Senior Investment Advisor and Portfolio Manager at Wellington-Altus. Tweets are not investment advice.

DM with your financial planning and investment questions.

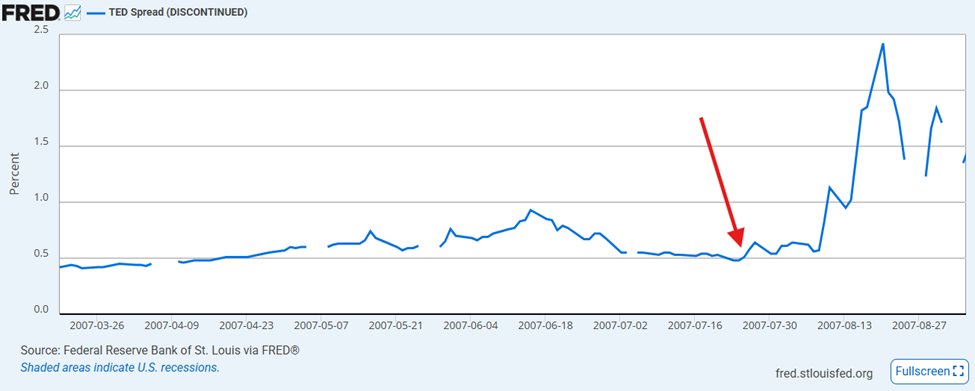

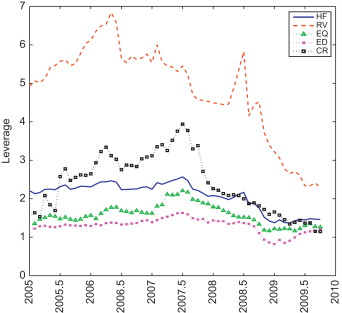

Hedge fund total leverage and across various strategies peaked into the 2007 quant quake

Hedge fund total leverage and across various strategies peaked into the 2007 quant quake

BoC presumably knows this.

BoC presumably knows this.