Characteristics of Zombie VCs

Characteristics of Zombie VCs Chart: PitchBook diagram of VC cashflows showing massive gap in liquidity.

Chart: PitchBook diagram of VC cashflows showing massive gap in liquidity.

Here's the trendlines for showing the year-over-year TOTAL deal percentage. Up and to the right.📈

Here's the trendlines for showing the year-over-year TOTAL deal percentage. Up and to the right.📈

Step 1: Return Capital to LPs

Step 1: Return Capital to LPs

Law of VC Database: roamresearch.com/#/app/Funds/pa…

Law of VC Database: roamresearch.com/#/app/Funds/pa…

1) Liquidation Preferences

1) Liquidation Preferences

There are two ways to approach financial securities.

There are two ways to approach financial securities.

2/ After five years of testing pre-money Safes, YC made two major changes to the Original Safe:

2/ After five years of testing pre-money Safes, YC made two major changes to the Original Safe:

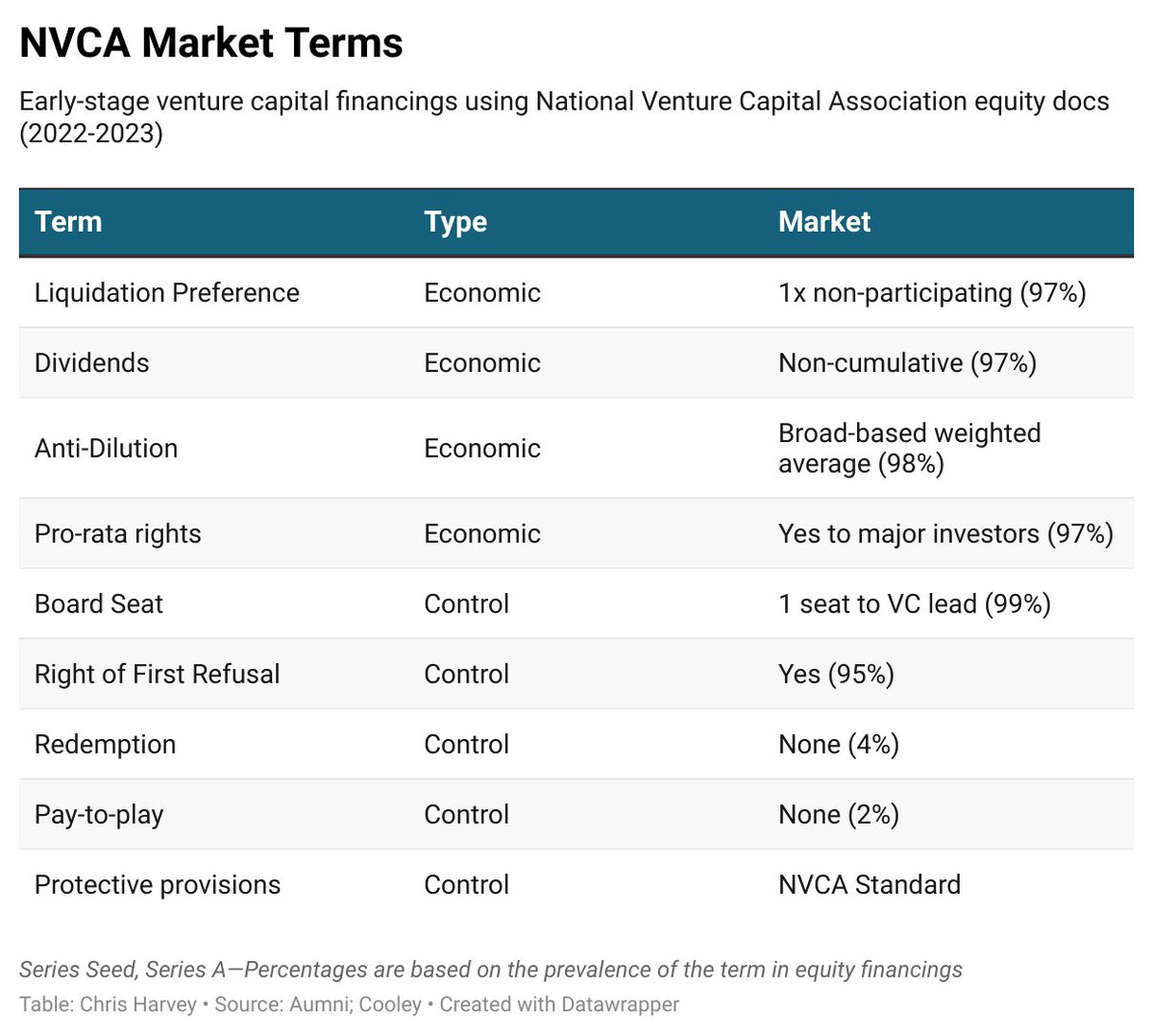

Market Terms for Emerging Venture Funds:

Market Terms for Emerging Venture Funds: