Chief Economist @LawEconCenter. Antitrust and price theory. 📝Price Theory Newsletter https://t.co/1S7TB6ANUP

First, Moody's isn't measuring spending. It's bascally just income.

First, Moody's isn't measuring spending. It's bascally just income.

@instrumenthull @borusyak @lihua_lei_stat @asheshrambachan @causalinf @steventberry @jamesbrandecon @lewbel

@instrumenthull @borusyak @lihua_lei_stat @asheshrambachan @causalinf @steventberry @jamesbrandecon @lewbel

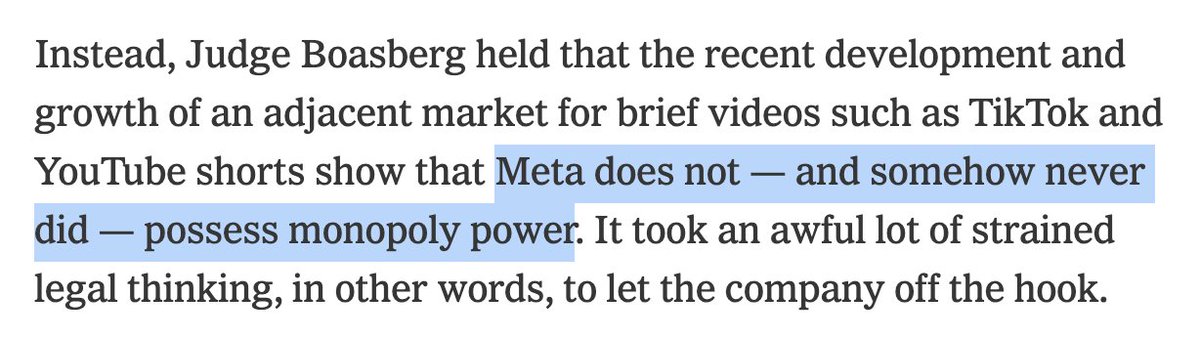

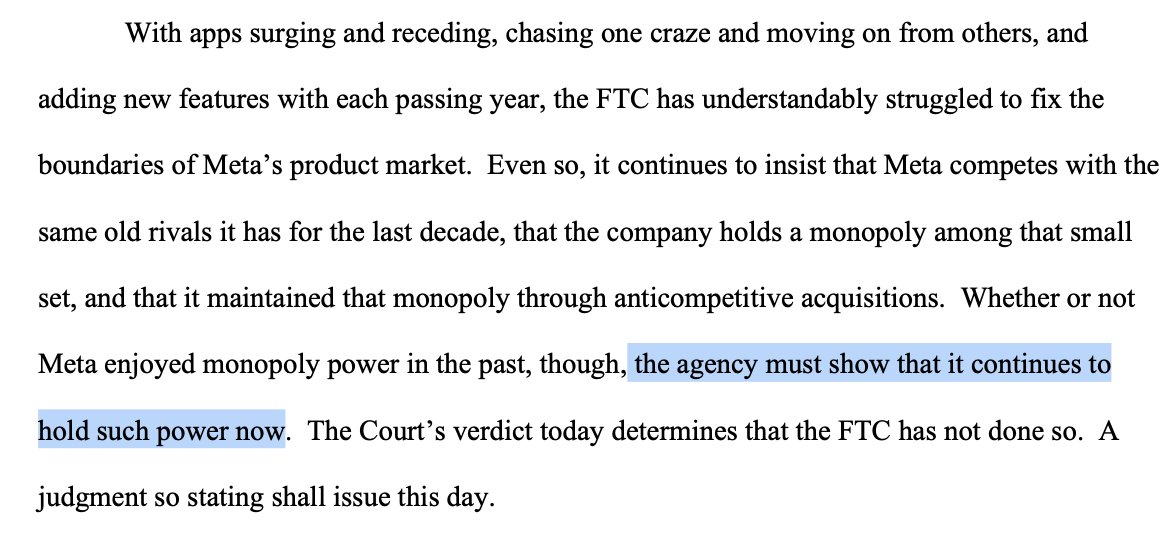

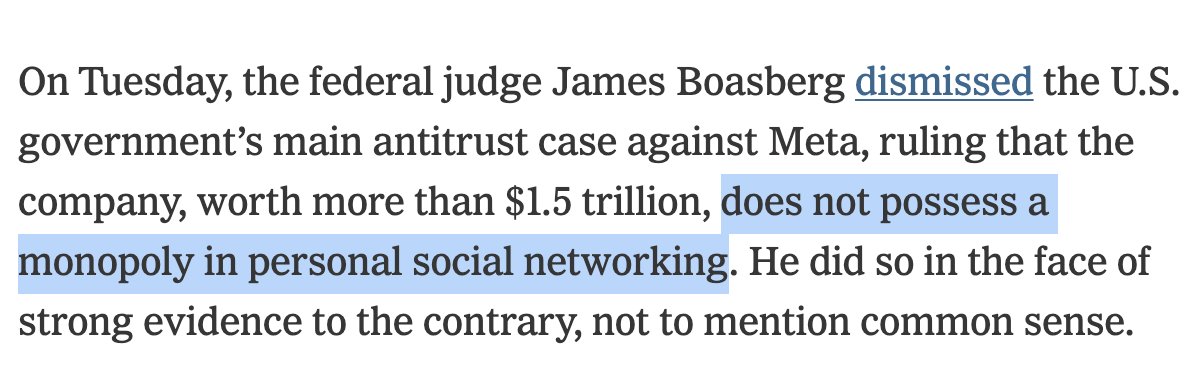

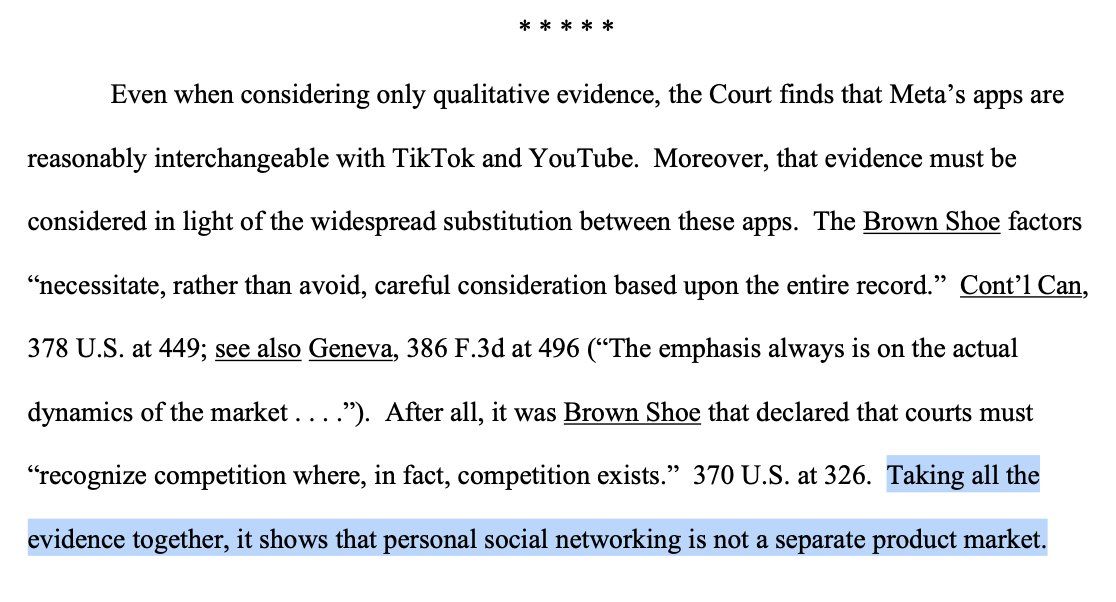

Right out the gate, Wu is wrong. That is not what the ruling said! Boasberg did not rule on whether Meta had a monopoly is personal social networking.

Right out the gate, Wu is wrong. That is not what the ruling said! Boasberg did not rule on whether Meta had a monopoly is personal social networking.

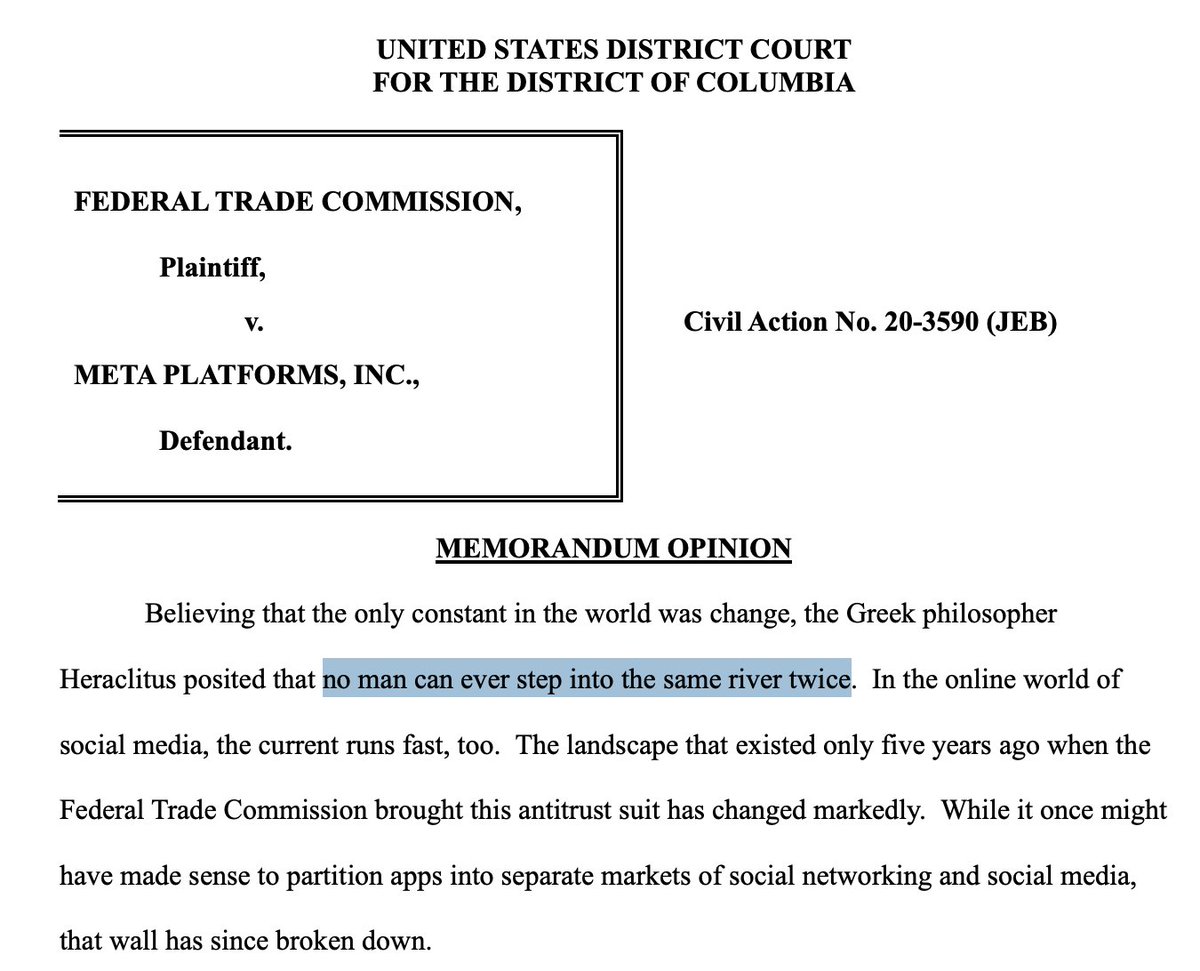

The vibe is set in line 1: Heraclitus and never stepping in the same rivier twice.

The vibe is set in line 1: Heraclitus and never stepping in the same rivier twice.

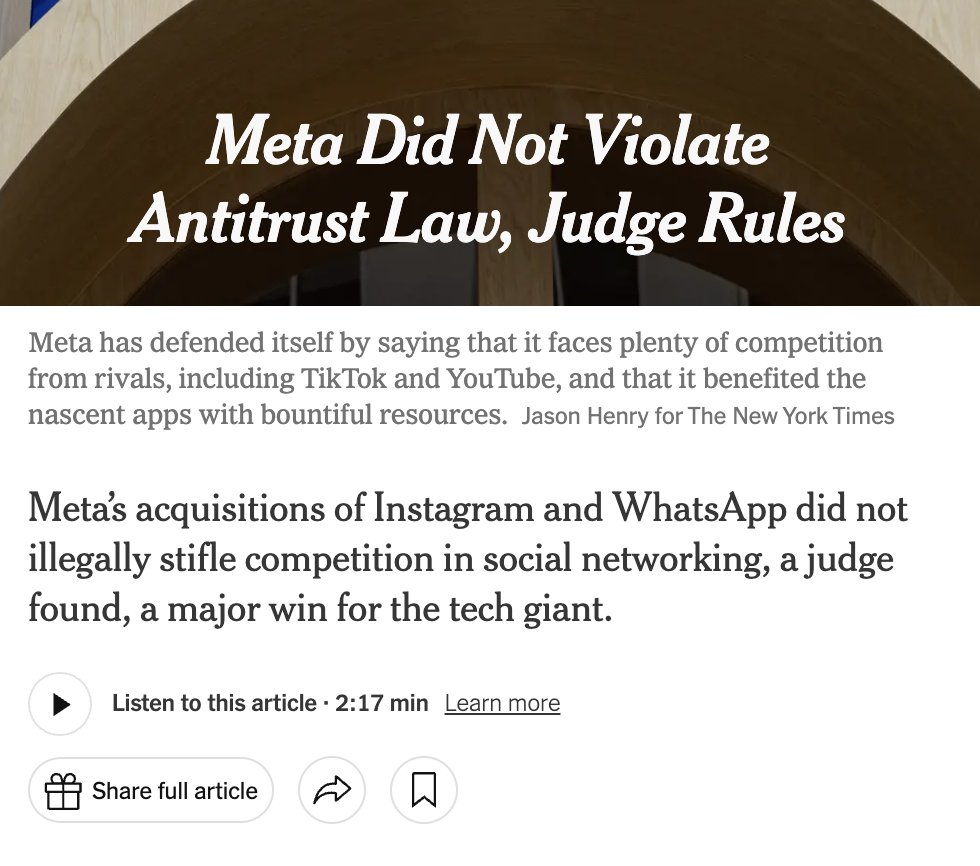

Piece here nytimes.com/2025/11/16/opi…

Piece here nytimes.com/2025/11/16/opi… Link to paper:

Link to paper:

Hayek taught us markets require minimal information. Traders only need to know prices, not everyone's preferences or endowments.

Hayek taught us markets require minimal information. Traders only need to know prices, not everyone's preferences or endowments.

The economic logic makes some sense:

The economic logic makes some sense:

For most of human history, living standards barely changed. Then something shifted.

For most of human history, living standards barely changed. Then something shifted.  It's a bit of shadowboxing against I'm not sure who.

It's a bit of shadowboxing against I'm not sure who.

Suppose a good is in fixed supply (perfectly inelastic). Increasing that tax generates no deadweight loss.

Suppose a good is in fixed supply (perfectly inelastic). Increasing that tax generates no deadweight loss.

The thing about small businesses is... They suck, in terms of job creation, productivity, etc.

The thing about small businesses is... They suck, in terms of job creation, productivity, etc.  Don't be confused by the currency/captial/trade stuff. What is he actually saying?

Don't be confused by the currency/captial/trade stuff. What is he actually saying?

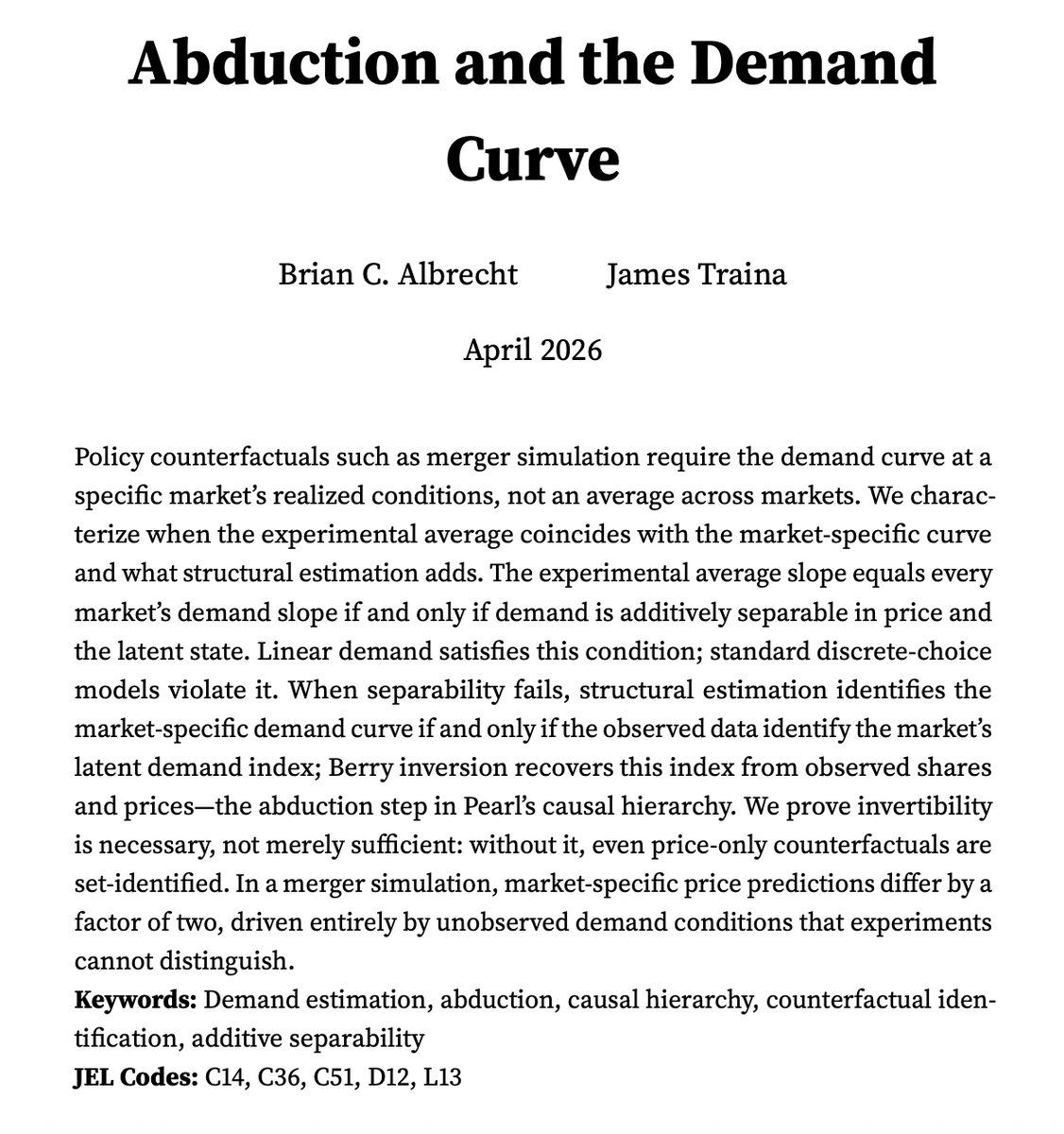

The liability phase is in the books.

The liability phase is in the books. Ravid, Roesler, and Szentes (2022) found a striking inefficiency: consumers won't fully learn about products even when information is nearly free.

Ravid, Roesler, and Szentes (2022) found a striking inefficiency: consumers won't fully learn about products even when information is nearly free.