Macroeconomist @TS_Lombard, bookworm and gourmet (and glutton). Stubbornly trying to make sense of data before speaking. RT=interesting

Prior to 2008-09 crisis, consensus had German fiscal multipliers around 0.6-0.7. But studies glossed over the state-dependent nature of multipliers and differences in fiscal tools. Since then, literature has shown that output multipliers are larger in certain conditions: 2/

Prior to 2008-09 crisis, consensus had German fiscal multipliers around 0.6-0.7. But studies glossed over the state-dependent nature of multipliers and differences in fiscal tools. Since then, literature has shown that output multipliers are larger in certain conditions: 2/

Unlike in the past, structural headwinds now affect Germany more than the EA 'periphery' because of Germany’s overexposure to manufacturing and exports.

Unlike in the past, structural headwinds now affect Germany more than the EA 'periphery' because of Germany’s overexposure to manufacturing and exports.

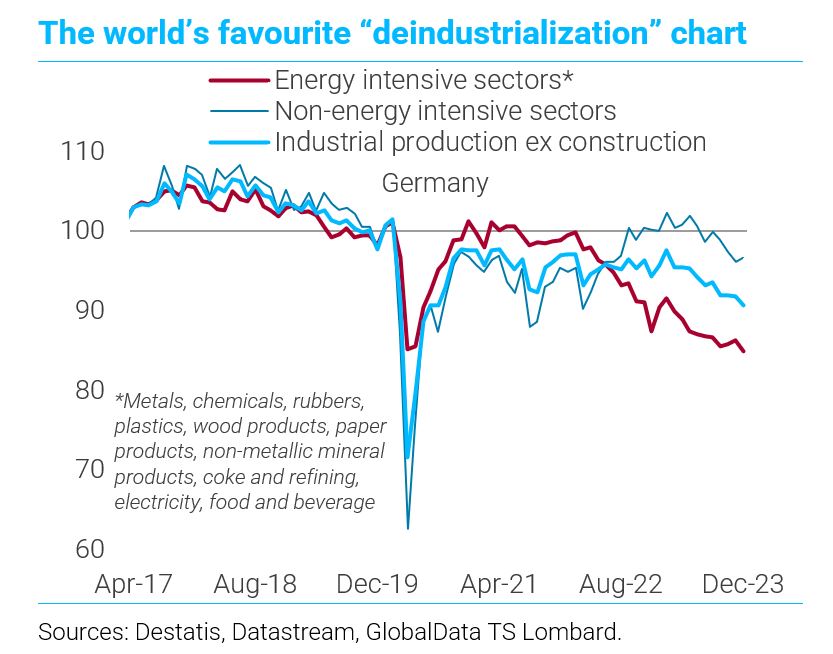

First, the fall in German and EA intermediate goods orders (most relevant for energy-intensive output), has been steeper than for other foreign orders. And it has continued despite the drop in energy/input costs, and easing supply bottlenecks.

First, the fall in German and EA intermediate goods orders (most relevant for energy-intensive output), has been steeper than for other foreign orders. And it has continued despite the drop in energy/input costs, and easing supply bottlenecks.

No doubt, the old export-led EA growth model is dead. The EA is losing competitiveness. First, China is turning from key export market into industrial rival. A big problem for overexposed EA economies and firms 2/

No doubt, the old export-led EA growth model is dead. The EA is losing competitiveness. First, China is turning from key export market into industrial rival. A big problem for overexposed EA economies and firms 2/

In EU, banks’ credit risk via CRE concentrates in the Nordics and Central Europe. Sweden tops the table, but, in the EZ, fixed-rate mortgages make Germany, the Netherlands and France less exposed (although more exposed in terms of loan profitability!) than Austria and Finland 2/

In EU, banks’ credit risk via CRE concentrates in the Nordics and Central Europe. Sweden tops the table, but, in the EZ, fixed-rate mortgages make Germany, the Netherlands and France less exposed (although more exposed in terms of loan profitability!) than Austria and Finland 2/