PARAG PARIKH FLEXI CAP

PARAG PARIKH FLEXI CAP First, a question nobody’s asking:

First, a question nobody’s asking: Rohan was the kind of investor everyone tells you to be.

Rohan was the kind of investor everyone tells you to be. To know the answer, we looked at six different parameters:

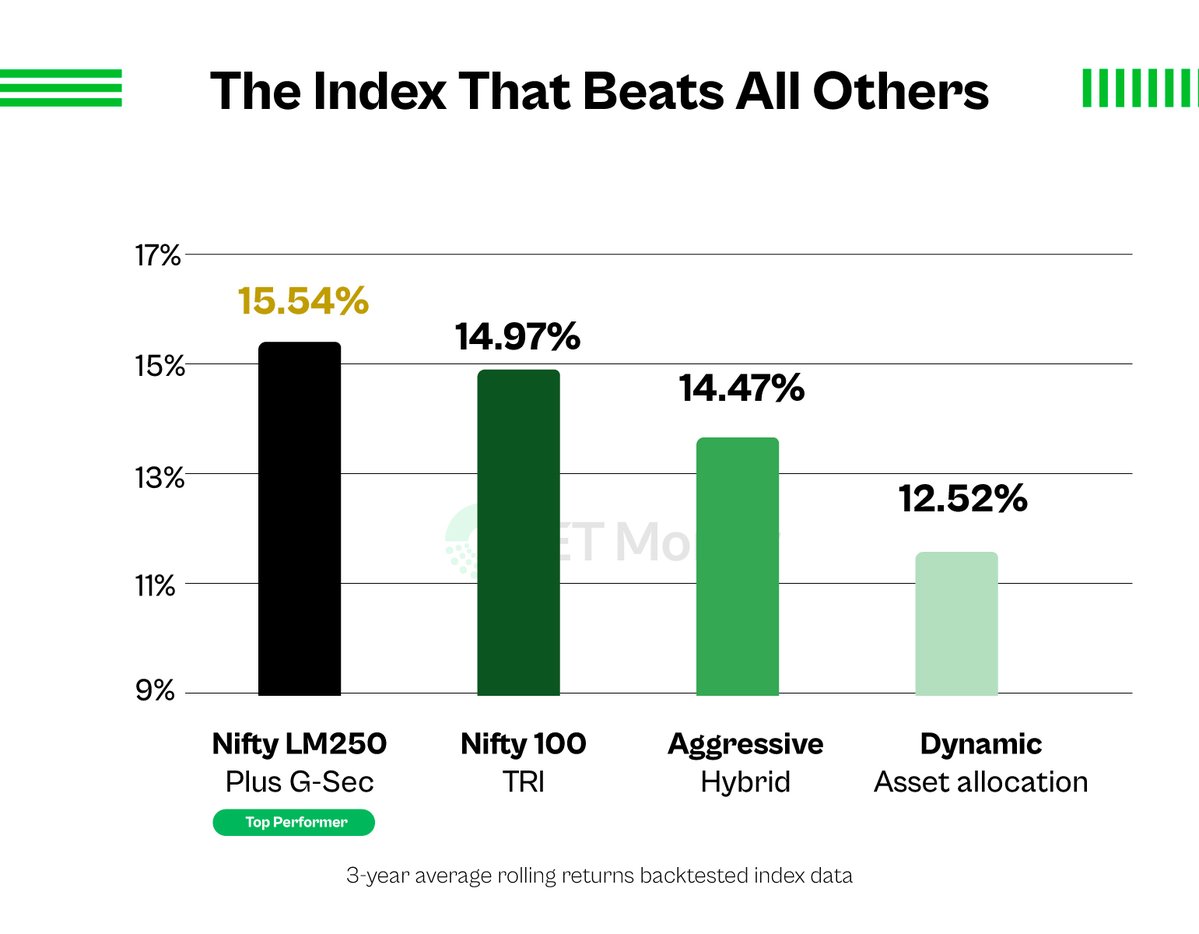

To know the answer, we looked at six different parameters: This fund combined TWO indices into one.

This fund combined TWO indices into one. 1) CASH HOLDINGS

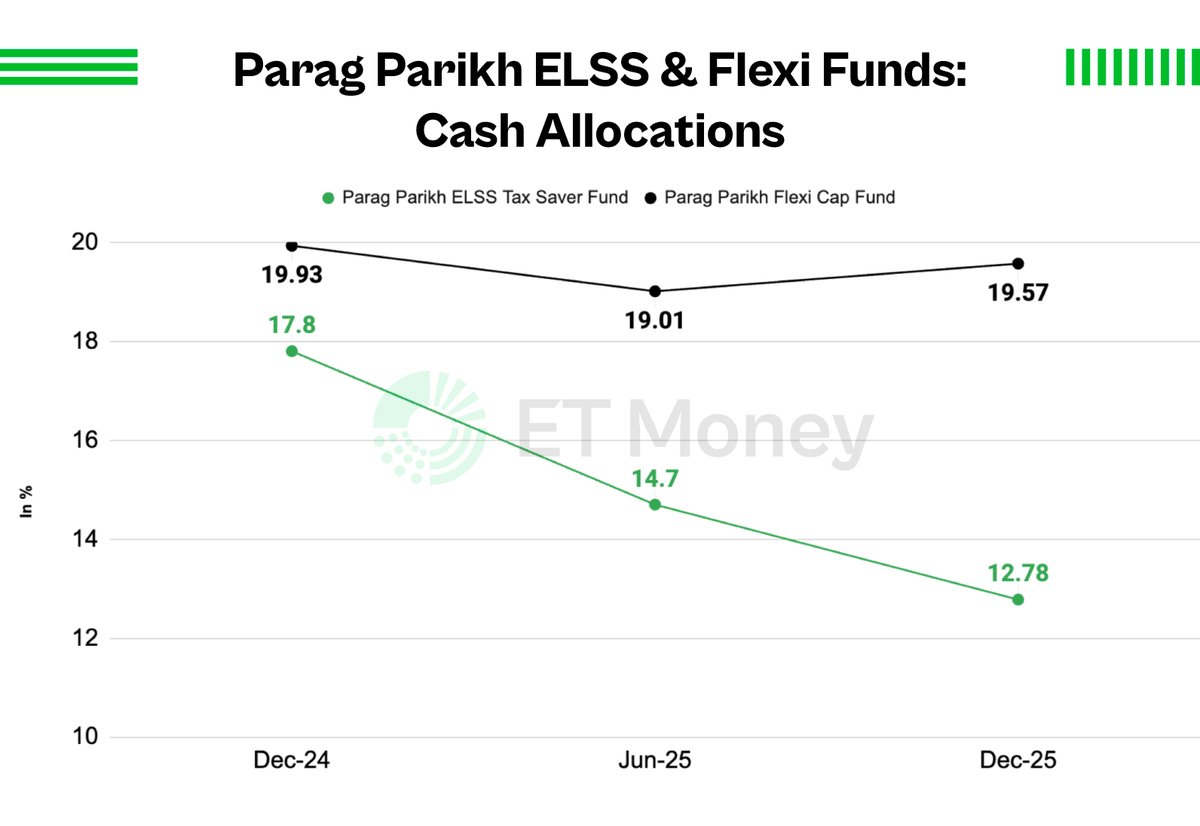

1) CASH HOLDINGS

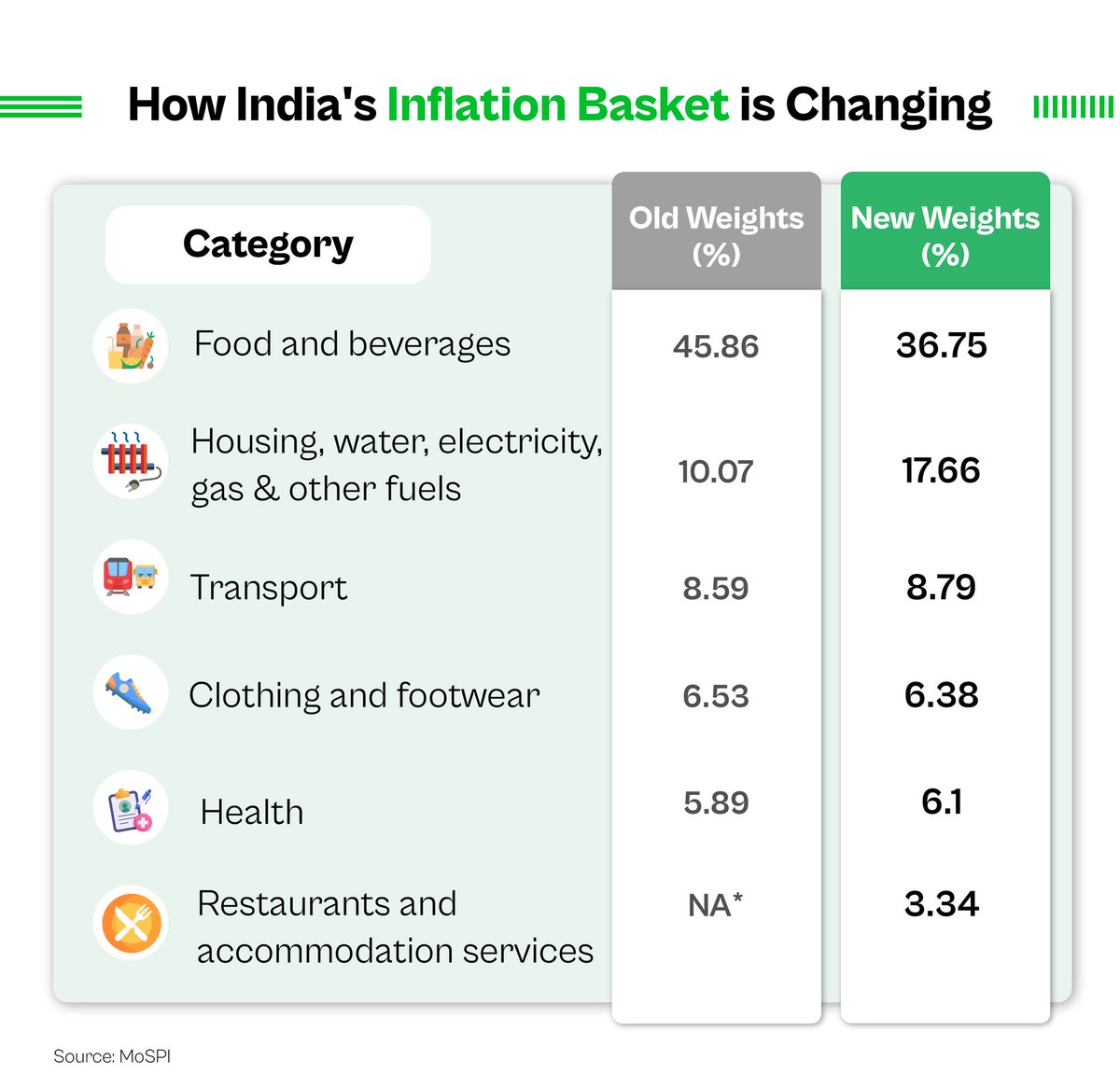

Inflation is measured using the Consumer Price Index, or CPI.

Inflation is measured using the Consumer Price Index, or CPI. Let’s start with the basics.

Let’s start with the basics.

1. BUSINESS MODEL

1. BUSINESS MODEL