States from 1816–1836, were modeled on the Bank of England and designed by figures like Alexander Hamilton to manage the nation's war debts, provide a stable currency, and create a central source of capital for economic development. Both were successful in many respects but ultimately fell victim to a deep-seated Jeffersonian suspicion of concentrated financial power and concerns about their constitutionality, leading Congress to refuse the renewal of their charters.

The demise of the Second Bank ushered in the Free Banking era around 1837–1862, a period often romanticized by some critics of central banking, but which was highly unstable. The system was characterized by a decentralized patchwork of state-chartered banks, each free to issue its own private banknotes. This led to a confusing and unreliable monetary landscape. While the term free banking suggests a lack of regulation, the era's instability was often exacerbated by flawed state laws. For example, many states prohibited banks from establishing branches, which prevented geographic diversification and made them more vulnerable to local economic shocks. Also, many states required banks to back their banknotes with specific state government bonds, tying the health of the bank to the fiscal condition of a single state government and concentrating risk. The result was a system prone to bank failures and periods of financial turmoil.

The period following the Civil War and the establishment of the National Banking System did little to solve the fundamental problem of financial fragility. Between 1863 and 1913, the United States experienced at least eight distinct banking panics. While some were confined to New York City, the crises of 1873, 1893, and 1907 were nationwide contagions that were devastating to the nation and the world.

The Panic of 1873, triggered by the failure of the banking house Jay Cooke & Co. due to overinvestment in railroads, led to the first closure of the New York Stock Exchange, the failure of at least 100 banks, and caused a depression that lasted until 1879. The Panic of 1893 was even worse, with over 500 banks and 15,000 companies failing, and unemployment skyrocketed.

These crises repeatedly exposed the two critical weaknesses of the US banking system, which were an inelastic currency and the lack of a lender of last resort. The money supply, tied to gold or national bank reserves, couldn’t expand to meet the public's demand for cash during a panic.

When depositors feared for a bank's solvency, they would run to withdraw their funds, and banks would be forced to sell assets at fire-sale prices, and many would fail, causing the panic to spread.

The Panic of 1907 was the final straw that broke the camel’s back. A failed attempt to corner the market in United Copper Company stock triggered a series of events that led to runs on New York trust companies, spreading fear throughout the entire financial system.

The crisis was ultimately squashed not by a government institution, but by the private intervention of financier J.P. Morgan, who organized liquidity pools and decided which firms would be saved and which would fail. The specter of a single private citizen wielding such immense power over the nation's financial fate convinced many that a public institution was needed to perform this role.

In response, Congress created the National Monetary Commission in 1908, which studied the central banking systems of Europe. This study and the ensuing political debate, which pitted agrarian and populist interests against those of Wall Street and big business, allowed the Federal Reserve Act of 1913 to become widely adopted and passed.

The Act was a uniquely American compromise that instituted a decentralized system of twelve regional Reserve Banks, overseen by a public Board of Governors in Washington, D.C., designed to provide the elastic currency and lender-of-last-resort functions that the previous system lacked.

The Fed's creation was the result and response to the well-documented and recurring failures of the decentralized, panic-prone financial system that preceded it.

1.2 The Modern Fed's Core Functions: Pillars of the Financial System

Over the century since its founding, the Federal Reserve's roles and responsibilities have evolved significantly, but its core functions remain central to the operation of the US economy. These functions are deeply intertwined, often creating complex trade-offs/compromises that are at the heart of modern monetary policy debates.

The Dual Mandate: Price Stability and Maximum Employment

The centerpiece of the Fed's current mission is its dual mandate, which is a set of goals assigned by Congress. The Federal Reserve Act, as amended in 1977, directs the Fed to conduct monetary policy "so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates". The goals of stable prices and moderate long-term interest rates are generally seen as a single objective, since stable prices are a prerequisite for moderate long-term rates, leaving the Fed with its two primary and often conflicting objectives.

The first is Maximum Employment. This doesn’t mean a 0% unemployment rate because economists recognize that there is always a level of frictional and structural unemployment as people change jobs and industries evolve. The Fed aims for the noncyclical rate of unemployment, which is the highest level of employment the economy can sustain without generating inflationary pressure. This level is not fixed and changes over time based on non-monetary factors. However, the Fed does not specify a fixed goal for employment but instead assesses it based on a wide range of labor market indicators.

The second is Stable Prices. This has been explicitly defined by the Fed's policymaking body, the Federal Open Market Committee - FOMC, as an average inflation rate of 2 percent per year, as measured by the Personal Consumption Expenditures – PCE price index. This target is considered low enough to avoid the economic distortions of high inflation but high enough to provide a buffer against deflation, which in this case would be a general decline in prices that can be uniquely destructive to an economy by increasing the real burden of debt and discouraging spending.

This dual mandate presents an inherent challenge. The policies used to stimulate the economy and promote employment, such as lowering interest rates, can also fuel inflation. Conversely, policies used to fight inflation, such as raising interest rates, can slow the economy and increase unemployment. Much of the Fed's work involves navigating this trade-off, making it a constant balancing act rather than a simple pursuit of fixed targets.

The Lender of Last Resort - LOLR

A foundational reason for the Fed's creation was to act as a lender of last resort, a function critical for maintaining financial stability. In a fractional-reserve banking system, banks hold only a fraction of their deposits in cash. If a large number of depositors demand their money back at once in a bank run, even a solvent bank can become non-liquid and fail. The fear of one bank's failure can spread, causing runs on other banks and potentially triggering a systemic crisis.

The Lender of Last Resort function is designed to break this chain of contagion. The Fed can provide short-term, emergency loans to make solvent but non-liquid financial institutions, ensuring they can meet depositor demands and restoring confidence in the system.

The classical theory of The Lender of Last Resort, articulated by Walter Bagehot in the 19th century, holds that the central bank should lend freely, but at a high penalty rate, and only against good collateral to discourage banks from relying on it except in true emergencies.

In the modern era, particularly since the 2008 financial crisis and the C19 pandemic, the Fed has expanded its The Lender of Last Resort role far beyond traditional discount window lending to commercial banks. Invoking its emergency powers under Section 13(3) of the Federal Reserve Act, it has provided liquidity to a wide range of non-bank financial institutions, including investment banks and money market funds, and has even established facilities to lend directly to corporations and municipalities.

While these actions were credited with preventing a complete financial collapse, they have also fueled intense debate about moral hazard—the idea that bailing out institutions encourages excessive risk-taking in the future.

Management of the National Payment System

Beyond its high-profile monetary policy and crisis-fighting roles, the Fed performs the crucial but often overlooked function of managing the plumbing of the US financial system. The Reserve Banks operate critical infrastructure that facilitates the daily transfer of trillions of dollars between banks, businesses, and government agencies.

Key payment services provided by the Fed include:

1. Automated Clearinghouse (ACH): This system processes large volumes of credit and debit transfers for services like direct deposit of paychecks, Social Security benefits, and automatic bill payments.

2. FedWire Funds Service: A real-time gross settlement system that enables participants to make large-value, time-sensitive payments with immediate finality.

3. Check Clearing: While the use of checks has declined, the Fed still provides services for collecting and settling checks between banks.

4. FedNow Service: Launched in 2023, this is a new instant payment service that allows for round-the-clock, real-time payments, enabling individuals and businesses to send and receive funds immediately, 365 days a year.

In this capacity, the Fed acts as a bank for banks that ensures the smooth, efficient, and secure settlement of transactions that underpin the entire economy. Any plan to abolish the Federal Reserve must account for how these essential, high-volume operational services would be maintained without disruption.

The Modern Monetary Policy Framework - From Scarce to Ample Reserves

The way the Fed implements monetary policy has undergone a fundamental transformation since the 2008 financial crisis. Before 2008, the Fed operated in a "scarce reserves" framework. It would buy or sell government securities in the open market to make small adjustments to the total amount of reserves in the banking system, influencing the federal funds rate (the rate at which banks lend to each other overnight) to move toward a specific target.

Following the crisis, the Fed's large-scale asset purchases, known as Quantitative Easing or QE as it has become to be known, flooded the banking system with trillions of dollars in reserves. This created an abundant reserves system, which remains in place today. In this framework, the sheer volume of reserves means that small changes in supply no longer affect the federal funds rate. Instead, the Fed now controls the rate primarily by setting its administered rates, particularly the interest rate it pays on reserve balances or IORB.

Banks have no incentive to lend to each other at a rate lower than what they can earn risk-free from the Fed, making the IORB an effective floor for the federal funds rate. This new system provides effective control over interest rates even when large amounts of liquidity are needed to support the economy, as was seen during the C19 pandemic. But, it also means the Fed must maintain a much larger balance sheet than in the past, a point of contention for its critics.

1.3 The Paradox of Independence and Accountability

The structure of the Federal Reserve is a unique hybrid, designed to resolve a fundamental tension in democratic governance, which is how to entrust immense economic power to an institution while insulating it from short-term political pressures. This has led to a system that is often described as independent within the government.

The Fed's independence is structural. The Board of Governors is a federal government agency, but the seven governors are appointed by the President and confirmed by the Senate for long, 14-year, staggered terms. This is intended to ensure that no single president can appoint a majority of the board and to allow governors to make policy decisions based on long-term economic considerations, rather than the short-term electoral calendar.

Academic research and international experience suggest that central bank independence is strongly correlated with lower and more stable inflation, as it allows policymakers to make unpopular decisions, like raising interest rates, when necessary.

The twelve regional Reserve Banks have a quasi-private structure. They are technically incorporated and have member commercial banks in their districts as shareholders. However, this ownership is, to a large extent, symbolic. The shares cannot be sold or traded, and they pay a statutorily fixed dividend of 6 percent.

They do not confer control rights in the way corporate stock does. The presidents of the regional banks are appointed by their local boards of directors, but must be approved by the Board of Governors in Washington. This structure is intended to blend public accountability with private-sector input and experience.

Despite this operational independence, the Fed is not free from oversight. It’s a creature of Congress and is ultimately accountable to the public and their elected representatives. This accountability is enforced through several mechanisms:

1. Congressional Testimony: The Fed Chair testifies before Congress semiannually on the Fed's monetary policy report, and other officials testify frequently.

2. Reporting Requirements: The Fed regularly publishes reports on its activities, including its annual report, FOMC meeting minutes, and weekly balance sheet data.

3. Audits: The Fed's financial statements are audited annually by an independent public accounting firm. In addition, the Government Accountability Office (GAO) conducts frequent audits of many Fed activities, though its audits of monetary policy deliberations are restricted.

The central issue is not, as some critics claim, that the Fed is a private corporation secretly controlled by bankers. The more substantive and valid debate revolves around whether this unique structure has the right balance. Critics argue that this insulation from the political process is fundamentally undemocratic, granting vast, unchecked power to a board of unelected technocrats.

Proponents counter that this very independence is what allows the Fed to pursue the long-term goal of price stability, a goal that would be consistently undermined if monetary policy were subject to the whims of electoral politics. This paradox of independence and accountability lies at the heart of the Fed's legitimacy and is a recurring theme in the debate over its existence.

It also strikes at the heart of those who claim the Fed has never been audited, which is not the case. The Fed has been audited multiple times since its creation and ratification in 1913. Critics are quick to argue that the Fed is hiding important monetary information and is a hive of nefarious economic activity that is hobbling or has hobbled our economy in one form or another.