2) $NVDA claims its China business went to "zero" after April 2025 U.S. trade restrictions. We believe that in reality, over 20% of Nvidia's FY 2026 compute revenues remained driven by China via illegal GPU diversion and Southeast Asian intermediaries.

2) $NVDA claims its China business went to "zero" after April 2025 U.S. trade restrictions. We believe that in reality, over 20% of Nvidia's FY 2026 compute revenues remained driven by China via illegal GPU diversion and Southeast Asian intermediaries.

2) $ADMA recognizes revenues upon delivery to distributors, who then sell onto end customers (infusion clinics, pharmacies, healthcare providers) and ultimately patients. In 2025, two $ADMA distributors drove 73% of revenues and represented 87% of receivables at year-end.

2) $ADMA recognizes revenues upon delivery to distributors, who then sell onto end customers (infusion clinics, pharmacies, healthcare providers) and ultimately patients. In 2025, two $ADMA distributors drove 73% of revenues and represented 87% of receivables at year-end.

2) Tom Lee's $BMNR defends $ETH by claiming "ETH is not in a death spiral because utility is going up." Lee cites post-Fusaka spikes in $ETH active address and transaction counts as evidence of supposed "strengthening fundamentals" and institutional adoption. Lee is clueless.

2) Tom Lee's $BMNR defends $ETH by claiming "ETH is not in a death spiral because utility is going up." Lee cites post-Fusaka spikes in $ETH active address and transaction counts as evidence of supposed "strengthening fundamentals" and institutional adoption. Lee is clueless.

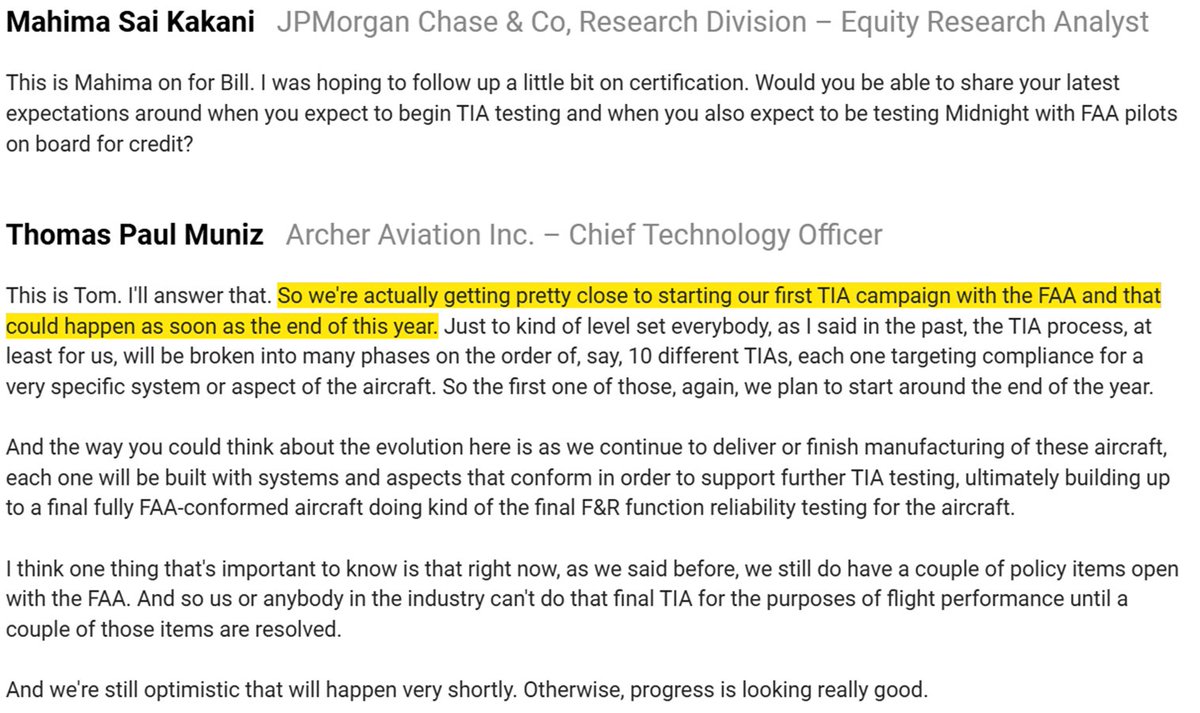

@jimmyfallon 2) We believe $ACHR has systematically lied about Midnight's progress in the LTM, to conceal underlying aircraft stability issues and its sham transition flight. Archer’s claim to near-term commercialization is not only premature, but reckless. Don't just take our word for it...

@jimmyfallon 2) We believe $ACHR has systematically lied about Midnight's progress in the LTM, to conceal underlying aircraft stability issues and its sham transition flight. Archer’s claim to near-term commercialization is not only premature, but reckless. Don't just take our word for it...