Expatriation - #FATCA Letter - CRS - CFC - PFIC - @CitizenshipTax

- US Citizenship Renunciation - @JustRenounce

- Green Card Abandonment - @GreenCardTax

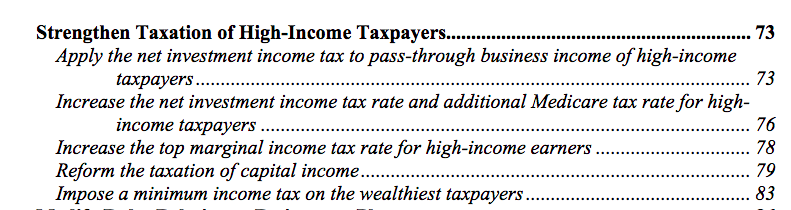

The 2025 Green Book repeats proposals in 2024, 2023 and 2022. For "some" of the impacts on #Americansabroad see this 2022 post from @VLJeker us-tax.org/2022/04/21/par…

The 2025 Green Book repeats proposals in 2024, 2023 and 2022. For "some" of the impacts on #Americansabroad see this 2022 post from @VLJeker us-tax.org/2022/04/21/par…

@TaxResidency Both US citizens and Green Card holders are subject to all provisions (worldwide tax, reporting and penalties) of US tax code. Green card holders (but not citizens) may use treaty (dual @taxresidency tie break) to become "treaty nonresidents" and taxable only on US source income.

@TaxResidency Both US citizens and Green Card holders are subject to all provisions (worldwide tax, reporting and penalties) of US tax code. Green card holders (but not citizens) may use treaty (dual @taxresidency tie break) to become "treaty nonresidents" and taxable only on US source income.

2016 US Model Tax Treaty has three "saving clause" provisions: 1. "Saves" US right to tax its "residents" (as determined under treaty tie break rules). 2. Tax US citizens who are residents of treaty partner country (treaty tie break rules don't apply) 3. Tax former citizens!

2016 US Model Tax Treaty has three "saving clause" provisions: 1. "Saves" US right to tax its "residents" (as determined under treaty tie break rules). 2. Tax US citizens who are residents of treaty partner country (treaty tie break rules don't apply) 3. Tax former citizens!