The number of housing units under construction peaked in October 2022.

The number of housing units under construction peaked in October 2022.

With endless economic news, it's challenging to grasp the economy's current standing accurately.

With endless economic news, it's challenging to grasp the economy's current standing accurately.

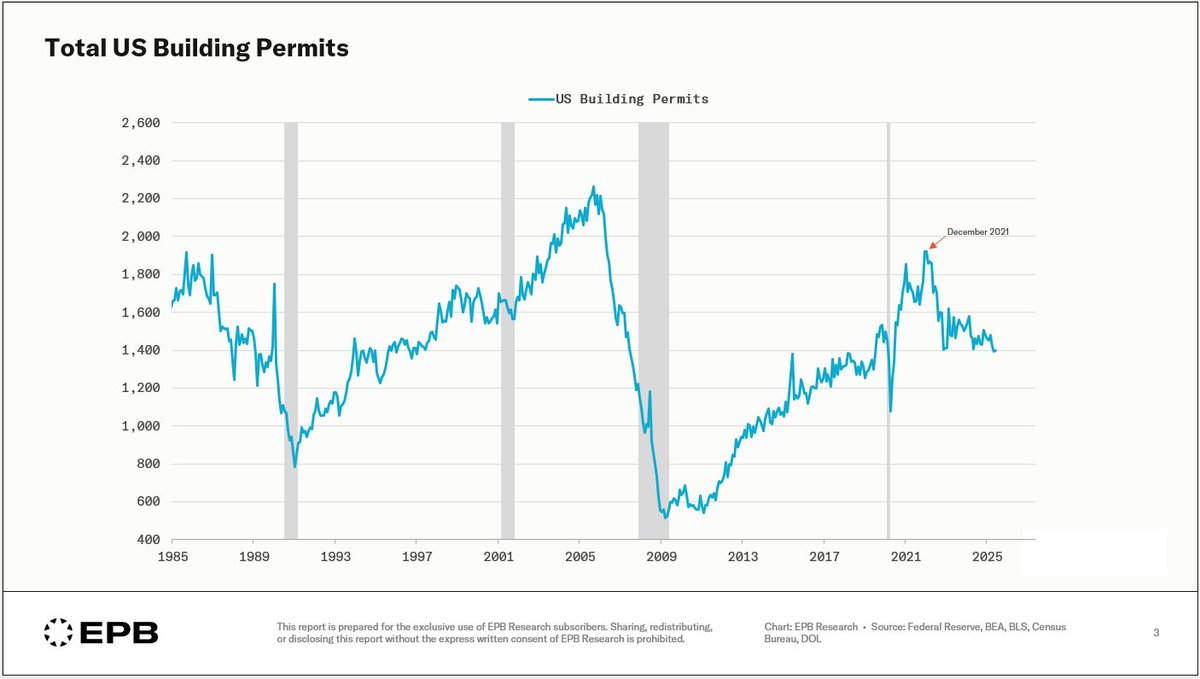

Inventory in the new construction market is at the highest level since the 2008 housing crisis, and this is leading to a massive divide in the housing market.

Inventory in the new construction market is at the highest level since the 2008 housing crisis, and this is leading to a massive divide in the housing market.

Retail sales are reported in nominal dollars, or including inflation.

Retail sales are reported in nominal dollars, or including inflation.

First, the Atlanta Fed GDPNow model is a rolling estimate that gets better with more data.

First, the Atlanta Fed GDPNow model is a rolling estimate that gets better with more data.  The economy has four primary categories:

The economy has four primary categories:

A high quits rate means employees are confident quitting because they believe finding a new, better-paying job will be easy.

A high quits rate means employees are confident quitting because they believe finding a new, better-paying job will be easy.