Also, I really do feel a debt of gratitude to the @SubstackInc platform for the way in which we were able to handle this. Through the chat we were able to keep constant contact with our readers and update them in real time, rather than have them kept in the dark while we wrote.

Also, I really do feel a debt of gratitude to the @SubstackInc platform for the way in which we were able to handle this. Through the chat we were able to keep constant contact with our readers and update them in real time, rather than have them kept in the dark while we wrote.

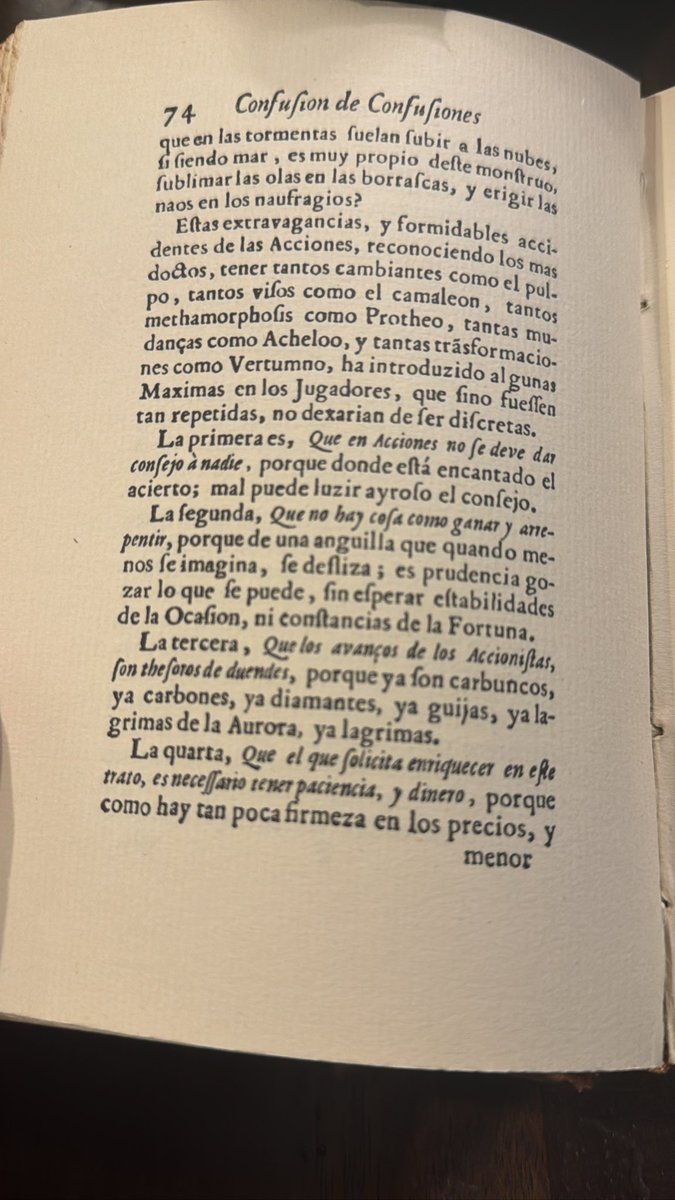

The most well known portion of the book is the discussion of de la Vega’s “four principles”. Paraphrased, these are…

The most well known portion of the book is the discussion of de la Vega’s “four principles”. Paraphrased, these are…

Some people love formulating a comprehensive thesis on single name equities, I love constructing baskets.

Some people love formulating a comprehensive thesis on single name equities, I love constructing baskets.

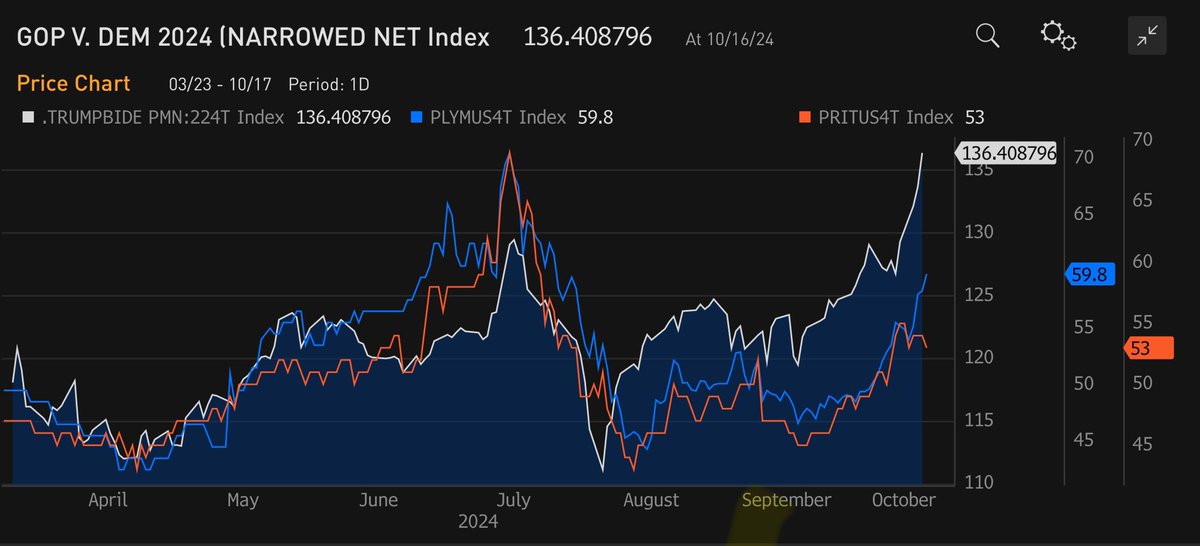

Read my plan, published on 3/5/24. It includes both baskets I mention above & also discusses the potential impact of election results on broad assets & single names alike.

Read my plan, published on 3/5/24. It includes both baskets I mention above & also discusses the potential impact of election results on broad assets & single names alike.

WARNING: UNHINGED MACRO THESIS

WARNING: UNHINGED MACRO THESIS Number 2, never let ‘em know your next move. Don’t you know bad boys move in silence and violence?

Number 2, never let ‘em know your next move. Don’t you know bad boys move in silence and violence?