Co-Founder & Chief Investment Officer at Brilliant Advice

My posts here are not financial advice. Tesla referral link: https://t.co/R8qwa106W4

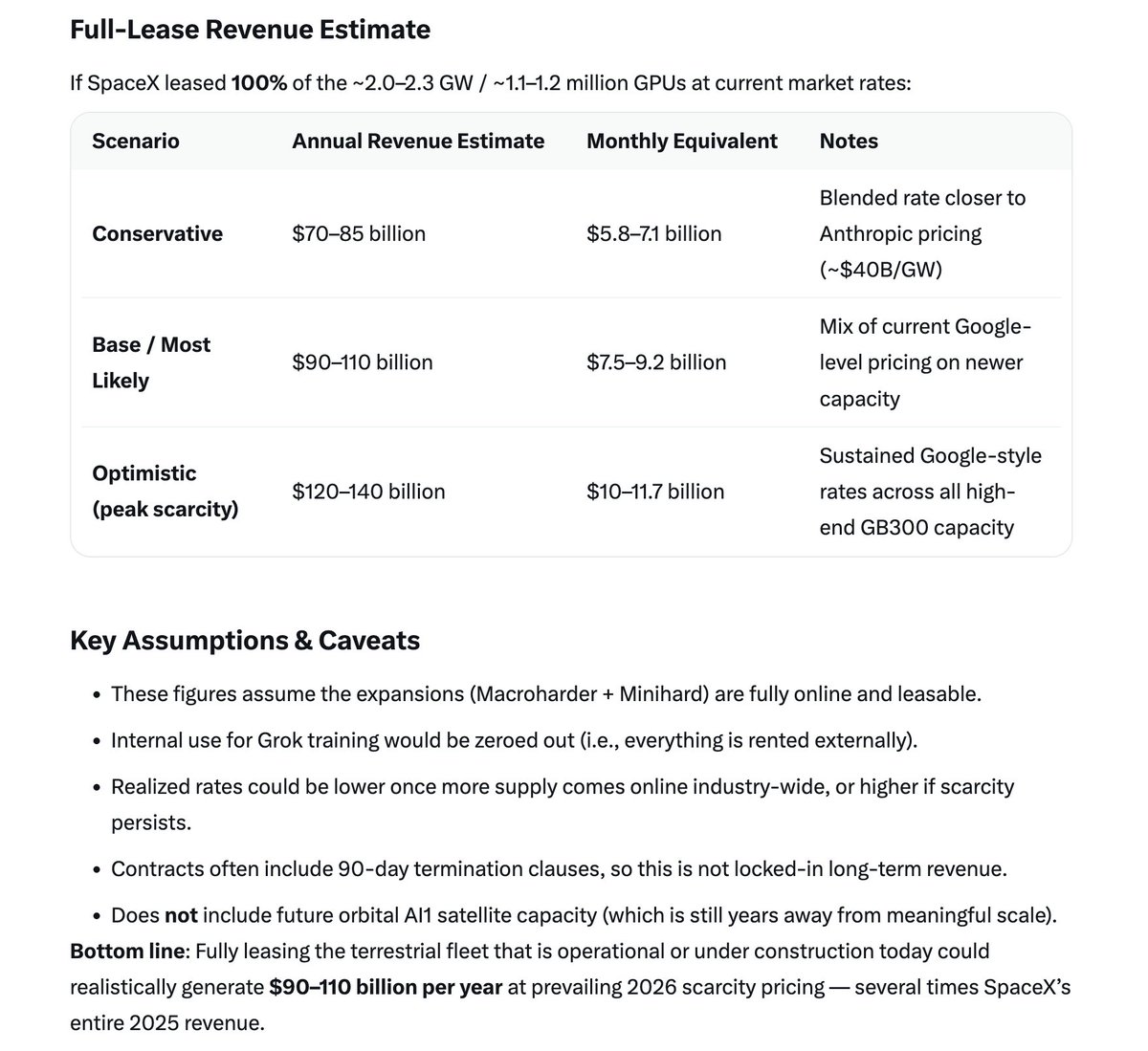

Here's what operational and under construction

Here's what operational and under construction

Core Commonality: Power Projection Through Infrastructure

Core Commonality: Power Projection Through Infrastructure

Solution #1: Cut Spending and Balance the Budget

Solution #1: Cut Spending and Balance the Budget

Many people seem to think that Robotaxis can only make money during the daytime and just for a few peak hours, but this real life case study using non-peak hours proves otherwise.

Many people seem to think that Robotaxis can only make money during the daytime and just for a few peak hours, but this real life case study using non-peak hours proves otherwise.

First, let's take a look at Nvidia - which is the first example of an "AI compounder."

First, let's take a look at Nvidia - which is the first example of an "AI compounder."

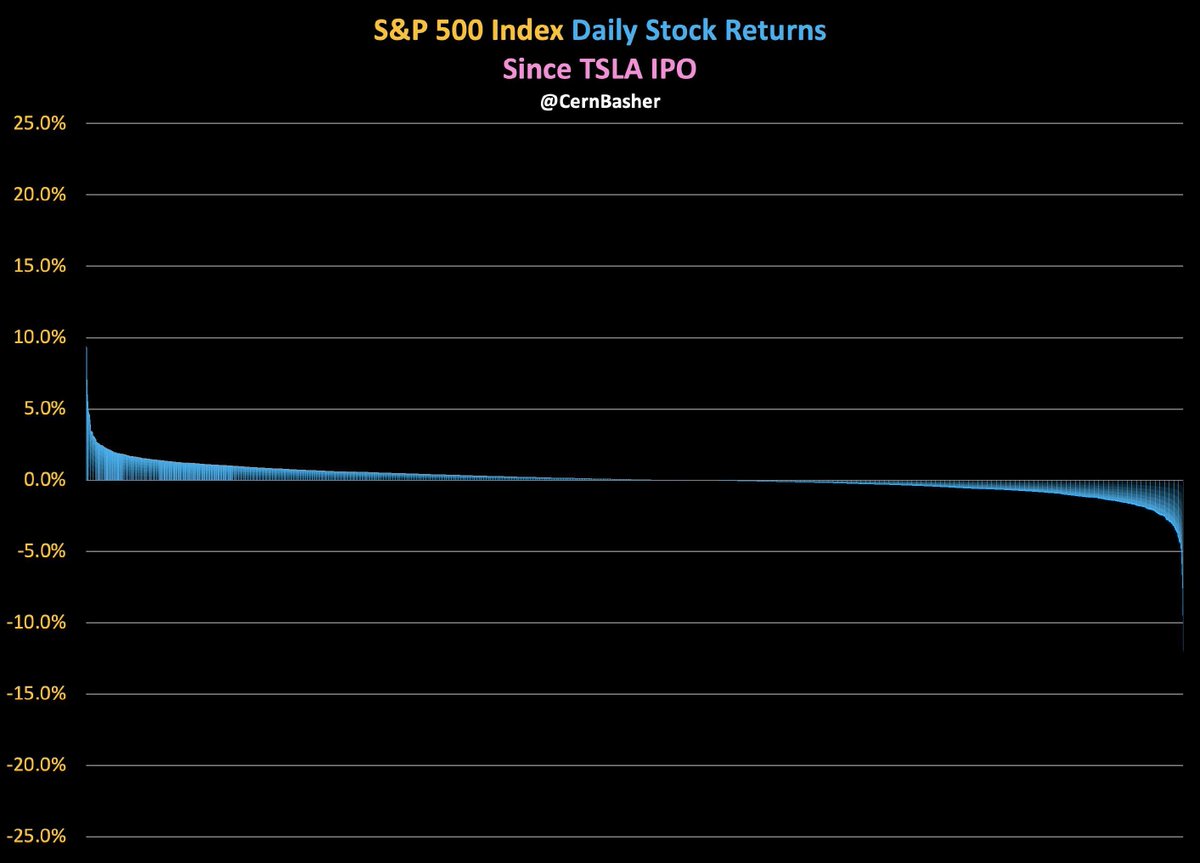

A multi-part post on Tesla's stock performance since the Jun 29, 2010 IPO...

A multi-part post on Tesla's stock performance since the Jun 29, 2010 IPO...

Let's compare Tesla's stock to Nvidia's over the same time period.

Let's compare Tesla's stock to Nvidia's over the same time period.

Lower long-term growth means that short term earnings matter more...

Lower long-term growth means that short term earnings matter more...

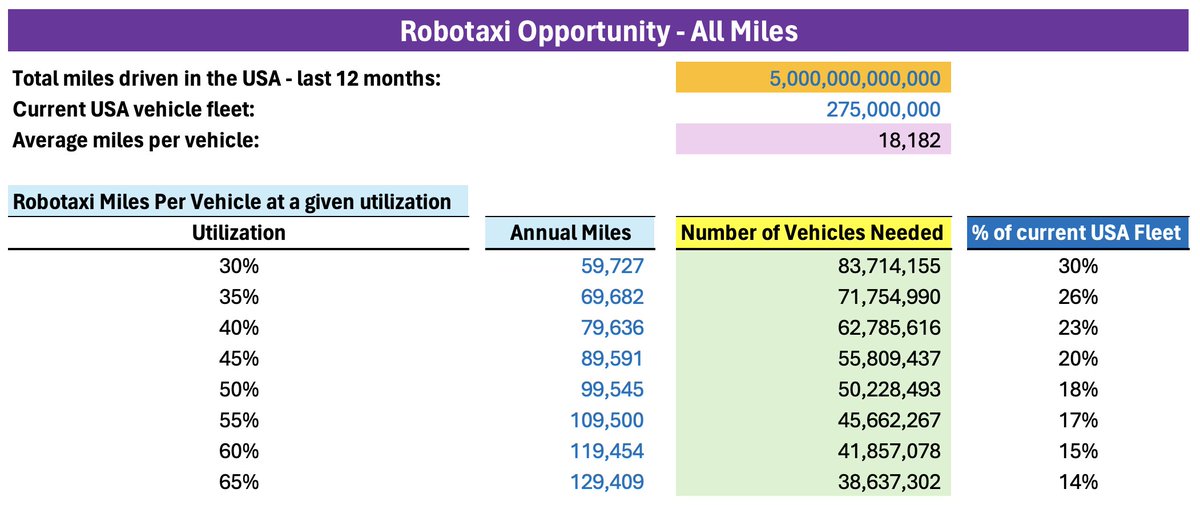

Now, let's look at what could happen when transportation becomes so cheap that people decide to travel more miles - when price goes down, demand always goes up.

Now, let's look at what could happen when transportation becomes so cheap that people decide to travel more miles - when price goes down, demand always goes up.

1) A deflation machine

1) A deflation machine And how might this look for Tesla?

And how might this look for Tesla?

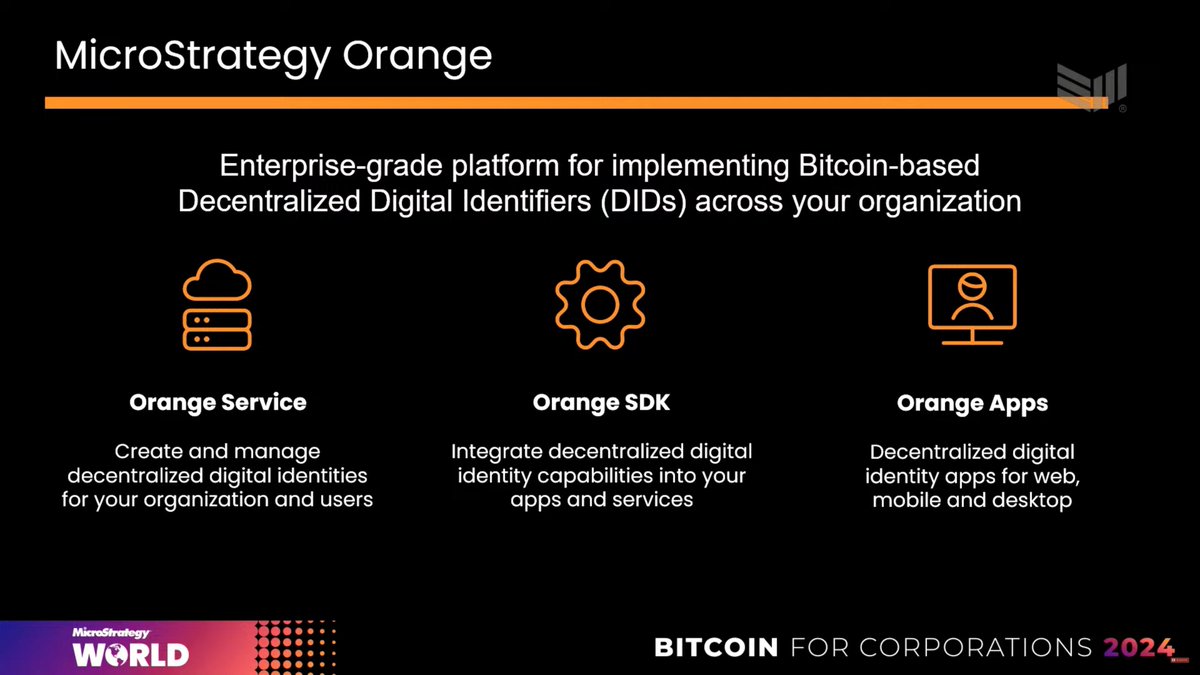

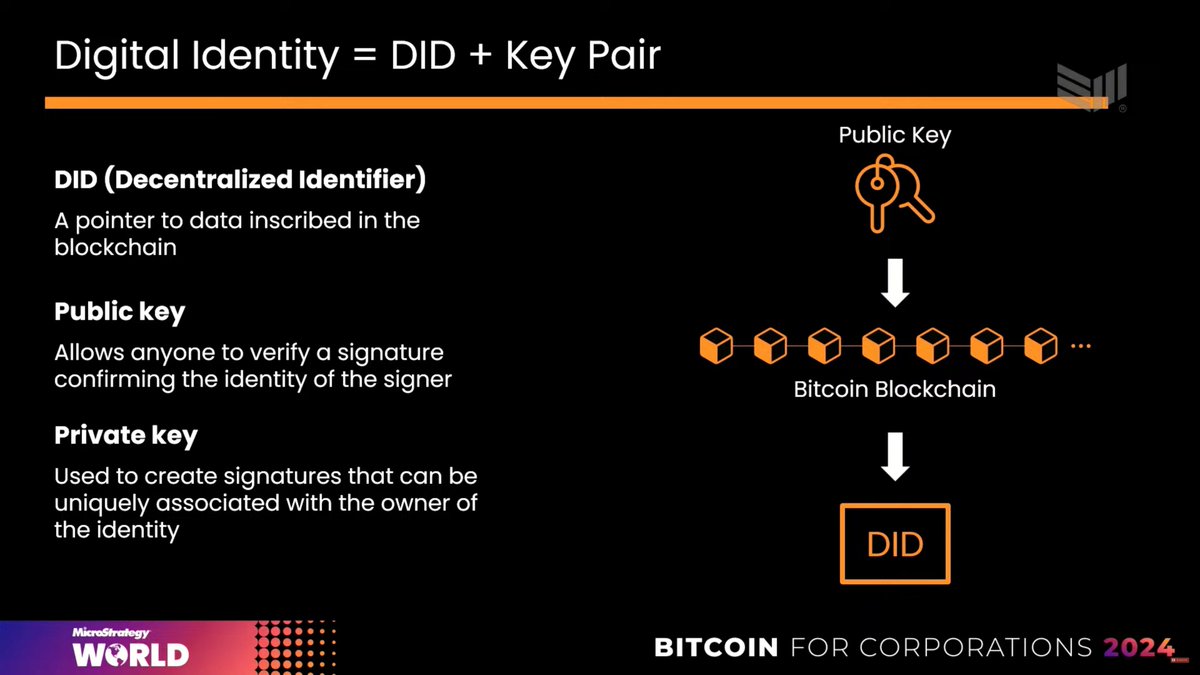

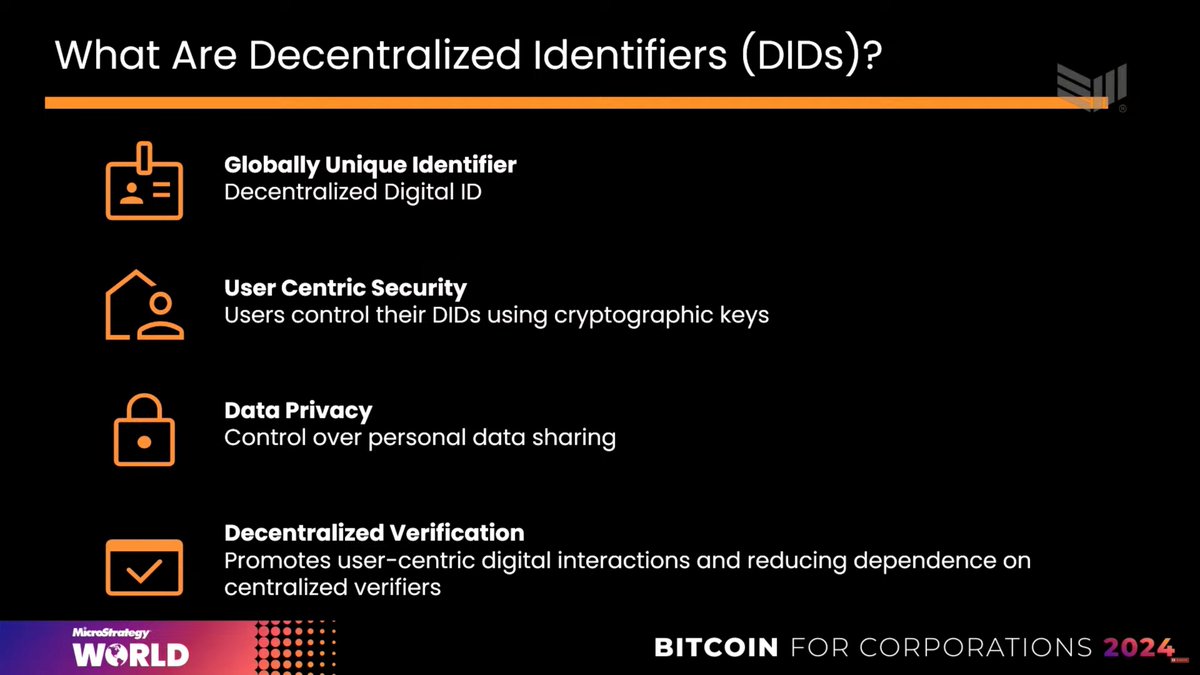

Michael Saylor explains Orange...

Michael Saylor explains Orange... 1) Robotaxi Implications - First, Second & Third Order

1) Robotaxi Implications - First, Second & Third Order

Here are the charts/calculations for the vehicles where FSD has already been purchased. This results in a larger jump in value.

Here are the charts/calculations for the vehicles where FSD has already been purchased. This results in a larger jump in value.

FUMES without Autonomy – a steady decline:

FUMES without Autonomy – a steady decline:

Figure @Figure_robot

Figure @Figure_robot

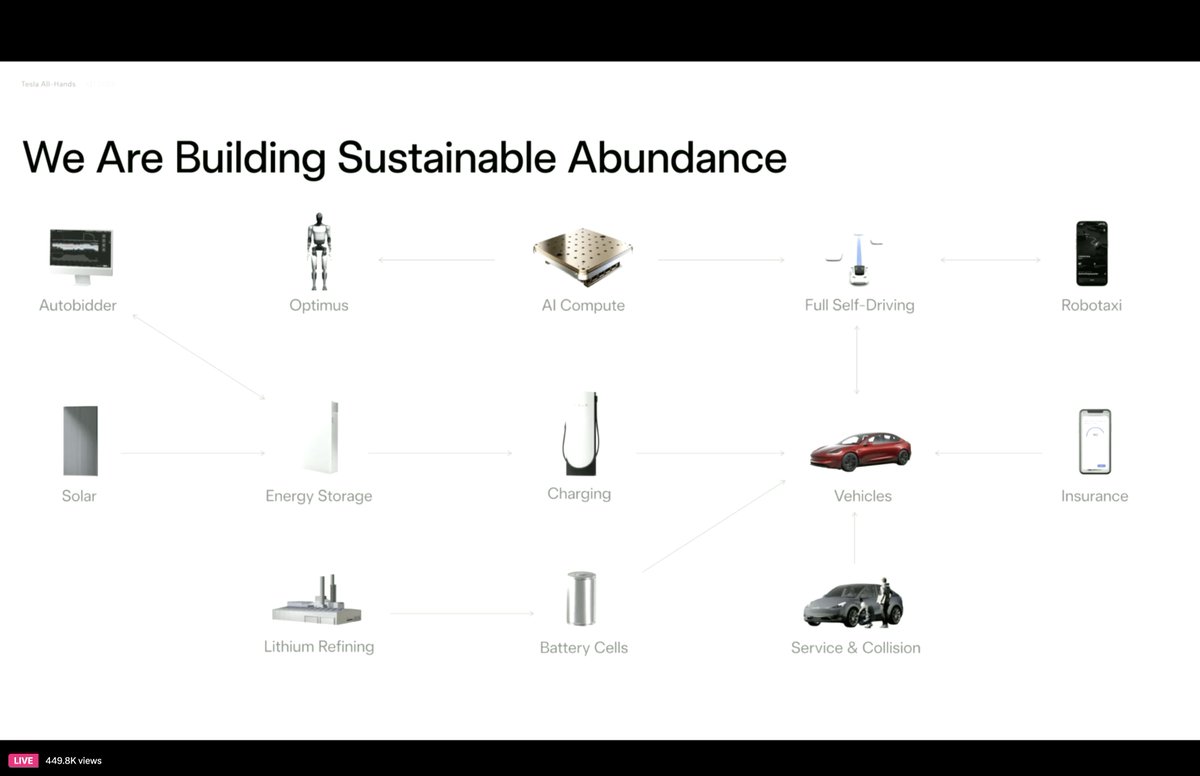

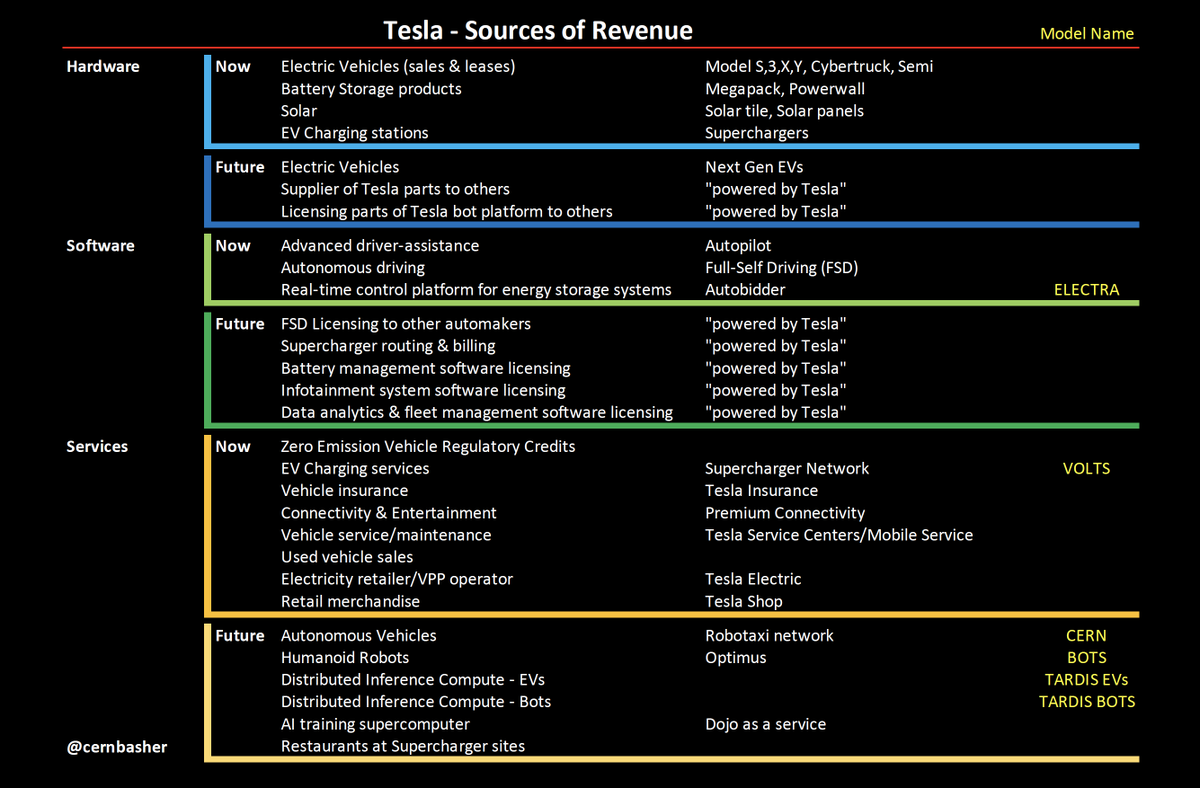

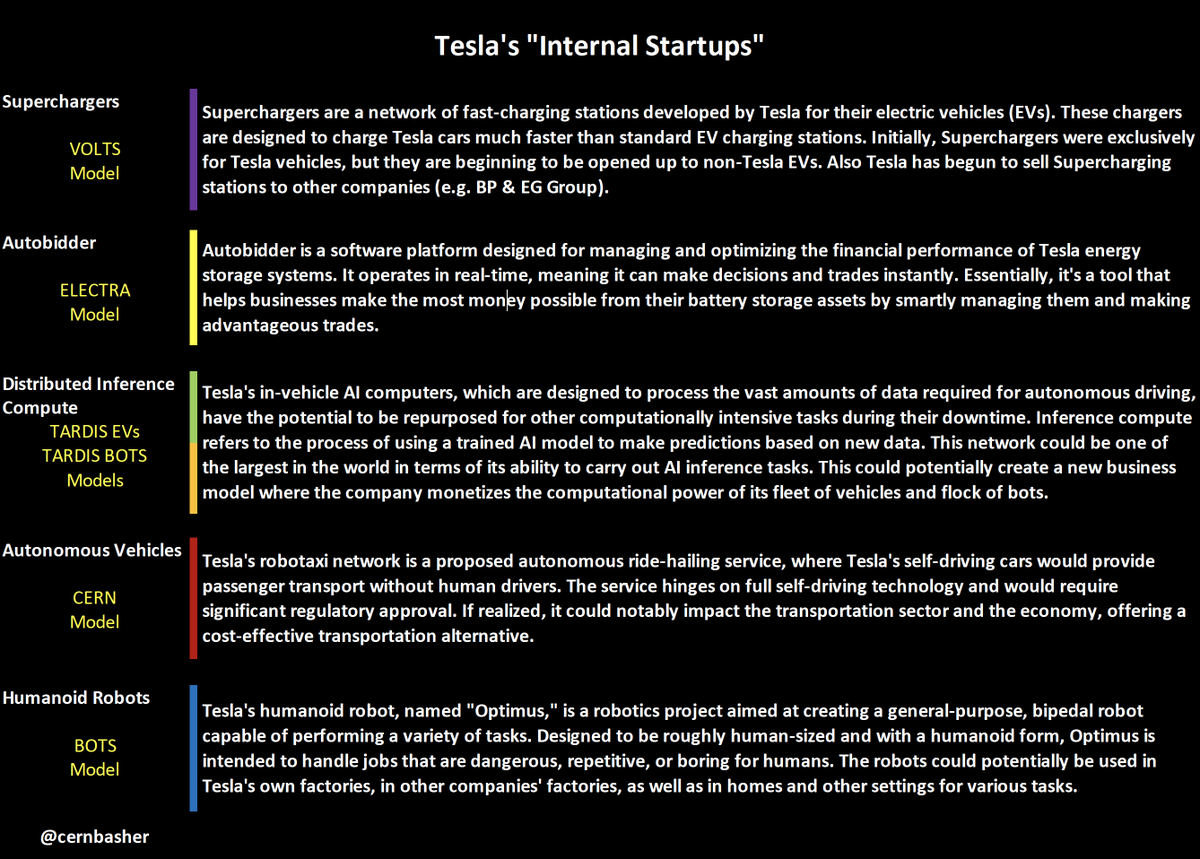

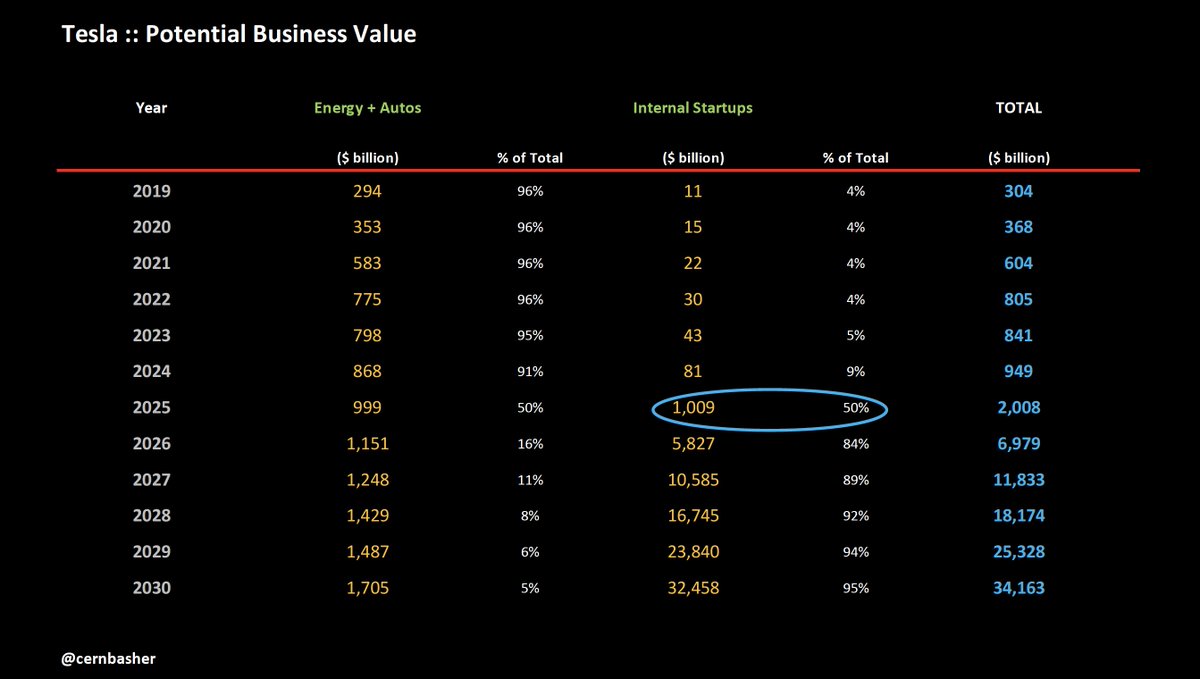

Three of the five Internal Startups - Supercharging, Autobidder and Distributed Inference Computing for both EVs and Bots could account for almost $1 trillion in market value by 2030.

Three of the five Internal Startups - Supercharging, Autobidder and Distributed Inference Computing for both EVs and Bots could account for almost $1 trillion in market value by 2030.

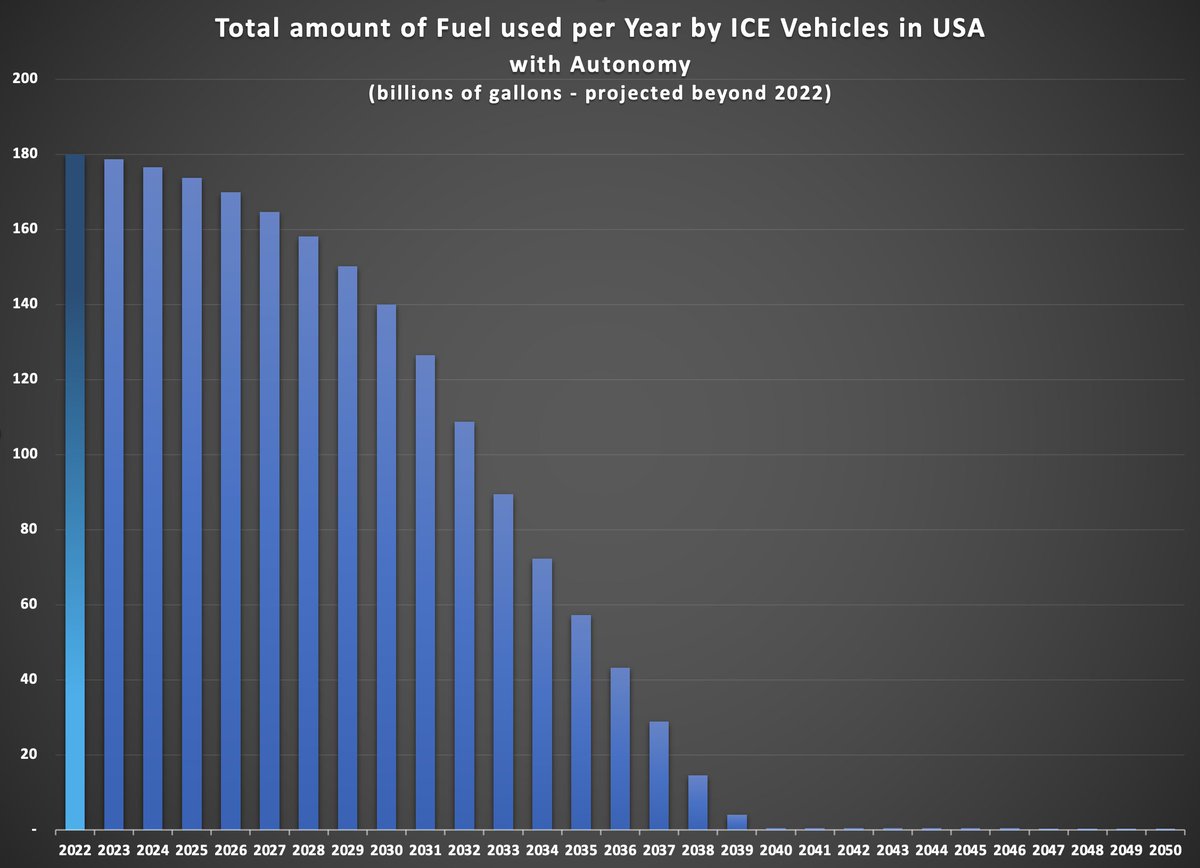

2/ FUMES with Autonomy – a rapid decline:

2/ FUMES with Autonomy – a rapid decline: