Founder, CEO and CIO @ARKinvest. Thematic portfolio manager for disruptive innovation, mom, economist, and women's advocate. Disclosure: https://t.co/chxRD4oWOd

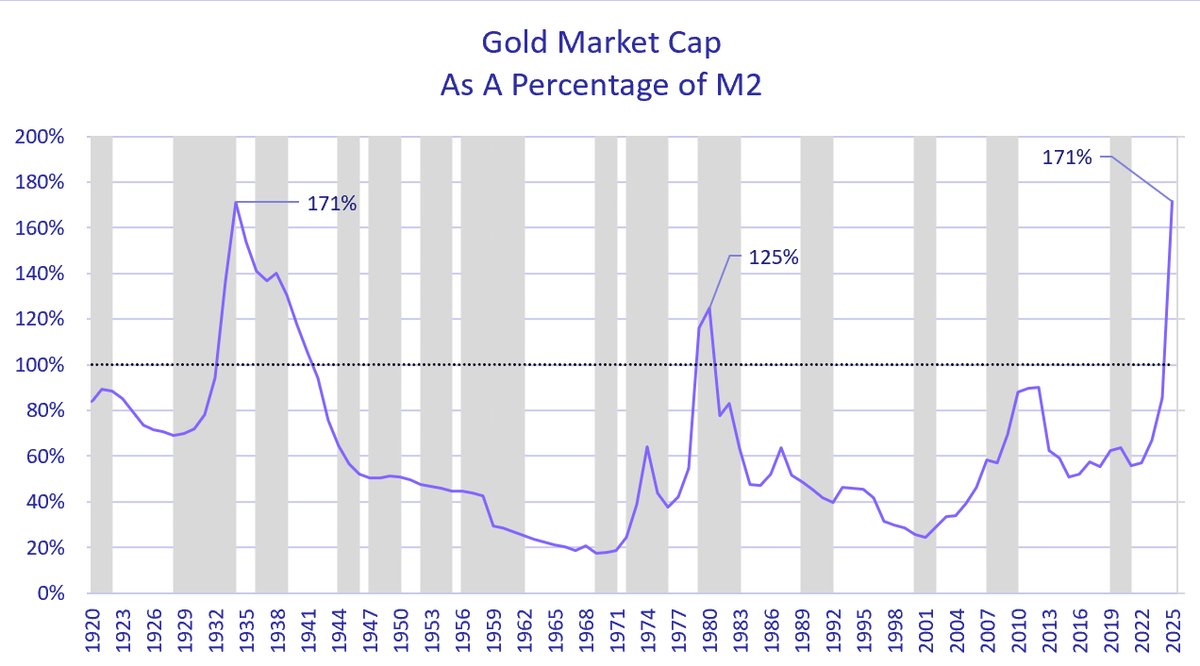

the ratio of gold to M2 has hit the all time high recorded during The Great Depression in 1934. In that crisis, the dollar devalued relative to gold by almost 70% on January 31, 1934, the government banned private ownership of gold, and M2 collapsed.

the ratio of gold to M2 has hit the all time high recorded during The Great Depression in 1934. In that crisis, the dollar devalued relative to gold by almost 70% on January 31, 1934, the government banned private ownership of gold, and M2 collapsed.

At first I thought that Amazon still was taking share and causing problems, but this chart suggests that market share has changed very little since 2020.

At first I thought that Amazon still was taking share and causing problems, but this chart suggests that market share has changed very little since 2020.